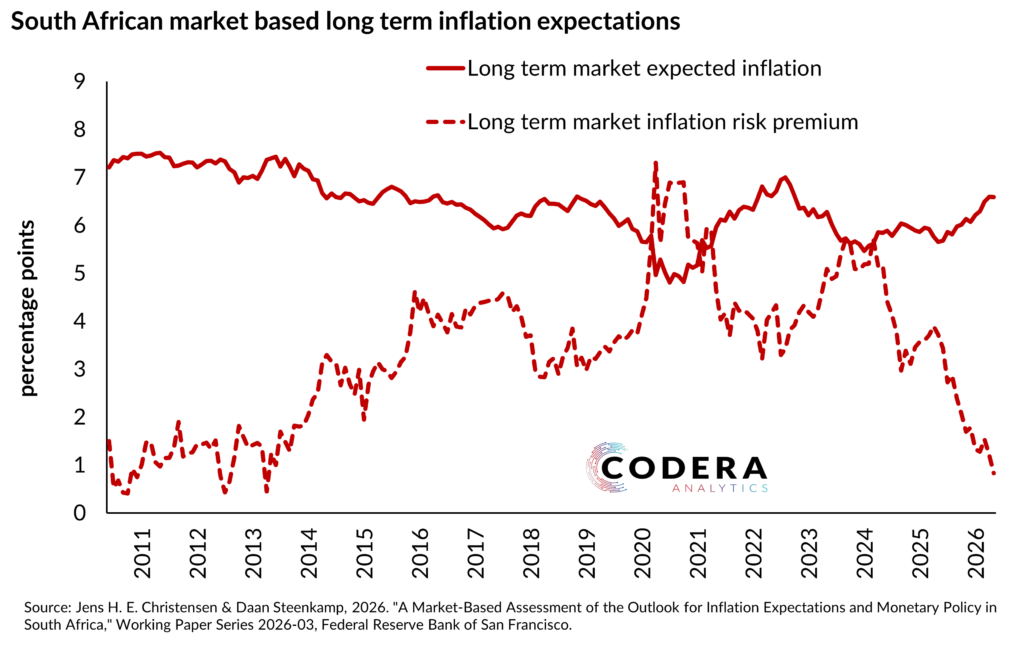

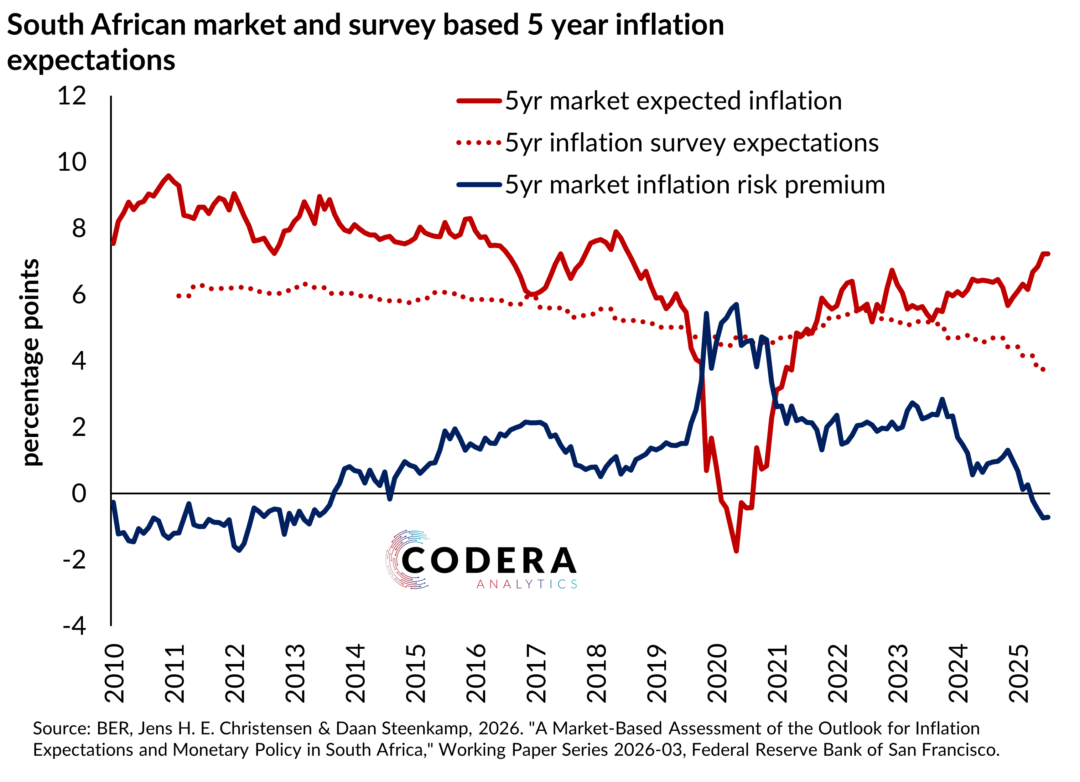

Despite the risk that inflation might remain well above target for the next several months, SARB and many economists still think rates could fall by year end. Market pricing, on the other hand, implies that the policy rate will continue to rise in 2026. What explains this divergence of views? Our estimates suggest that the market expects inflation to remain higher over the long term, with inflation expectations not as anchored as the surveys that SARB focuses on imply. Our analysis suggests that government borrowing costs have come down on account of lower sovereign credit risk, and lower inflation risk, not lower inflation expectations. This means that sustainably reducing inflation to the new target will require monetary policy to remain tighter for longer to re-anchor inflation expectations to a permanently lower level. This would also imply that the benefits of a lower target will be smaller over the next few years than SARB assumes, since borrowing costs continue to build in high inflation expectations.