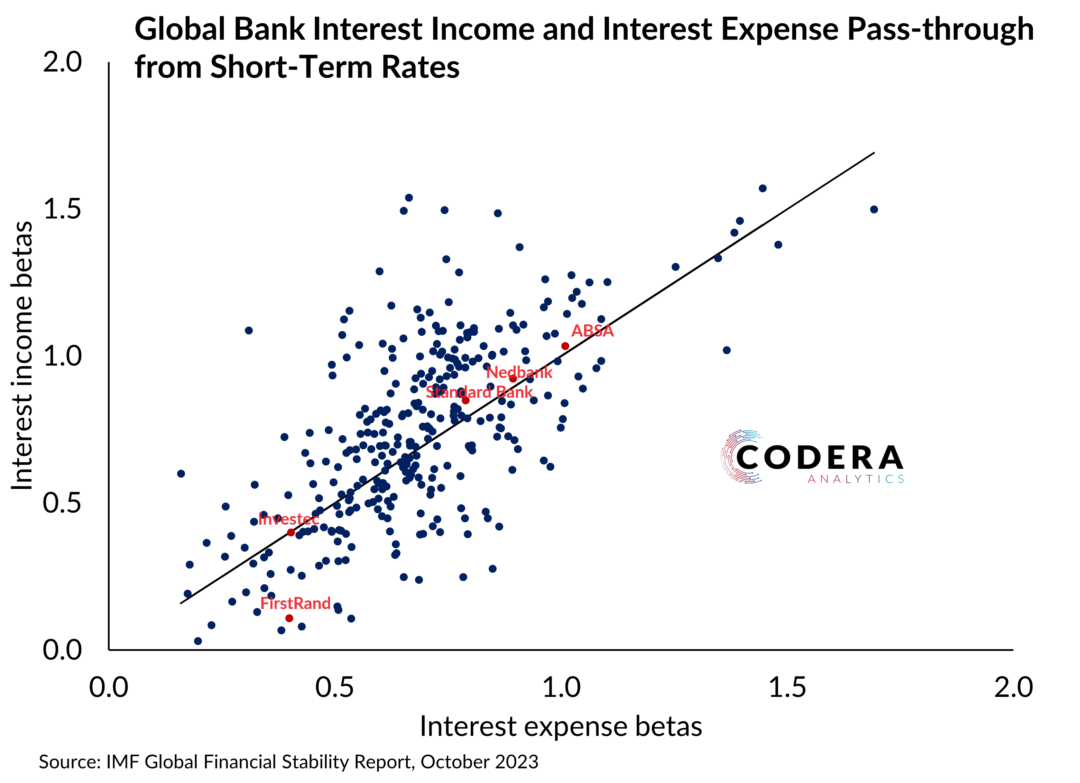

Our paper that assesses the degree to which changes in the SA policy rate are passed through to individual bank lending and deposit rates is now available in the Journal of Macroeconomics. We show that rate hikes are typically passed through to mortgage interest rates completely while rate cuts are not. This asymmetry is more prevalent for household than corporate mortgages. Pass-through to household and corporate call deposit interest rates is typically complete, but cheque account interest rates are highly sticky and experience weak pass-through. Our results indicate that banks’ pass-through decisions often impose greater costs on households than firms, and may blunt the stimulatory effect of rate cuts by weakening their impact on debt servicing costs and the remuneration of deposit balances.

Harness your data