Today’s blog post is an unedited version of our Business Day article.

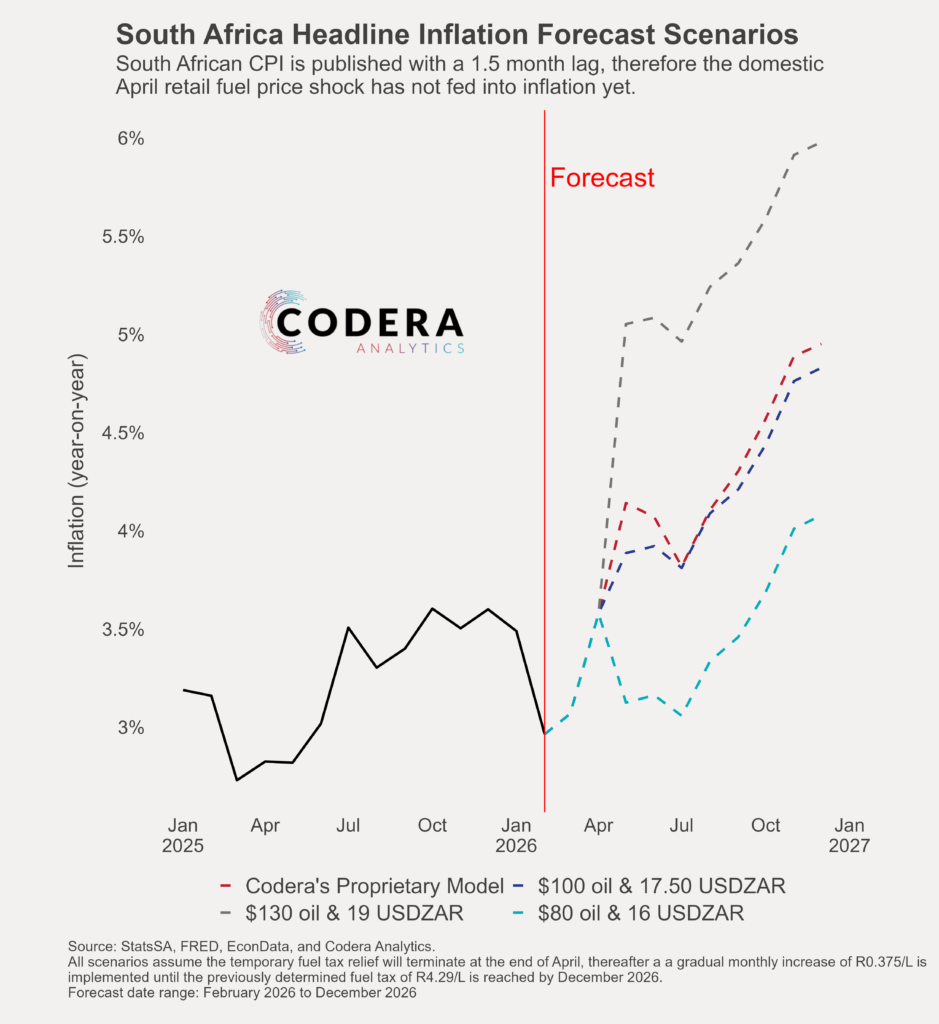

South African consumer inflation is most likely going to increase to over 4.5% in the next 12 months. This is not just because of externally imposed pressures from oil prices, but optimistic projections of the Reserve Bank that means monetary policy is more accommodative than it should be.

