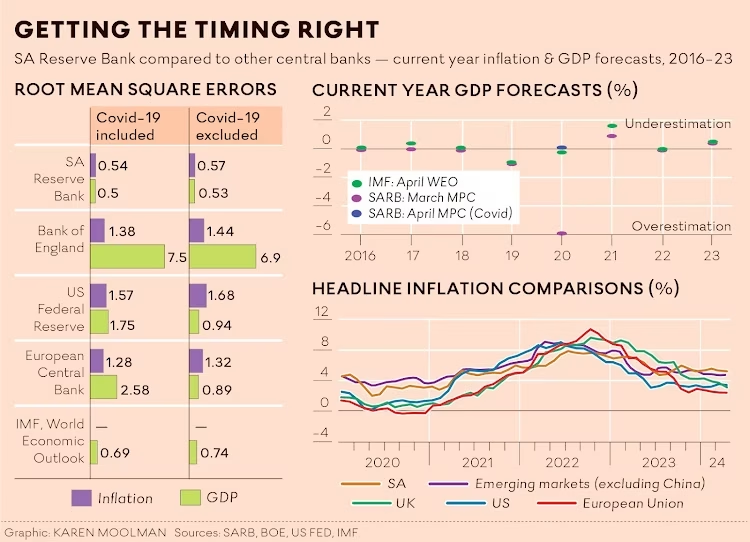

In ‘How Reserve Bank’s forecasting fares in uncertain times‘ the Reserve Bank (SARB) asserts that its forecasts have been more accurate than the International Monetary Fund (IMF)’s estimates for South Africa and more accurate than the forecasts of the Bank of England, European Central Bank and US Federal Reserve Bank for their economies. In the post, we assess this claim.

No one saw the COVID-19 pandemic coming, so it is useful to split out comparisons of forecasts errors for a sample that excludes the pandemic. Using the SARB’s published projections from all Monetary Policy Committee (MPC) Statements between 2016 and 2023, we obtain root mean square errors (the measure of forecast accuracy used in the SARB’s assessment) consistent with those SARB reported for CPI inflation and for GDP growth when the COVID pandemic is excluded from the sample, but forecast errors are almost four times larger for GDP for the full sample than reported by SARB.

Annual forecast errors (1 year ahead, calculated by Codera)

