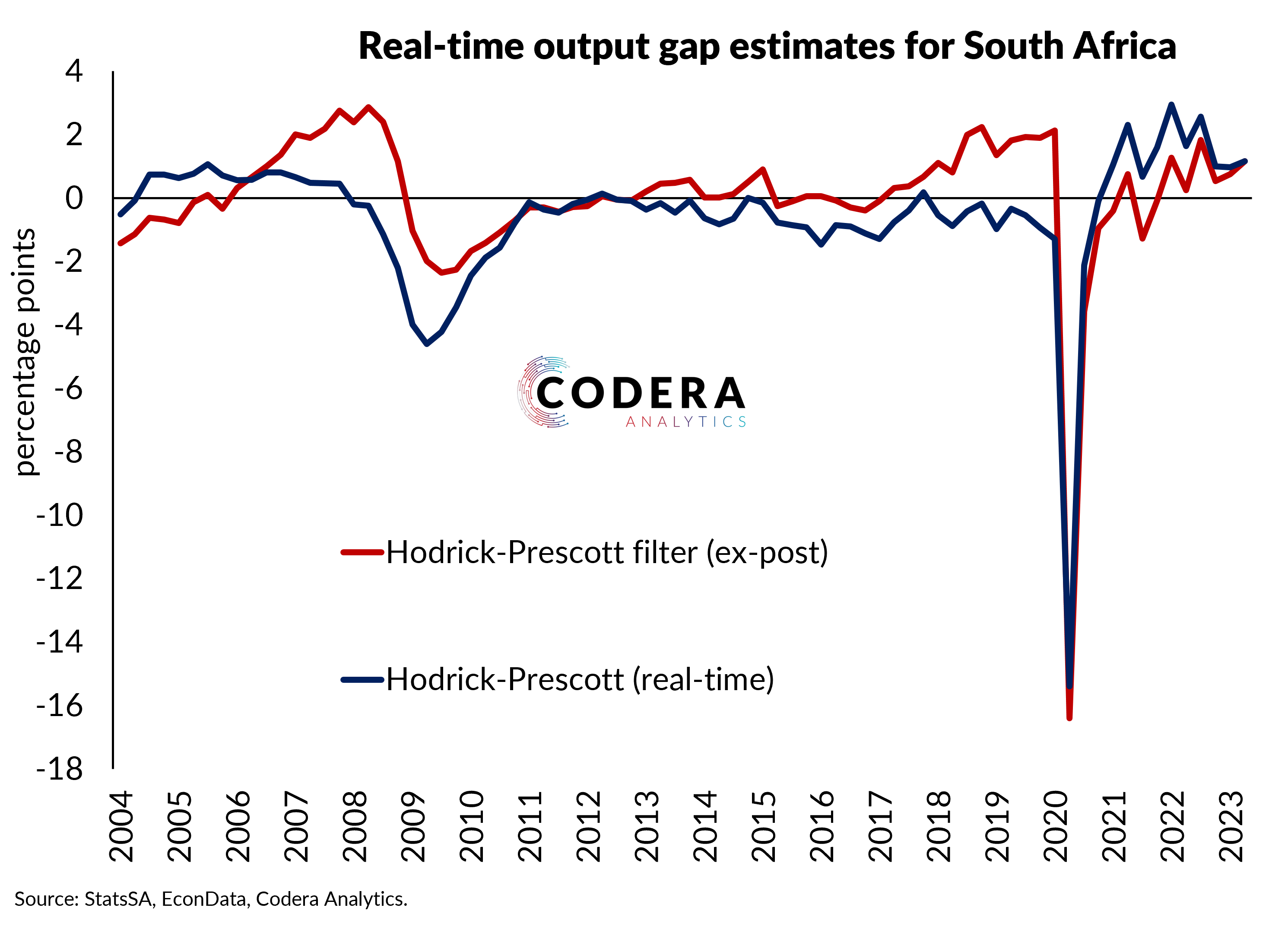

Since the concept of economic slack cannot be observed directly we have to estimate it, i.e. there is no ‘true’ output gap at a given point in time. Many statistical filters used to estimate the output gap are afflicted by the ‘end-point problem’ that makes estimates at the estimates at the end of the sample subject to revision as new data becomes available. GDP data are also revised, which means that the same estimation technique might produce different estimates when revised figures are available. This post assesses how a commonly used statistical filter, the Hodrick-Prescott (HP) filter’s output gap and potential growth estimates for South Africa have changed with new data and data revisions.

