Today’s blog post is an ungated version of a Business Day article in which we use real-time forecasts to explain fiscal slippage in South Africa and compare SARB, Treasury, IMF and Market forecast accuracy.

Why has South Africa’s fiscal position slipped?

Daan Steenkamp, Jan-Hendrik Pretorius and Lisa-Cheree Martin

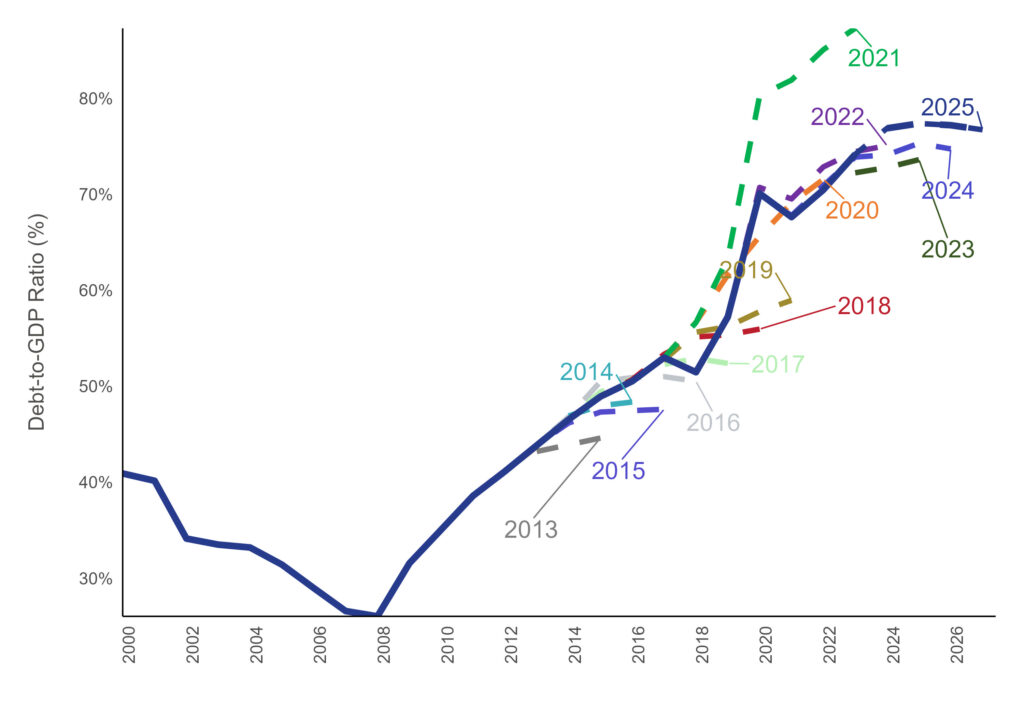

South Africa’s public debt has ratcheted up since 2008, more than doubling relative to the size of the economy, despite National Treasury forecasts that consistently predicted stabilisation. Was Treasury over-optimistic about the outlook for the economy, or did some spending categories grow much more than Treasury expected? Our analysis shows the answer is more nuanced than it might appear: what drove the slippage was a combination of macroeconomic surprises that caught every major institution off guard, and large, persistent spending overruns.