| Period | SARB CPI inflation | SARB GDP growth |

| 2016-19 | 0.48 | 0.50 |

| 2020 | 0.50 | 5.80 |

| 2021-23 | 0.65 | 0.57 |

| Incl. Covid-19 | 0.55 | 2.11 |

| Excl. Covid-19 | 0.56 | 0.53 |

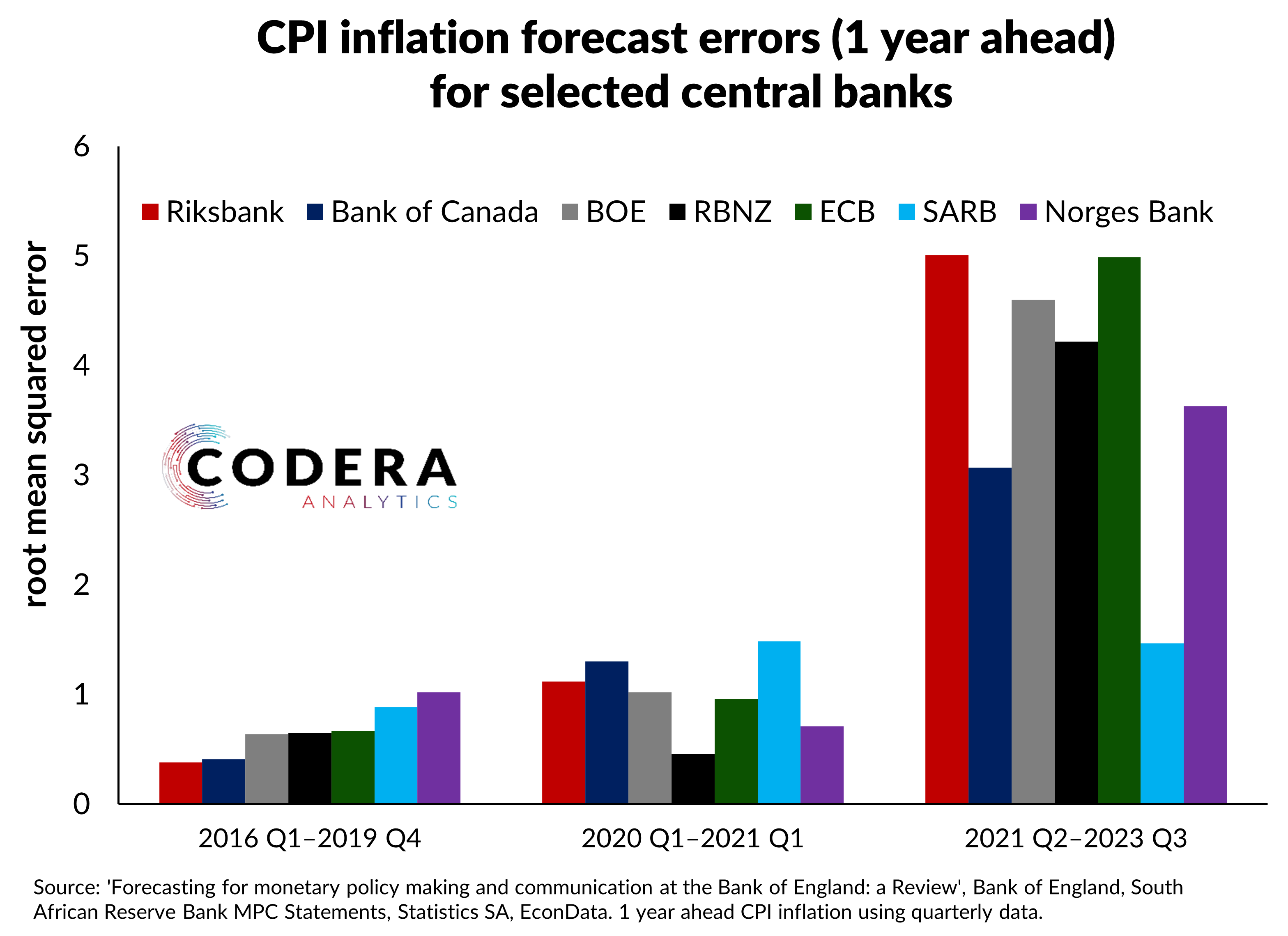

SARB’s inflation forecasting performance has been commendable, with inflation forecasts relatively accurate compared to GDP. However, we cannot replicate the comparisons to the other central banks SARB provided or IMF projections. In the chart below, we compare inflation forecasts of other central banks from the Ben Bernanke review of forecasting by the Bank of England. We do not find that SARB’s inflation forecasts have been more accurate than those of major central banks they compared themselves to. In large part, this owes to the more volatile inflation rate of South African CPI when compared to developed markets, which makes it more difficult to forecast. This feature of developing economy data is something that is observed across most economic measures when comparing developing and developed markets. This is in contrast to the article that shows that the SARB has forecast CPI and GDP more accurately than all of the developed economies (shown in the article) in recent times.

This comparison is only possible for inflation as the SARB does not make quarterly forecasts of GDP available. However, the GDP forecast errors presented by SARB are much lower than presented in our pre-COVID study of SARB forecast errors published in the South African Journal of Economics.

In an earlier post, we compared SARB projections CPI and GDP to IMF projections using a different forecast error definition and annual projections, and showed that SARB projections for current year and next year South African GDP growth (as projected at the time of the March Monetary Policy Committee Statement) have been more optimistic than those of the International Monetary Fund’s (IMF) (as published in April). The IMF’s inflation projections have been slightly less accurate for the current year and one-year ahead, on average.

Footnote

In the comparison to other central banks above we use quarterly data and assume that the Bernanke review sample periods correspond to forecast dates and not the dates of when the forecast was made.

Note that the IMF comparisons presented do not exclude the COVID pandemic.