The output gap (a measure of economic slack) is used, amongst other things, for estimating the impact of capacity pressures on the inflation outlook. Today’s post shows that the passthrough of the output gap to headline inflation peaks with a 2 to 3 quarter lag, while its impact peaks at a 3 to 4 quarter lag in the case of underlying (core) inflation in South Africa. The economic rationale for delayed impacts of capacity pressures/slack to inflation is that there are many economic rigidities that slow price setting adjustments down, including gradual adjustments in labour and product markets, and slow adjustment in inflation expectations (here and here). Positive correlations at shorter lags suggest that inflation responds quickly to economic slack or overheating, while significant correlations at longer lags indicate a delayed effect of output gap changes on price levels.

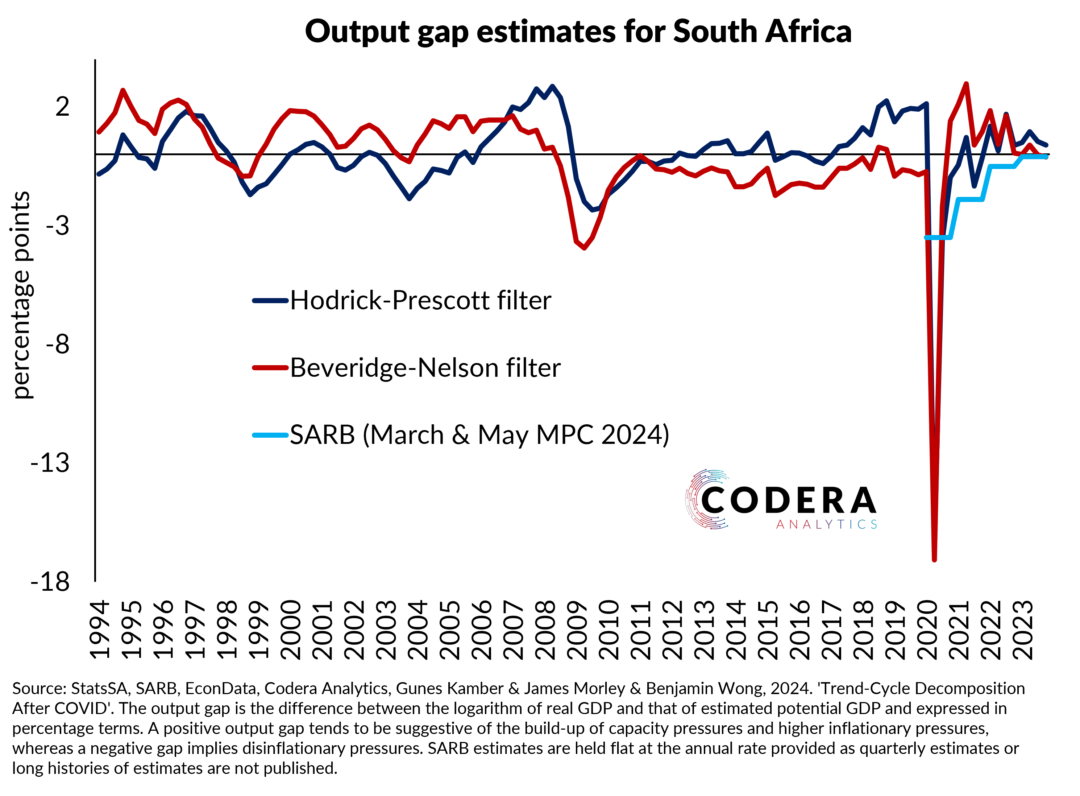

We showed in an earlier post (update coming next week), that there are several statistical problems with SARB’s output gap estimates that undermine its usefulness in economic forecasting and understanding inflation dynamics. The main problem is that their estimates imply that there has been persistent economic slack for around 15 years. This is inconsistent with the statistical definition of an output gap, which implies that eventually economic excess capacity is eliminated.

SARB does not publish quarterly estimates for the output gap, so it is not possible to compare our estimates to their estimates directly. Note that their annual estimates likely overstate the correlations obtained in the chart below. Our quarterly analysis suggests that the passthrough to underlying inflation of capacity pressures peaks may be very different from what SARB’s estimates imply about the macroeconomic consequences of economic slack. SARB currently assumes that there has been a small amount of excess capacity in South Africa, contributing to some deceleration of inflation, while our estimates suggest that there is, despite low growth, evidence of a build-up of capacity constraints that may be expected to push up inflation in future.

We showed in an earlier paper that estimates based on the same approach used here out-performed SARB’s output gap estimates at predicting GDP and inflation in models specified in line with SARB’s QPM. If you believe our estimates, SARB will need to revise its estimates in 2025 and may also need to re-calibrate its QPM forecasting model.