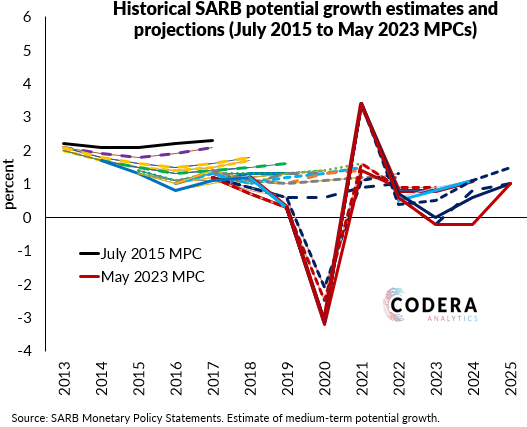

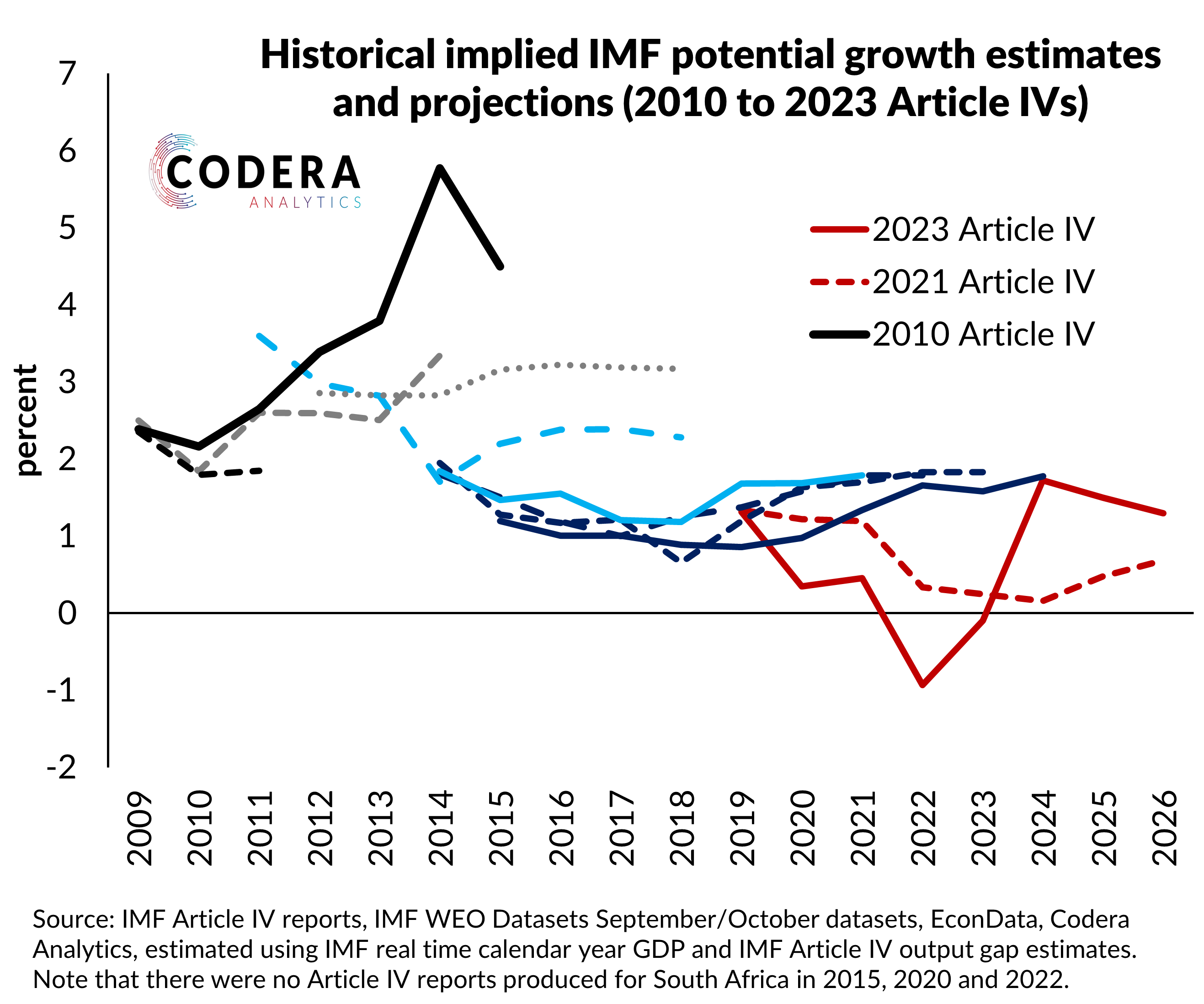

The SARB has progressively lowered its estimates of potential growth since it first began publishing its estimates. The same has been true of the IMF’s view of the economy’s underlying trend of growth (backed out below using their real time output gap and WEO real GDP estimates). However, the IMF’s latest projections (published June 2023) imply a slightly more pessimistic view of the potential growth rate of the economy than that of the SARB for 2022, but a more optimistic estimate from 2024 onwards.

Footnote

Note that the IMF and SARB estimates are based on slightly different definitions, with the SARB estimate reflecting a medium term concept, whereas the IMF estimate presented here is their implied estimate of the underlying trend growth of the economy at a particular point in time. The annual real GDP growth rates from the WEO are identical at first decimal to the rates from the Article IV 2023, suggesting the use of the WEO real GDP data will not meaningfully affect the accuracy of the implied potential growth estimates I have backed out.