The market expects the policy rate to rise further in South Africa in 2026, while the SARB and many market economists think rates could fall by year end. What explains this divergence?

While the median analyst that covers South African inflation and the SARB expect that inflation will return rapidly to the inflation target in 2027. Our estimates suggest that the market, on the other hand, expects inflation to remain higher over the long term, and that inflation expectations are not as anchored as inflation surveys suggest. When we use the entire shape of the nominal and inflation-linked bond curves to extract market-based inflation expectations and inflation risk premia, we find that market-implied inflation expectations have not declined since the announcement of a lower target. The estimates imply that sustainably reducing inflation to the new target will require monetary policy to remain tighter for longer to re-anchor inflation expectations to a permanently lower level.

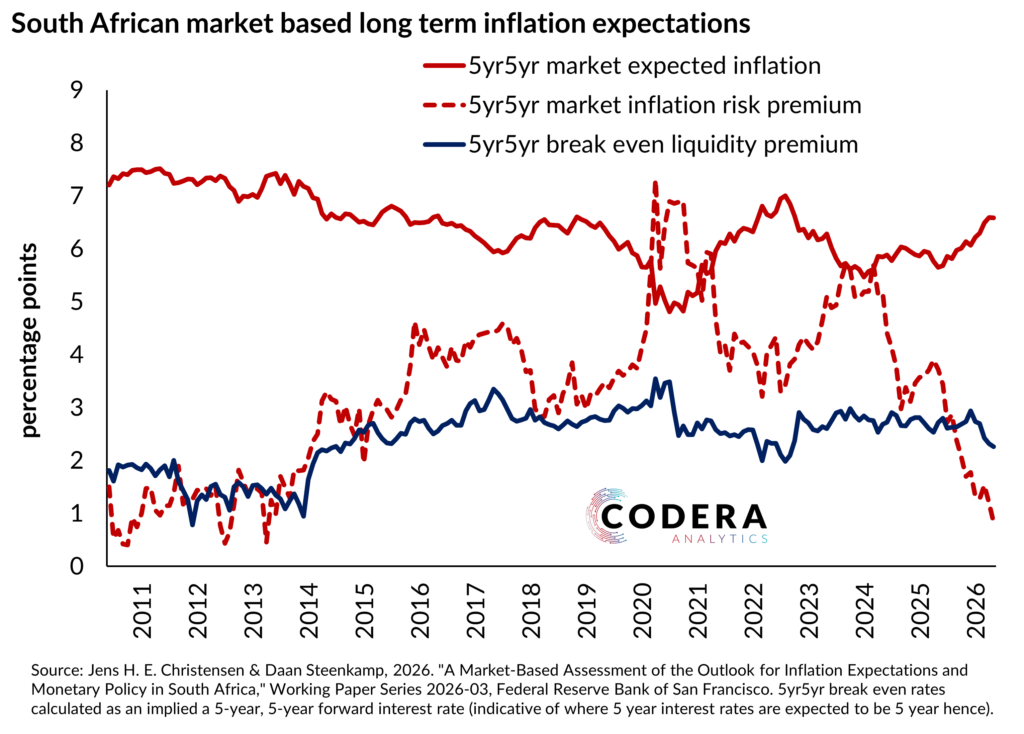

The credibility of the new inflation target is best judged by looking at a 5yr5yr horizon. The chart below shows that market-based expected inflation has not decline structurally for South Africa, but that inflation risk premia have. Inflation expectations are substantially higher in South Africa than in other emerging markets (see here for Mexico for a comparison when using the same approach).

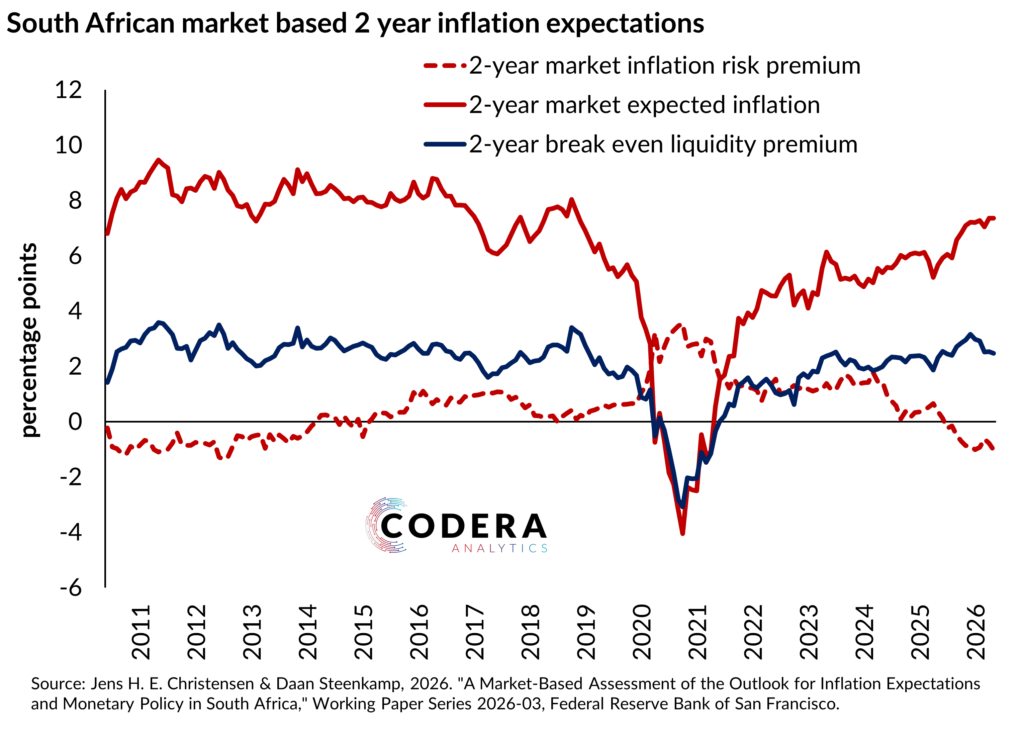

If we instead estimate the market-based 2-year expected inflation rate, we see the market expects medium term inflation to pick up by more than economists or the SARB expect. The large drop in 2020/21 reflects a sharp decline in yields from front-loaded monetary policy easing. These estimates suggest that SARB’s monetary policy stance is not as restrictive as survey-based inflation expectations might suggest.

Footnote

The SARB’s modelling ignores that there are liquidity differences between nominal and inflation-linked bond markets (see Box 6 in the October 2025 MPR, for example). The charts above suggest that there are large and time-varying liquidity premia that need to be accounted for when estimating inflation risk premia.