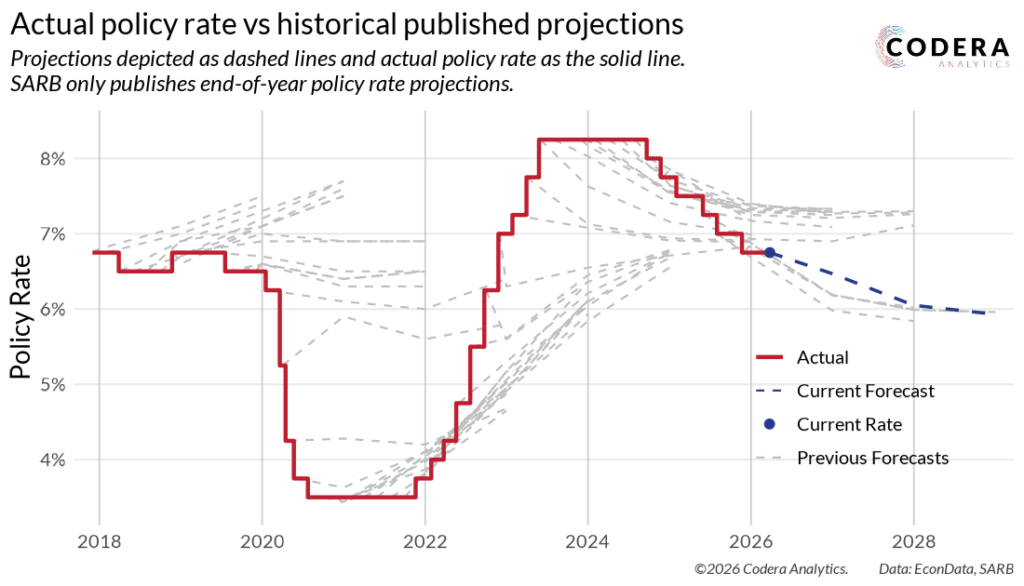

In late March, the Reserve Bank projected that it could cut its policy rate by 25 basis points and still meet its new inflation target. This projection assumed that the policy stance is currently restrictive relative to market conditions, that inflation expectations are anchoring to the new target, and that the spike in the global oil price would be short-lived. There is growing evidence that these assumptions are not going to hold in 2026.

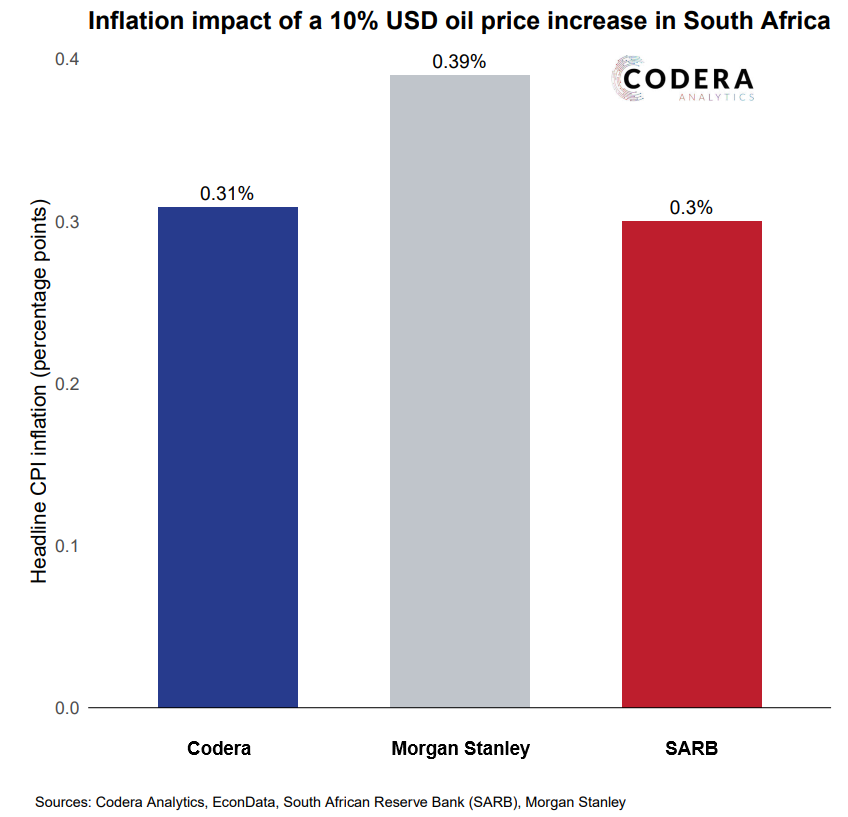

Oil price spikes and exchange rate volatility mean that there is a significant transport cost increase heading our way. Our modelling suggests that over the long term, headline inflation rises by 0.3 percentage points in response to a 10% increase in the US dollar price of oil. However, when oil price increases are accompanied by a weaker exchange rate or other supply chain disruptions, the ultimate impact on inflation tends to be higher still. Since the exchange rate depreciated sharply in March, we forecast that inflation will rise to over 4.5% this year and continue rising to over 5% by early 2027. Should the oil price increase further and the rand depreciate, inflation will rise even more.

