Whether now is a good time to lower South Africa’s inflation target depends, amongst other things, on whether the economic costs of doing so are worth bearing.

In a recent speech, the Reserve Bank Governor argued that the costs of disinflation in South Africa have generally been low, attributing this to the SARB’s credibility and effective communication. This perspective is based on the notion that the Phillips curve in South Africa is relatively flat and that inflation expectations are firmly anchored.

We suggested in earlier posts (see here and here) that inflation expectations may not be as well anchored as the SARB assumes, while we presented estimates from the IMF and from an earlier SARB paper that suggest that the Phillips curve is steeper than SARB assumes and therefore that the costs of shifting to a lower inflation target might be higher than implied in the Governor’s speech.

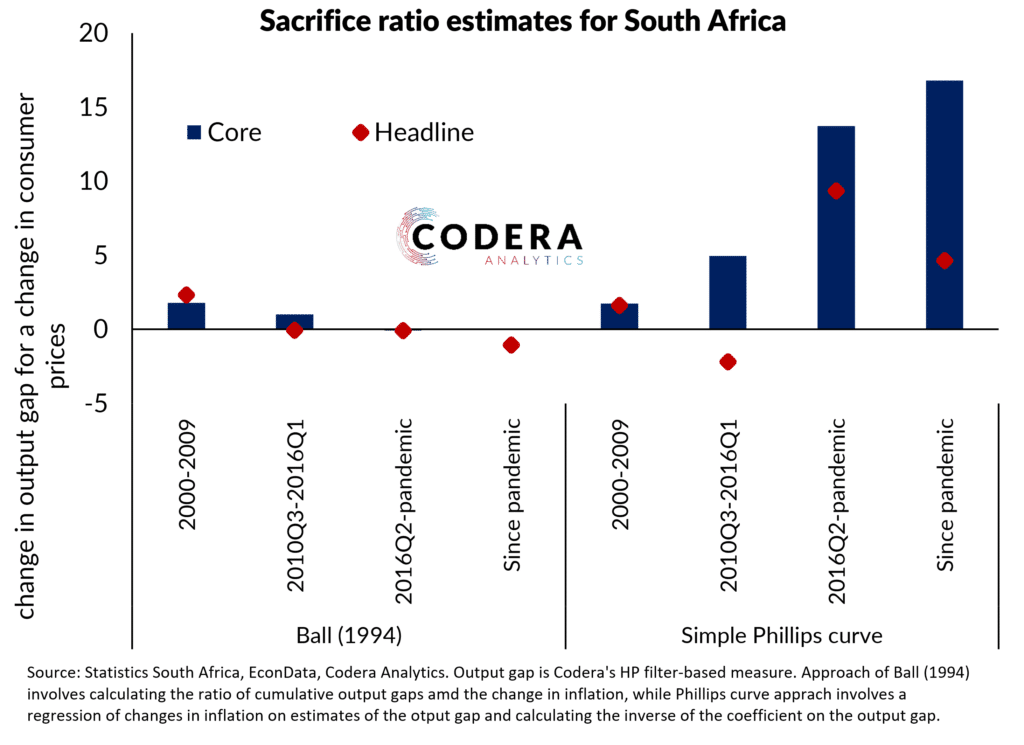

In today’s post we present some simple estimates of the sacrifice ratio for South Africa that captures the extent to which lower inflation requires the sacrifice of output. The challenge with sacrifice ratio estimation is that it is highly sensitive to the sample period used, the theoretical framework and estimation approach used, as well as the measure of the output gap (a measure of economic slack) that is used. One will also tend to find differences between estimates based on headline and core (underlying) inflation, given, for example, differences in how they are affected by supply shocks. The post shows that there is therefore considerable uncertainty around estimates of the sacrifice ratio.

The chart below compares sacrifice ratio presents estimates based on capacity pressures measured using a commonly used approach (the HP filter) and assessment of changes in inflation over similar sub-samples to those used in the SARB analysis referenced in the Governor’s speech. We show that the estimates would align with the SARB’s take that the sacrifice ratio has been near zero over recent years when using the simple approach advanced by Ball (1994), which cumulates output gaps and inflation over selected periods.

On the other hand, Phillips curve models (which relate the output gap and inflation pressures) tend to suggest that South Africa’s sacrifice ratio is higher than assumed by the Governor. South Africa’s post global financial crisis (GFC) inflation experience has been marked by a global supply shock-driven decline in inflation, along with inflation volatility driven by exchange rate, oil price and food price shocks. At the same time, capacity pressures (pandemic period excluded) have been modest compared to the pre-GFC given our low rate of economic growth.

Note that the estimates in the chart below are meant to be illustrative: in our opinion, Phillips curve models should also account for time variation in the relationship between capacity pressures and inflation (as discussed here), and things such as unit labour costs and inflation expectations (as we did in this earlier paper).

This is not to say that South African policymakers should not be considering lowering the inflation target. But the structure of the economy, the measurement of the target, the stance of fiscal policy and the commitment of government to a lower target affect the economic costs of lowering the target and the ideal timing of a policy change.

There is much less of a consensus around the optimal inflation target than some of our policymakers like to suggest and the policy debate in South Africa needs to take these uncertainties more seriously.