SARB estimates that load-shedding has reduced economic growth in 2022 by 0.7 percentage points, and will reduce growth by 2 percentage points in 2023 and 0.8 percentage points in 2024. Their estimates are on the high end of the range that others have published but are more up-to-date, while they have lowered their potential growth estimates to closer to what what the IMF and World Bank have estimated previously, down to -0.2% for 2023 and rising only to 0.8% in 2024. For inflation, SARB estimates load-shedding’s impact on prices to be 0.6 percentage points in 2022, with 1.1 percentage points expected to be added in 2023 from load-shedding (an extra 0.5 percentage points relative to 2022). It is likely that the full impact of load-shedding could be larger than what the SARB estimates, given that their estimation approach does not account for the various indirect impacts of load-shedding, such as on investor confidence and the currency (notably, SARB is quite upbeat about the outlook for investment).

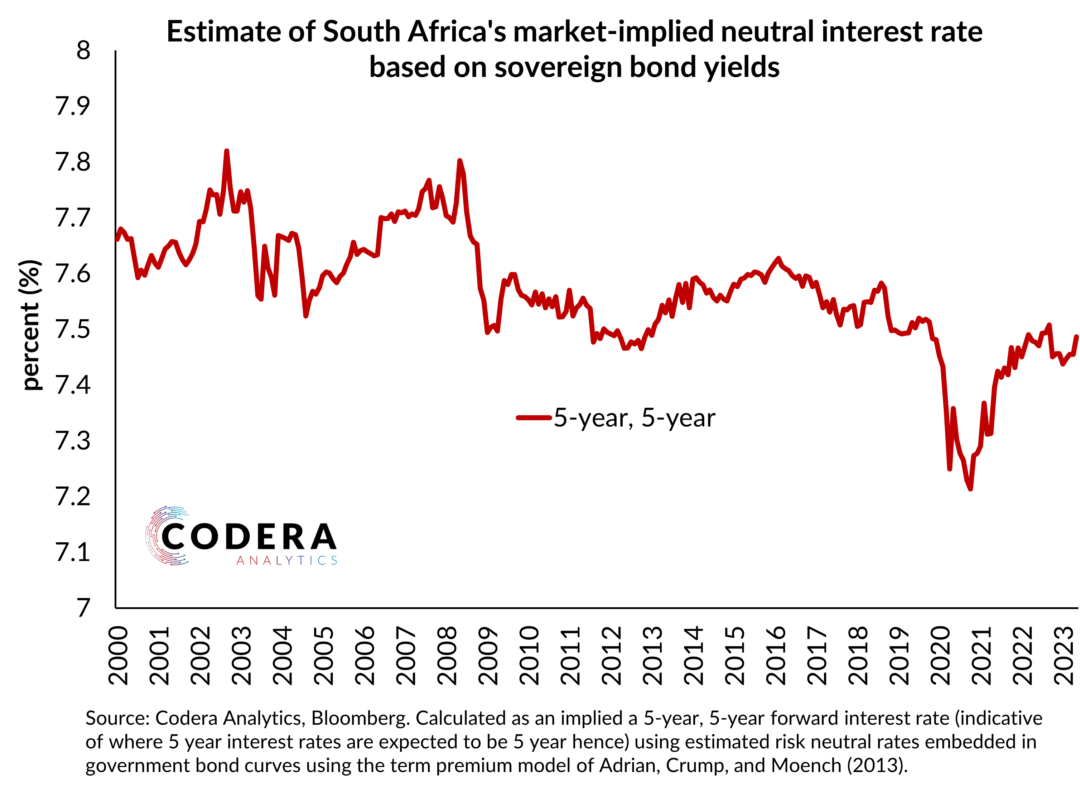

It is very surprising that there has been no structural modelling of the impact of load-shedding on potential growth and productivity in South Africa published after so many years of electricity constraints. Getting that estimate broadly right is very important for SARB: it impacts the assessment of the appropriate stance of monetary policy – that is, how much the SARB should be tightening rates in response to higher inflation. SARB estimates that our real interest rates is nearing neutral, but is still slightly accomodative. Market pricing has been quite volatile this year, but our estimates of where the market thinks rates will go over the longer-term in South Africa have been quite good at predicting SARB decisions over the last 6 months or so.

SARB quite rightly is concerned about the danger that the ongoing spike in inflation could lead to a de-anchoring of inflation expectations. They show in the Review that surveyed expectations of inflation of businesses has been increasing (now at 6.2 percent 2-years-ahead). But there are quite a few curiosities about their analysis, notably that it is unusual to present distributions of inflation expectations over single year periods, given how small the cross-sectional and time-series samples are. The historical distribution of inflation outcomes look quite a bit different from those presented based on survey expectations and one would really want to assess shifts in distributions using larger samples to ensure the results are representative. In a future post I will look at the distributions of SARB’s own forecasts and recent outturns for components of inflation, and assess just how broad-based inflation pressures have been (our CPI-common measure has been above core, and trend inflation has been picking up).

There are two boxes in the Review on forecast errors, yet there is no assessment of the structural drivers of these forecast errors using the models they use for forecasting. This makes it harder to judge whether SARB’s judgements have been credible and whether the stance of monetary policy has been appropriate over recent history.

The SARB also announced that a version of their QPM model with a fiscal block is on the way. This is a good thing – it will help SARB think through the implications of fiscal policy for the business cycle and inflation pressures, and they suggest that the updated model will provide more accurate forecasts of inflation. The benefits of the inclusion of a fiscal block would presumably be better storytelling abilities (such as providing richer explanations for wage or inflation pressures), and so it is curious that such analysis was not presented. The decision to adopt a new version of a structural model hinges on whether it provides a credible economic narrative about historical developments in the economy and hopefully the forthcoming paper will provide details on how well the new version of the model can explain growth and inflation and how different its assessment of the appropriate stance of policy is.

Finally, here are my suggestions for boxes for the next MPR:

- Implications of a shift to QPM 3.0

- What does the updated model imply for drivers of forecasts compared to the current version and therefore the appropriate stance of policy?

- Forecast error analysis from the perspective of QPM, i.e. what aspects of SARB’s assumptions and forecasts explain forecast errors for GDP and inflation?

- An assessment of the stance of fiscal policy given SARBs view of the business cycle, and implications for monetary policy.

- Implications of loadshedding for potential growth and the output gap

- Transmission of recent monetary policy tightening to market rates and the real economy

- Effectiveness of the implementation of the monetary policy under the new implementation regime