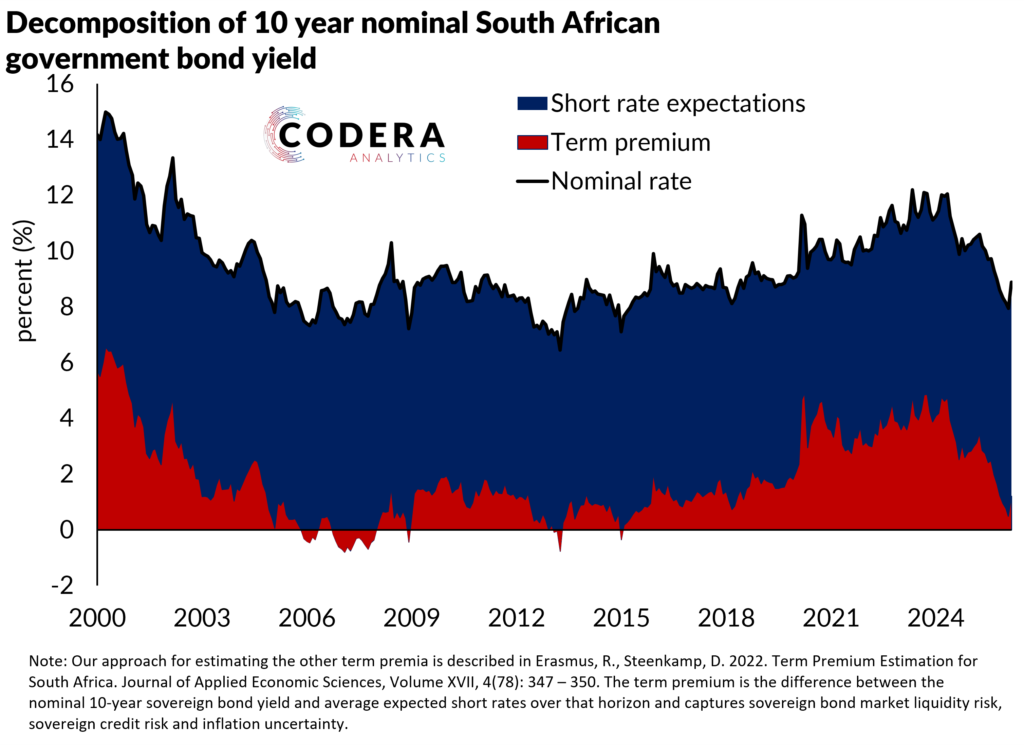

Today’s post provides an update of Codera’s term premium estimates for the South African sovereign bond curve. Focusing on the 10 year point, our estimates show that that the recent increase in long yields has reflected a higher term premium and an increase in average expected short rates. After nearing post-2000 lows, the term premium is back to over 1 percentage points, while average expected short rates jumped just over 25 basis points since the start of the Iran conflict.