The market now expects at least a 50 basis point increase in the bank rate this year. Why does the market think the Reserve Bank’s baseline projections will not bear out?

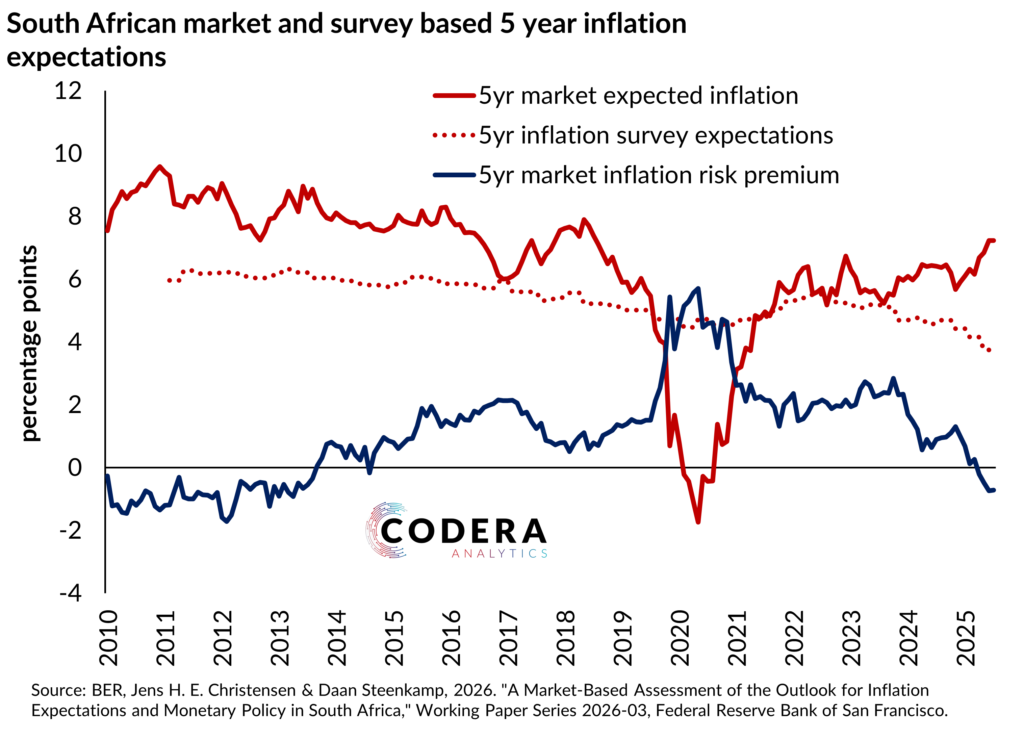

Apart from concern that the Middle East conflict could persist, this reflects an increase in the risk premia that affect the rand and government borrowing costs. Our modelling shows that the market is also not convinced that average inflation is going to fall towards the target over the next five years. When we use all government bonds in issuance to extract inflation expectations and inflation risk premia, we find that market-implied inflation expectations have not declined since the announcement of a lower target.

Our estimates suggest that sustainably reducing inflation to the new target would require monetary policy to remain tighter than assumed by the Reserve Bank. Since inflation expectations are partly backward-looking in South Africa, inflation would need to average near the new target for a long time before price setting and wage demands could be expected to change sustainably. To anchor expectations at the new target, the policy rate will need to be higher for longer than the Reserve Bank currently projects.

Another reason why the market expects inflation to pick up more than the Reserve Bank is that the Bank is assuming that the government and other stakeholders have bought into the lower target. It is not clear that has happened yet.

Take electricity price increases. The Bank projects lower electricity price increases than we think are realistic, given the challenges Eskom faces. The Bank projects electricity inflation of 9.1% in 2026, tapering off to only 3% over the long term.