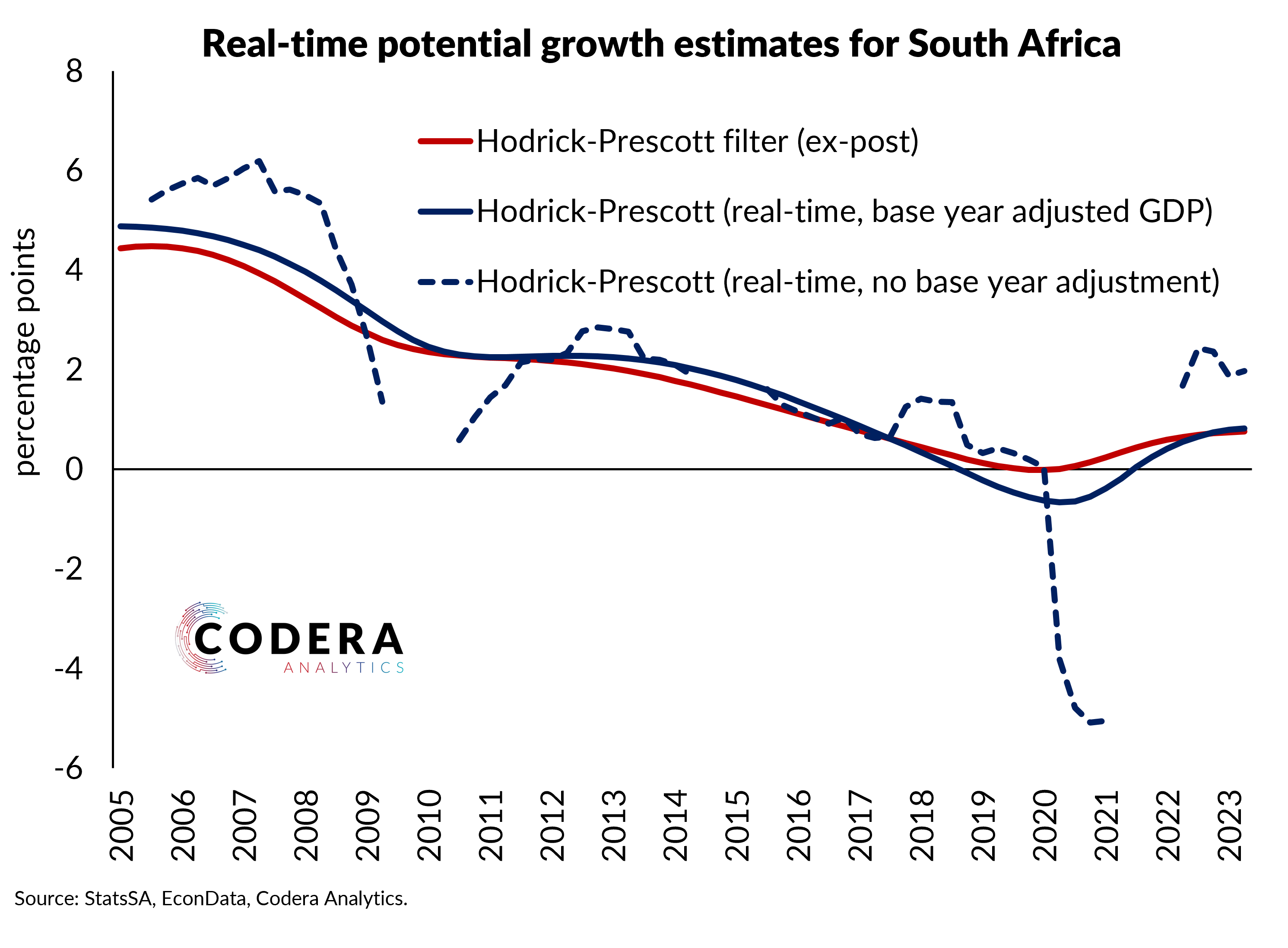

With a longer data sample, an HP filter now implies that there more capacity pressure in the lead up to the global financial crisis (GFC) of 2008/9 and ahead of the COVID-19 pandemic 9 (‘ex-post’ estimates). This reflects the fact that such a filter tends to ‘look through’ very abrupt changes in GDP, so that it attributes more of a large change in GDP to a change in capacity constraints in the economy. An HP filter using data available at the time (‘real time data’) suggested that South Africa’s potential growth was higher between 2005 and 2018 than such a filter now implies with updated data. Since the pandemic, the revised potential estimates from the same technique are higher than with real-time data.

The decline in trend growth surprised SARB, National Treasury and the IMF and has seen these institutions revise their estimates down over time (see here). The filter suggests that potential growth has been falling over the last decade. It also suggests that the under-utilised capacity built up during the COVID-19 pandemic has dissipated. So despite the slow growth of the economy, the filter implies that there may be mild demand pressures acting on prices. The most recently published SARB assumptions (from the July 2023 MPC) imply that SARB sees economic growth to be largely in line with potential in 2023 (though their output gap estimates are slightly negative).

What might the implications be of potentially under-estimating how much potential growth fell following the pandemic? For monetary policy, it implies a risk of over-estimating the amount of under-utilised capacity in the economy. If taken literally by policymakers, these estimates imply a risk that monetary policy might have being too accommodative (i.e. rates too low) if the output gap was indeed judged to be more negative in real-time. For fiscal policy, policy may have been too ‘loose’ given more-limited under-utilisation of capacity than previously thought.

There is an active debate at the moment about whether more aggressive fiscal consolidation might be needed to balance the books in South Africa. Hopefully, this post helps to demonstrate the difficulty of assessing how much fiscal adjustment might be needed to stabilise the fiscal position at a given point in time, given the difficulty in accurately assessing the state of the economy and its implications for revenue and expenditure in real-time.

Footnotes

This analysis is based on ‘true’ real-time estimates taken from historical vintages of data published by Statistics South Africa. Given base year changes in GDP, the potential growth estimates are based on base year adjusted estimates of GDP (from Codera) for illustrative purposes, but estimates without a base year adjustment are also presented. Our EconData platform makes it possible to easily produce and update this type of analysis for publicly available macroeconomic and financial data.

