Today’s blog post is our Business Day article in which we discuss why South Africa benefits less from commodity windfalls than other commodity exporters and argue that SA has government-induced Dutch Disease.

Why commodity windfalls don’t trickle down in SA

South Africa’s terms of trade are near multi-generational highs. The terms of trade measure the prices of the goods and services South Africa exports relative to the prices of goods and services that we import. Higher terms of trade usually make a country wealthier by boosting what can be bought from the rest of the world with what is domestically produced.

But the recent IMF World Economic Outlook report shows that, unlike many commodity exporters, the wealth effects from higher commodity prices are negative in South Africa.

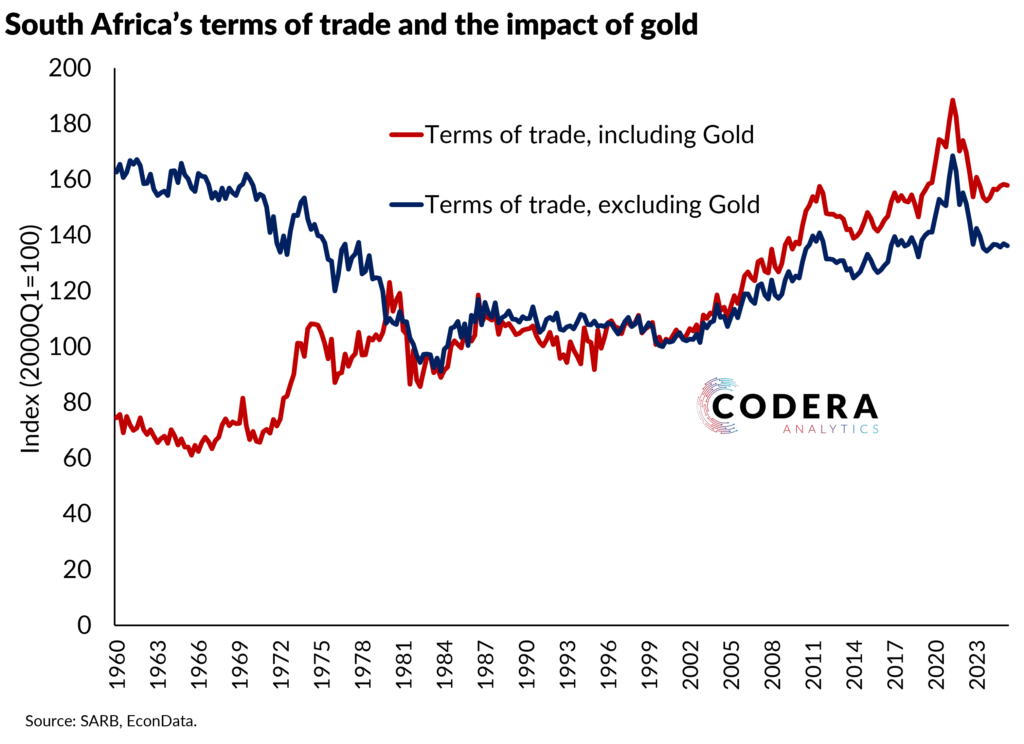

There are several reasons why commodity windfalls have not trickled down in South Africa. The first reason why South Africa has not benefitted from the boom is that conventional terms of trade measures likely overstate the actual gains from higher prices. As the figure above based on the Reserve Bank’s terms of trade indices shows, gold has played an important role in the long-term increase in South Africa’s terms of trade. But if gold is excluded from the calculation, our terms of trade are down compared to the 1960s. Gold exports are also much less important now, with volumes declining significantly over the last two decades.

Alternative measures suggest that South Africa’s term of trade boom might have been much more modest than standard measures suggest. The IMF’s commodity terms of trade measure suggests that South Africa’s terms of trade are back to 2000 levels and never jumped nearly as much as for Australia or Canada.

