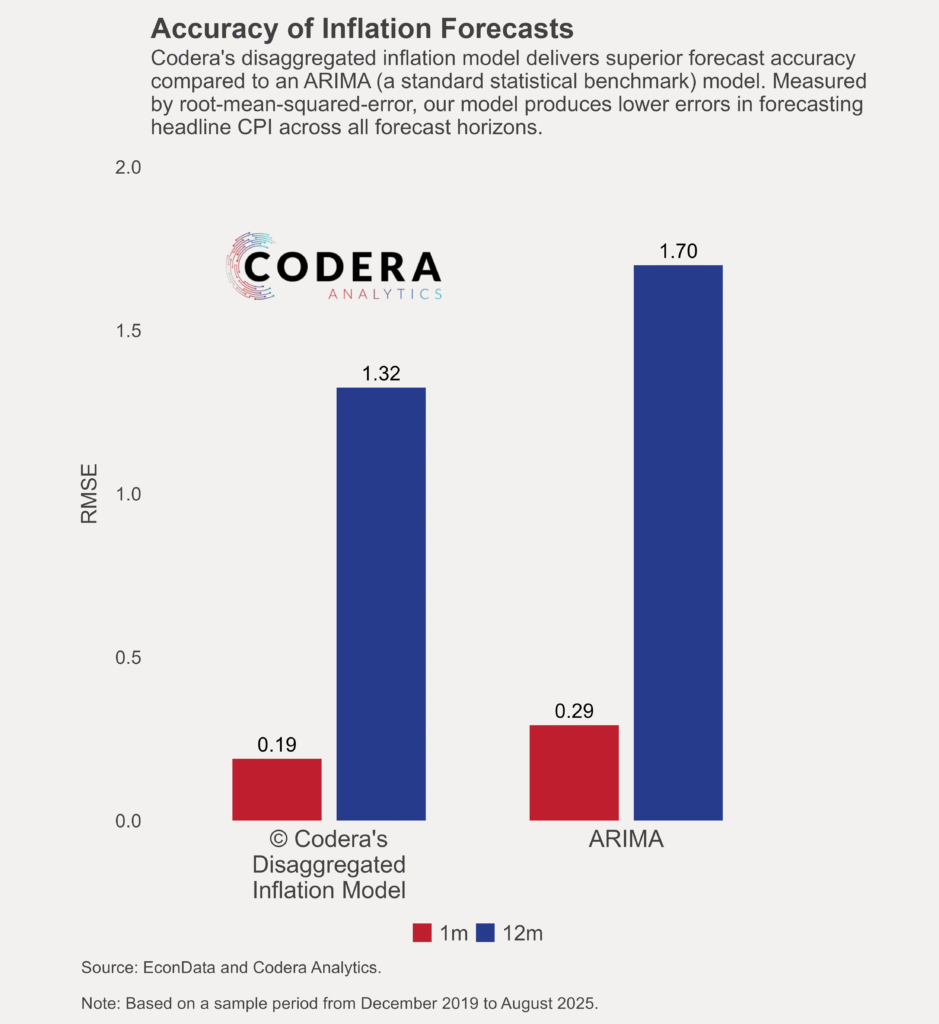

Today’s post by Oliver Guest shows that Codera’s disaggregated inflation model is more accurate at out-of-sample inflation forecasting over the short term (1 month ahead) and over the long term (12 months ahead) than benchmark statistical models.

Note that this comparison on purely statistical forecasts – Codera also improves statistical forecasts by applying judgements to incorporate off-model information, such as electricity tariff changes or within-month price changes using web-scraped information. Though the sample used in this post is not comparable directly to our earlier forecast accuracy assessments of SARB’s forecasts, these forecasts compare favourably, even though they are not based on Codera’s official forecasts.