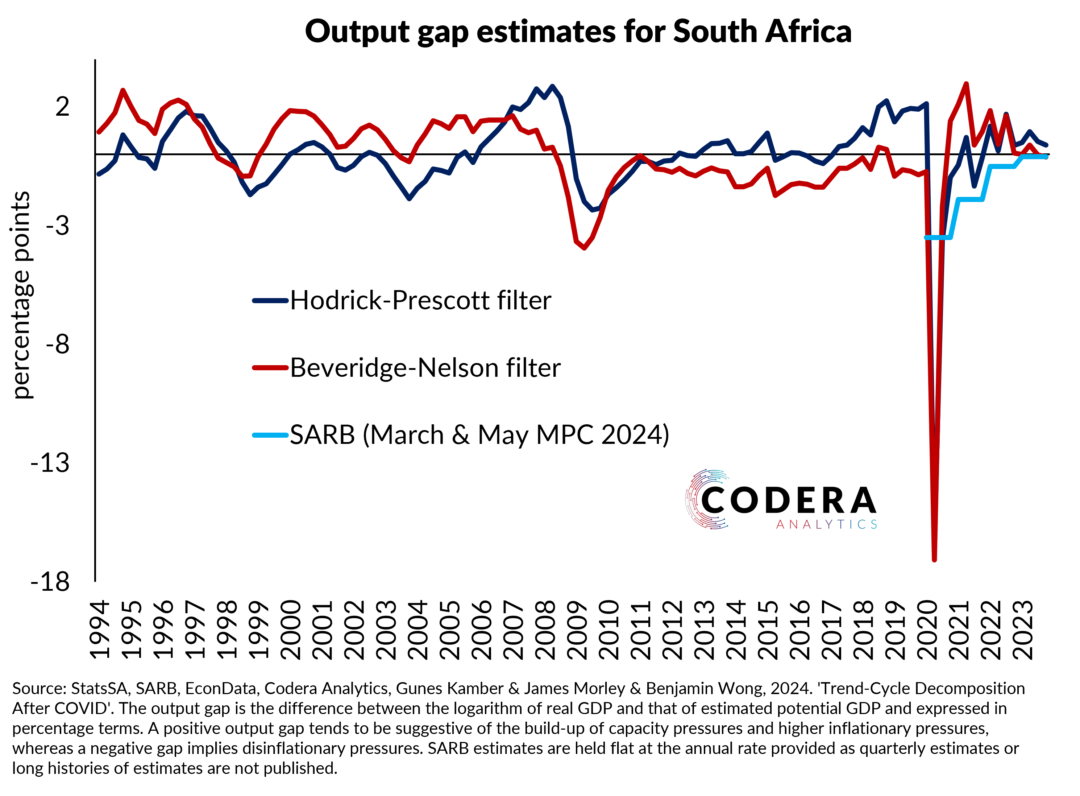

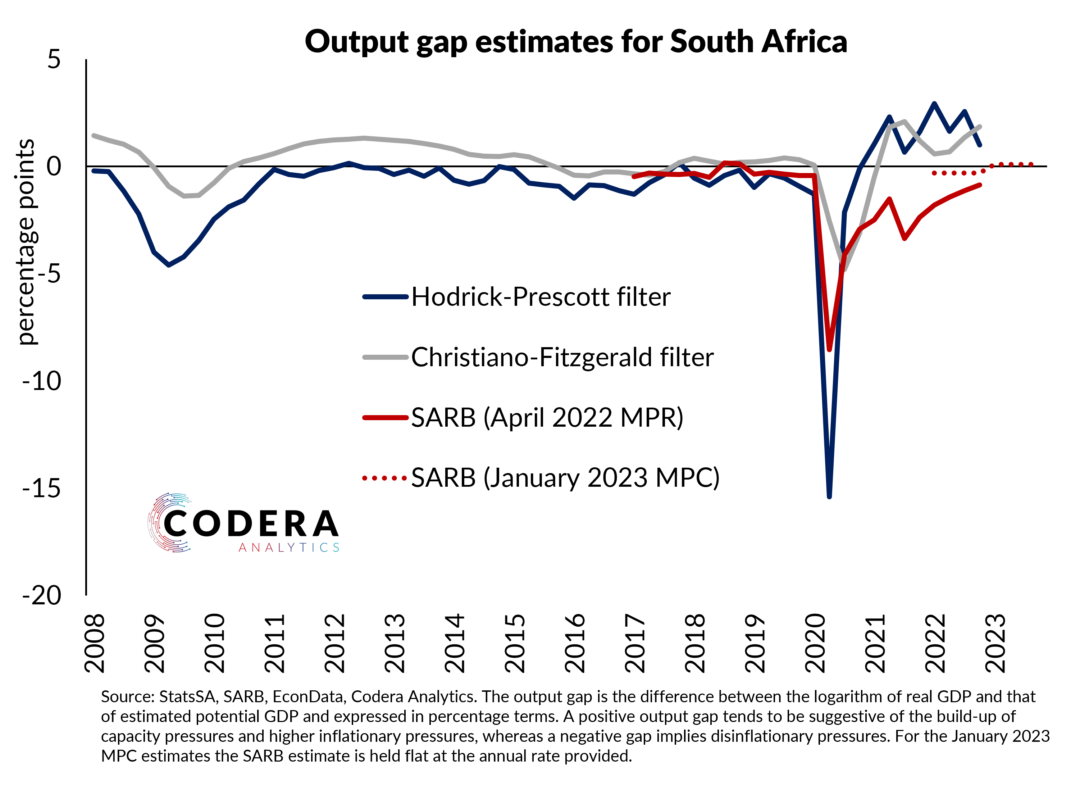

Note that the HP filter is a commonly used statistical approach for output gap estimation. The problem with simple filters such as the HP is that they are not well suited to interpreting the economic impact of the COVID shock. That said, they are a useful benchmark to compare more sophisticated approaches against.