A new ERSA paper by Pirozhkova, Ricco and Viegi assesses the South African Reserve Bank’s (SARB) policy communication and the macroeconomic impact of its decisions. The authors argue that “policy decisions are often unanticipated and come to market participants generally as a surprise”. This is quite a controversial finding and raises questions about the measurement of policy surprises and policy communication in South Africa.

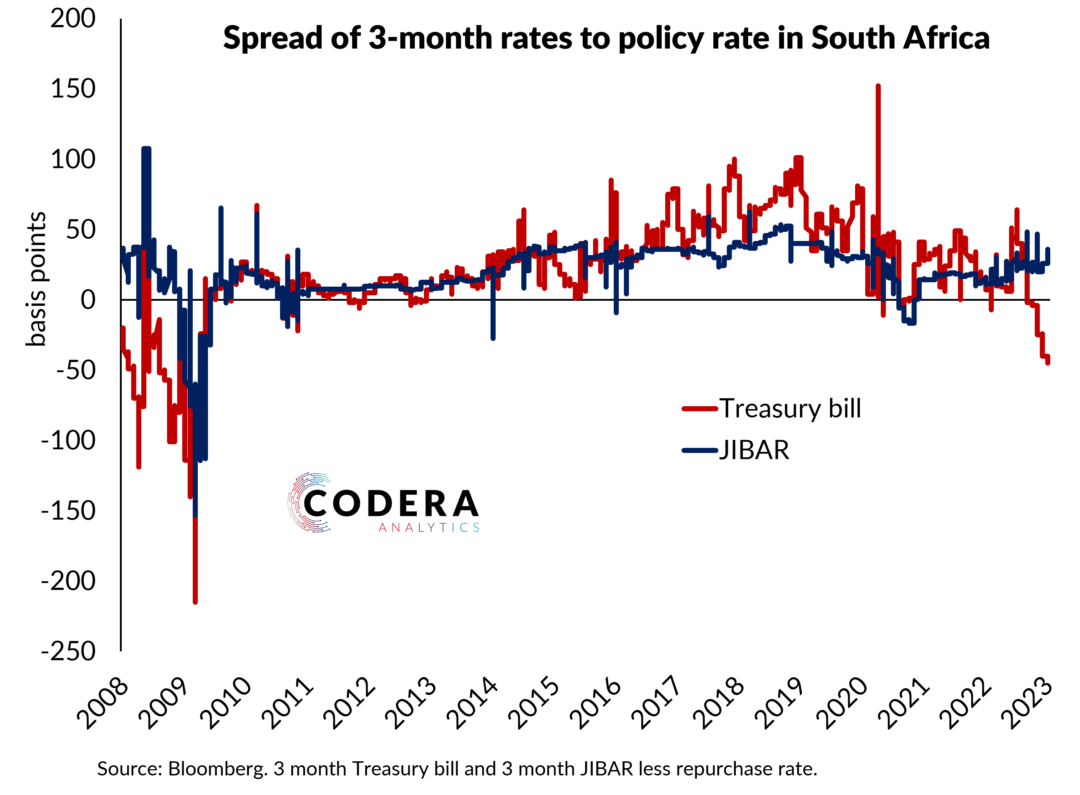

There are lots of ways to measure market expectations of monetary policy. There are also lots of problems with the market reference rates that are published in South Africa (here and here) and used by analysts to measure market expectations of the SARB’s next policy decision.

The authors use the changes on the day of a monetary policy announcement in the 3-month Johannesburg Interbank Average rate (JIBAR) references rate, forward rate agreements (FRA) and interest rate swaps at different horizons and the 5-year credit default swap (CDS) spread for South Africa to define policy surprises. Given the wide measurement window used, the authors’ measures of monetary policy surprises will also capture drivers of reference rates, the bond market, and CDS spreads beyond just the policy decision by SARB.

The way most analysts in South Africa measure monetary policy surprises is to use the difference between the 3-month JIBAR and a FRA rate corresponding to the date of a specific policy decision (see here for details). If one where to use this approach instead, one would find that there have been few meaningful monetary policy surprises since late 2017.

Said differently, most market participants would find the paper’s claims very surprising as market pricing has, on most occasions over the last decade, been in line with the policy decision by SARB’s Monetary Policy Committee (MPC).

However, this does not mean that policy guidance has been as good as it could be. One might argue, for example, that the MPC could still do a better job of explaining what underlies their projections and how they would react should different economic shocks occur.

Since the COVID-19 pandemic, there has been a vigorous debate about the appropriate role of forward guidance by central banks. It is a pity that the paper does not consider the last four years of monetary policy decisions as there has been several instances where policy projections diverged from actual MPC decisions (see here and here).

Footnote

It is worth noting the caveat that JIBAR and FRA rates could contain time-varying term premia that could make assessments based on the approach market participants use to gauge policy expectations slightly inaccurate. This is why the development of an active Overnight Indexed Swap (OIS) market and creation of a secured overnight reference rate in South Africa is so important. OIS contracts, if based on the an overnight rate such as the proposed South African Secured Overnight Financing Rate (ZASFR) that would track the SARB’s repo rate, would provide a direct measure of market expectations of future monetary policy decisions.