Figure: Historical National Treasury debt-to-GDP projections

Source: National Treasury, EconData

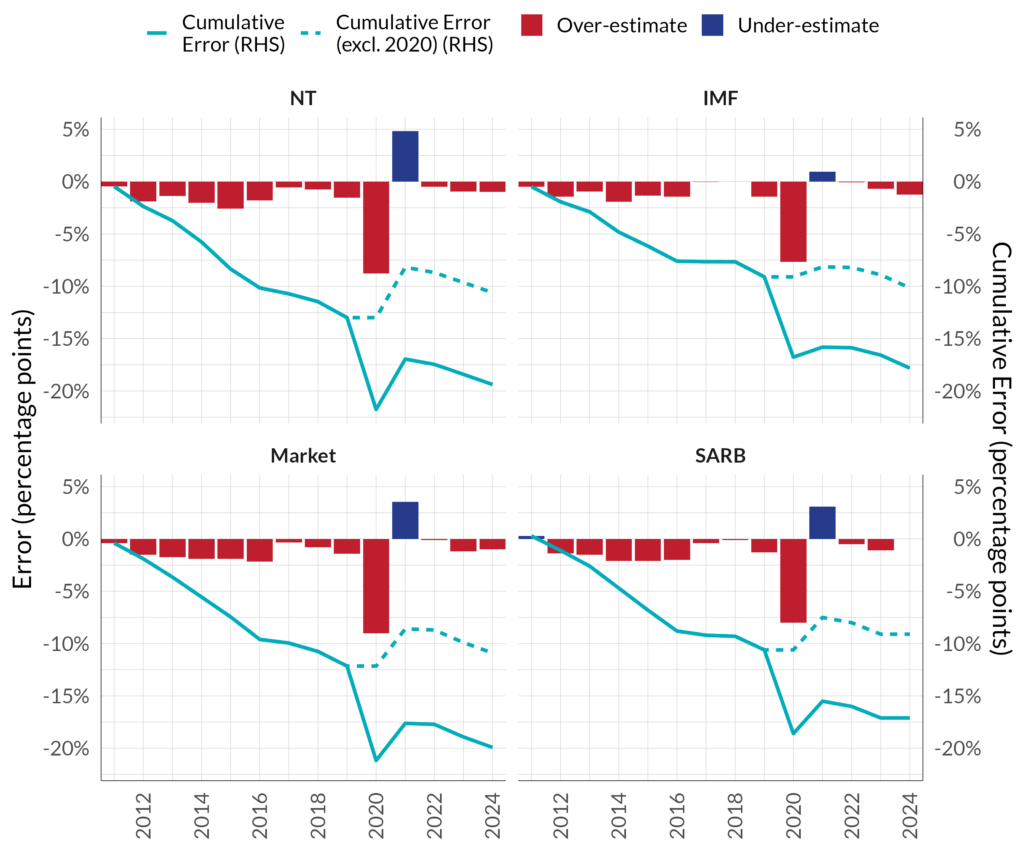

Since 2010, the Treasury’s growth projections tended to over-estimate economic growth, reflecting the difficulty of forecasting in an environment of recurring shocks and shifting structural constraints. Treasury’s forecasting errors for GDP growth were not, however, out of line with institutions such as the SARB or IMF, or those from the private sector. All three of these institutions and private sector forecasters were surprised by the decline in trend growth since the global financial crisis.

Figure: Comparison of one-year-ahead National Treasury, SARB, IMF, and private sector forecast errors for real GDP growth

Note: One-year-ahead forecast errors are computed as realised values minus the corresponding forecast for each vintage. IMF forecasts refer to the April World Economic Outlook. National Treasury (NT) forecasts come from the February Budget. Consensus forecasts reflect February expectations for each year. SARB estimates are from the January MPC forecasts. Source: National Treasury, IMF, Bloomberg, EconData.

Lower-than-expected growth saw tax revenues generally disappoint between 2016/17 and 2020/21, despite a brief improvement owing to unexpectedly high commodity prices for in 2021/22 and 2022/23. Effective tax rates also increased over time, driven by an increase in the VAT rate to 15 per cent in 2018/19 and a below-inflation adjustment in personal tax brackets over time.

But weaker revenues were only part of the story. A major driver of the sustained rise of public debt was expenditure overruns. Before the COVID-19 pandemic, the largest contributor was unplanned support of state-owned enterprises such as Eskom, and the announcement of free higher education. Since the COVID-19 pandemic, total public expenditure has consistently increased by more than Treasury projected, despite a significant slowdown in the growth of government expenditure across major components of spending. Large unplanned spending, including free higher education and social relief of distress grants, and unexpected borrowing in support of state-owned enterprises, were the most important contributors to larger-than-expected borrowing requirements over this period.

A key exception to a general pattern of overspending in major government spending components was capital expenditure. There has been persistent decline in the share of government investment in total investment, with the national investment rate falling towards pre-democracy lows since 2010. This matters because sustained underinvestment in infrastructure feeds directly into the structural constraints that have slowed economic growth, the same growth shortfall that has driven revenue disappointments over the same period.

The compounding effects of past policy decisions on the fiscal framework over time is best summarised in the impact on cumulative debt service costs that government has had to pay. Between 2011 and 2024, government had to pay over R2.5 trillion in unexpected debt service costs. This is more than 20 times what government spends on policing per year.

The implication of slower economic growth than Treasury expected was that attempted fiscal consolidation undertaken since 2010 was not sufficient to stabilise debt. Fiscal forecasts can be highly uncertain as predicting the outlook for the macroeconomy and future government decisions can be difficult, if not impossible. Another complication is that fiscal projections are intended to provide a signal about the fiscal authority’s framework and policy plans, which are subject to changes in government or policy positions. Our analysis shows that discretionary budget decisions, and differences between fiscal plans and their implementation, have had a significant impact on the fiscal position over time.

To make fiscal projections more resilient to macroeconomic shocks and consistent with debt stabilisation, we recommend regular evaluations of the National Treasury’s assessment of the state of the business cycle, reviews of forecast errors and risks around projections, and longer-term fiscal scenario provision. Another area to consider is enhancements to fiscal planning processes, such as regular post-budget evaluations and independent reviews. Stricter requirements for deviations from medium-term expenditure allocations, additional oversight mechanisms, or reforms to state owned enterprise support arrangements would also help to strengthen fiscal institutional arrangements further. The Treasury is expected to publish details of fiscal anchors at the Medium-Term Budget Statement later this year.

This article is based on Southern Africa — Towards Inclusive Economic Development (SA-TIED) Working Paper 297: ‘Understanding fiscal slippage and fiscal forecast errors in South Africa‘ by Jan-Hendrik Pretorius, Lisa-Cheree Martin, and Daan Steenkamp.”