SARB releases a Monetary Policy Review (MPR) twice a year to provide more detail about its interpretation of the drivers of the economic outlook and the appropriate stance of policy. The headlines from the MPR included:

- SARB expects core inflation to remain elevated near recent levels at around 4.9% over the next year

- Exchange rate pass-through to inflation is estimated to have increased by 60% since its estimated low in 2018Q2, representing an upside risk to the outlook for core inflation

- The SARB projects our risk premium to fall, under the assumption that GDP growth improves and the fiscal situation improves as predicted by National Treasury. Continuation of an elevated risk premium therefore presents an upward risk to their long term interest rate projections

- SARB’s potential growth estimate is unchanged at -0.2% for 2023, rising to only 0.8% for 2024. This is similar to estimates we recently presented, although there is a quite a lot of divergence between historical estimates from alternative approaches

- In the post-presentation discussion, it was noted that loadshedding is estimated to have subtracted 1.8 percentage points from GDP growth this year, with smaller impacts expected for 2024

- The SARB interpreted rising coupons on new bond issuances as ‘reflecting a rising supply and softening demand’, expressing concern over financing risk for the government

- The balance of risk of targeted rate of inflation is to the upside, as communicated through their CPI fan chart

- The SARB projection for the policy rate has not been updated since the September decision, at which time it suggested the rate would remain at its currently level for the rest of 2023 before beginning to fall in 2024Q1

- The monetary policy stance is assessed to be restrictive (as shown by a real repo rate about their estimate of neutral, see chart below), and predicted to remain so over the entire forecast horizon.

The SARB also noted potential upside risk to the global neutral rate, although it did not present estimates. Our own estimates suggest that South Africa’s neutral rate has remained relatively stable over the last couple of months, as have market-implied rates for the US and several other major economies (with the exception of the UK).

Estimates of the impacts of a weakening sovereign financial position for long bond yields were presented: ‘long-term bond yields are estimated to rise by between 9 and 12 basis points for every percentage point increase in fiscal deficits’. It is a bit unusual to use the fiscal balance for this type of analysis, as it does not always map very well to measures of fiscal risk, such as higher borrowing requirements or higher debt. There is also a rather confusing footnote that states that ‘simple regressions reveal that a one percentage point deterioration in fiscal balances or increase in the debt ratio pushes yields up by around 6 to 10 basis points’, given the various econometric challenges when variables are trending and there are potential non-linear relationships between variables.

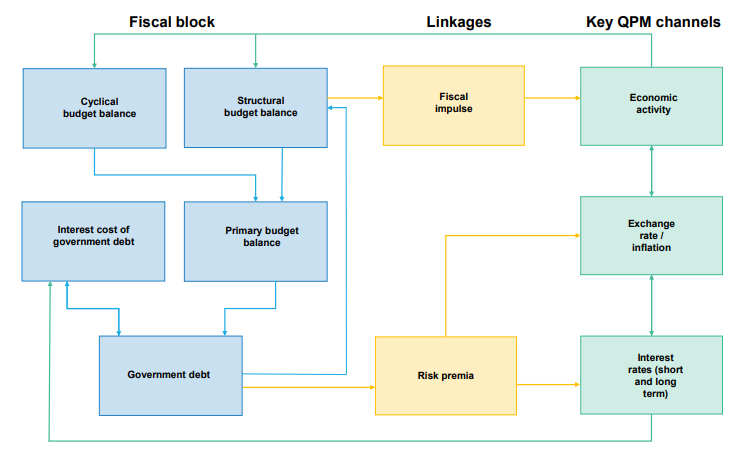

The lack of assessment of the implications of the stance of fiscal policy for monetary policy is noteworthy given the recent inclusion of a fiscal block in the SARB’s QPM model. The MPR does state that ‘as long bond yields increase and become more sensitive to fiscal developments, they become less responsive to monetary policy.’ This argument presumably ascribes the recent increase in the term premium embedded in long rates to higher fiscal risk, although this seems hard to confirm empirically with commonly used proxies. It would be nice to see deeper analysis of this issue.

Likewise, the MPR suggests that the shift to a surplus-based monetary policy implementation framework (MPIF) has enhanced the transmission of monetary policy. Unfortunately, the accompanying charts in the financial market section do not make it possible to assess how interbank spreads and other market rates have changed compared to the pre-MPIF period, so it would be nice to see supporting analysis in a future MPR.

Lastly, it is a pity that the MPR does not use the QPM to communicate the narrative underlying their most recent projections and the stance of policy. For example, while there is frequent mention of the implications of demand and supply developments, there is no explicit analysis of the contribution of these shocks to the persistence of inflation. The advantage of having a framework like QPM available is that it can support better understanding of the central bank’s economic narrative about historical developments in the economy and help market participants and the public understand how it is likely to react to specific economic shocks.