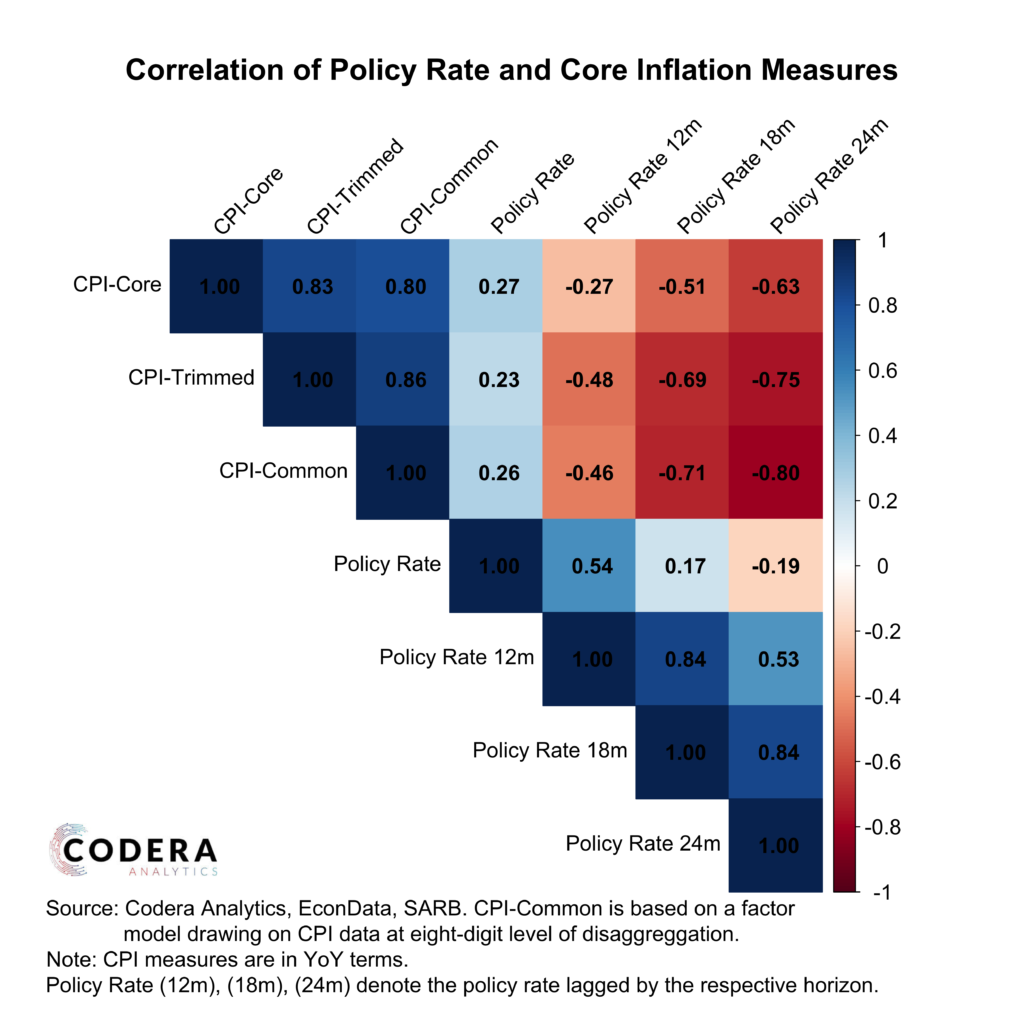

Today’s post by Jurgens Fourie looks at the correlation between the SARB policy rate and core Inflation measures at different lag horizons. The contemporaneous correlation is weakly positive since SARB tends to respond to rising inflation if there is a risk of breaching the inflation target. However, as the lag extends, the relationship inverts. By 18 months, correlations reach -0.51, -0.69, and -0.71 across Core CPI, CPI-Trimmed Mean, and Codera’s CPI-Common measure, consistent with the SARB’s assumption that the monetary policy large is between 12-18 months. The correlation strengthens further at 24 months, reaching -0.63, -0.75, and -0.80 respectively, indicating the transmission effects may persist beyond the conventional 12-18 month window. The strengthening negative relationship at longer horizons suggests policy does eventually dampen inflation, but with a considerable delay.