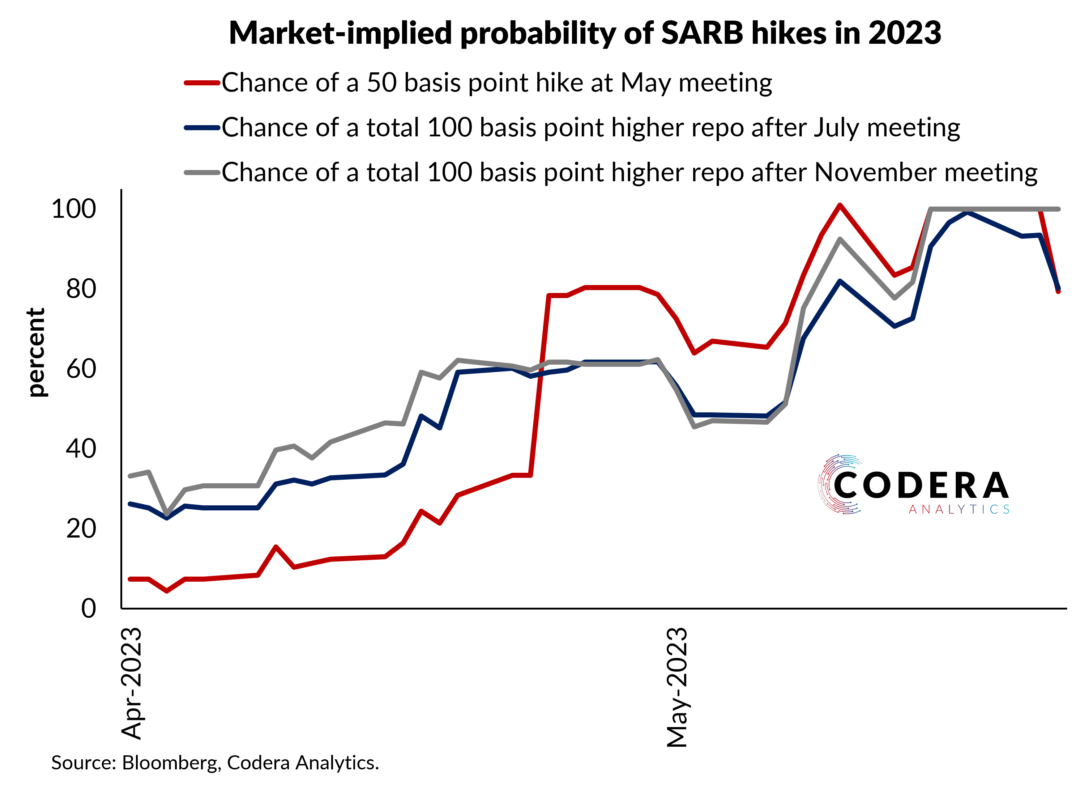

Yesterday’s 50 basis point hike did not surprise commentators. But what was surprising was that their forecasts still did not build in the observed higher policy rate. While the market has been pricing in further rate hikes, the Monetary Policy Committee (MPC) forecasts embed a 7.63% end of year policy rate (with the rate now at 8.25%). The market does not appear to agree with the SARB’s forecasts that assume that we have already seen the policy rate peak. The chart below shows that SARB’s published policy path has been much lower than the MPC has actually decided appropriate. The divergence was larger still in 2022, when the spike in global inflation caught SARB by surprise (as it did some other central banks).

There are many explanations for the divergence (see here for a discussion of the post-pandemic revisions). But as noted previously, it has taken SARB a long time to revise their judgements about the underlying trends in the economy. One would hope that the shift to a new version of QPM for the July meeting will be accompanied by closer alignment between the model’s historical and monitoring quarter implied policy rates and actual MPC rate settings. Publishing forecasts that are not based on the actual decisions made by the MPC creates uncertainty around the reaction function of the SARB (i.e. how the Bank will react to specific economic shocks) and makes it difficult for market participants to anticipate how interest rates might change over time. It is also possible that the ZAR spike following the announcement reflected some of this uncertainty, but this possibility warrants deeper analysis.

It is also puzzling that despite tighter policy than required by their forecasting model to get inflation to the midpoint before the end of the forecast horizon, SARB’s inflation forecasts are largely in line with market analyst forecasts. The large exchange rate depreciation over recent days creates a lot of upside risk to their inflation forecast, even if their forecasts have not fully reflected the April softening.

One would also expect that higher risk premia will be pushing up the market-implied neutral rate and we will provide an update of our neutral estimate next week to dig into this further. It will be interesting to see whether the QPM update is accompanied by updated trend and unobservables estimates.