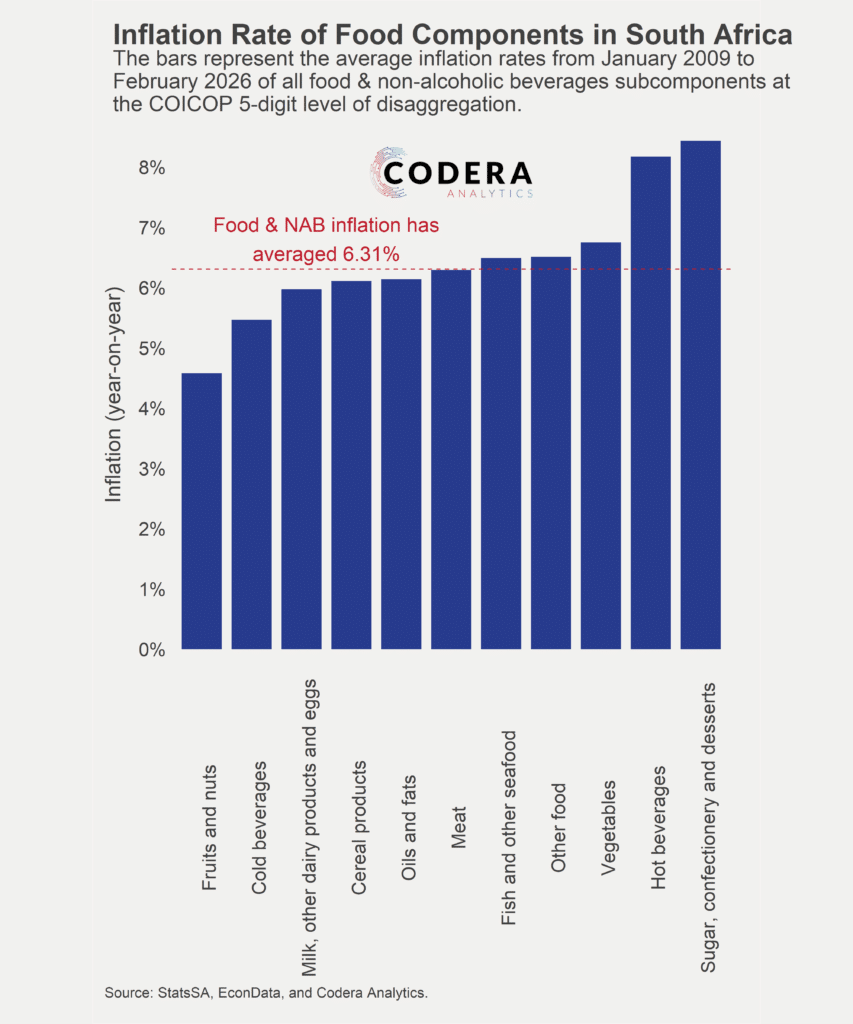

The Reserve Bank’s latest projections also assume that food inflation in South Africa will shift structurally lower following the reduction in the inflation target. But food inflation in South Africa has historically been much higher than the new target. Since January 2009, food inflation has averaged 6.3% – much higher than the 3% the Bank assumes over its projection period. Recent farmgate price data suggest that many food categories, particularly meat, will continue to experience increases at much faster rates than the inflation target, particularly as fertiliser and transport costs spike. Early indications are also that labour unions will continue to push for wage increases that far exceed the new target.

The credibility of the Reserve Bank’s commitment to the new target will be tested this year. The Bank’s job would be much easier if organs of the state and unions were to commit to not only the lower target, but also to reforms that promote the responsiveness of inflation to monetary policy.

One such reform would be deregulation of retail fuel prices in South Africa. This would promote competition, potentially lowering margins. It would also make the market more responsive to supply and demand changes, improving efficiency.

Reforms that address above-target inflation in other categories of government-related inflation are also important. Interest rate changes do not affect water and utilities prices, so the Bank needs help from government if inflation in these categories is to be brought under control.

Structural reforms that improve public service delivery, enhance competition, align South Africa’s policy frameworks to global best practice, and promote investment are needed to reduce supply side pressure on prices. Public support needs to be galvanised for such ambitious reforms. Without a unified national effort to support the new target, South Africans should prepare for significantly higher borrowing costs. The question is: who will organise such a social compact?

Dr Steenkamp is CEO of Codera Analytics and a research fellow with the economics department at Stellenbosch University.