If one instead measures terms of trade based on the level of export and import prices (with prices expressed based on actual price levels instead of indices) South Africa’s terms of trade are up around 15% since 2000, compared to over 50% based on the Reserve Bank’s measure.

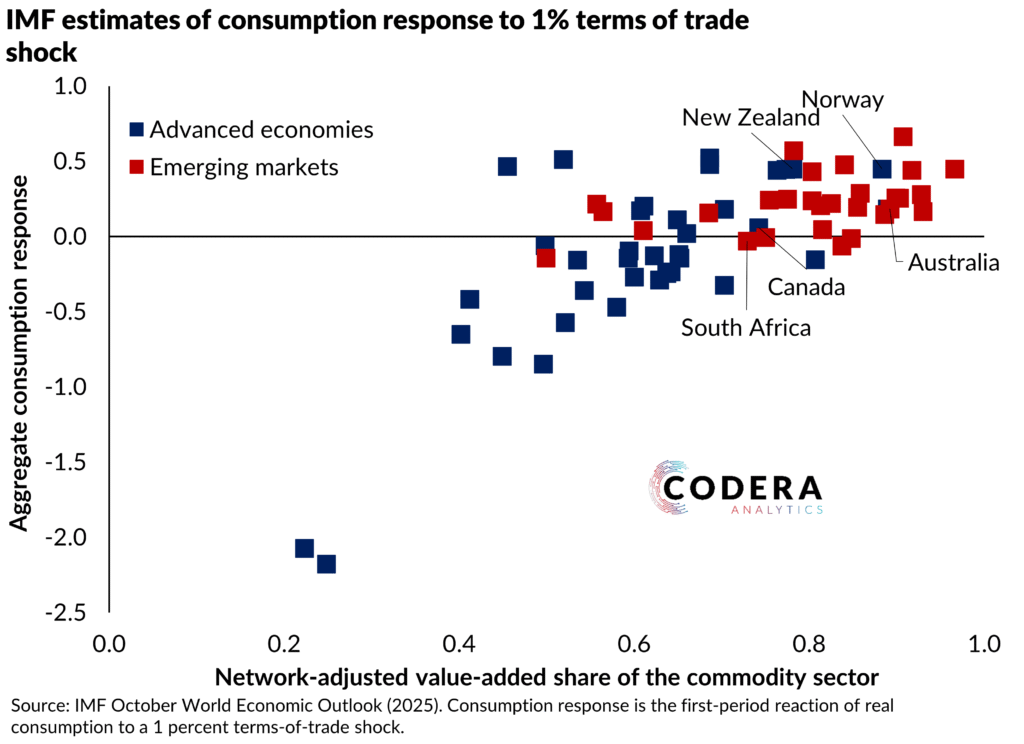

The second reason South Africa has not benefitted as much from the commodity boom as other net commodity exporters is that our commodity-related industries are not well connected to the rest of the economy or the rest of the world. Countries where the commodity sector is more interconnected tend to see stronger effects of commodity price changes on the economy.

South Africa is not well integrated into global value chains compared with major economies. This limits the extent to which South African firms benefit from faster growth in major emerging markets. IMF estimates show that Indian and Chinese firms experience, respectively, 25- and 20-times bigger revenue growth impacts from faster G20 emerging market growth surprises than South African firms.

The IMF estimates show that the links between domestic industries in South Africa are also weaker across all industries than is typical in major economies. Likewise, our estimates show that the primary sector in South Africa uses fewer domestic manufactured inputs than the sectors such as construction and telecommunication.

Despite extensive state support, South Africa is ‘beneficiating’ less and less of its mining products, with decreased transformation of mined resources into higher value added manufactured products.

When it comes to what South Africa exports, the Harvard Growth Lab and the Observatory of Economic Complexity measures show that the sophistication of our products have been declining over time, as a result of increasing reliance on raw commodity exports. Fast growing emerging markets such as China and India have achieved the opposite.

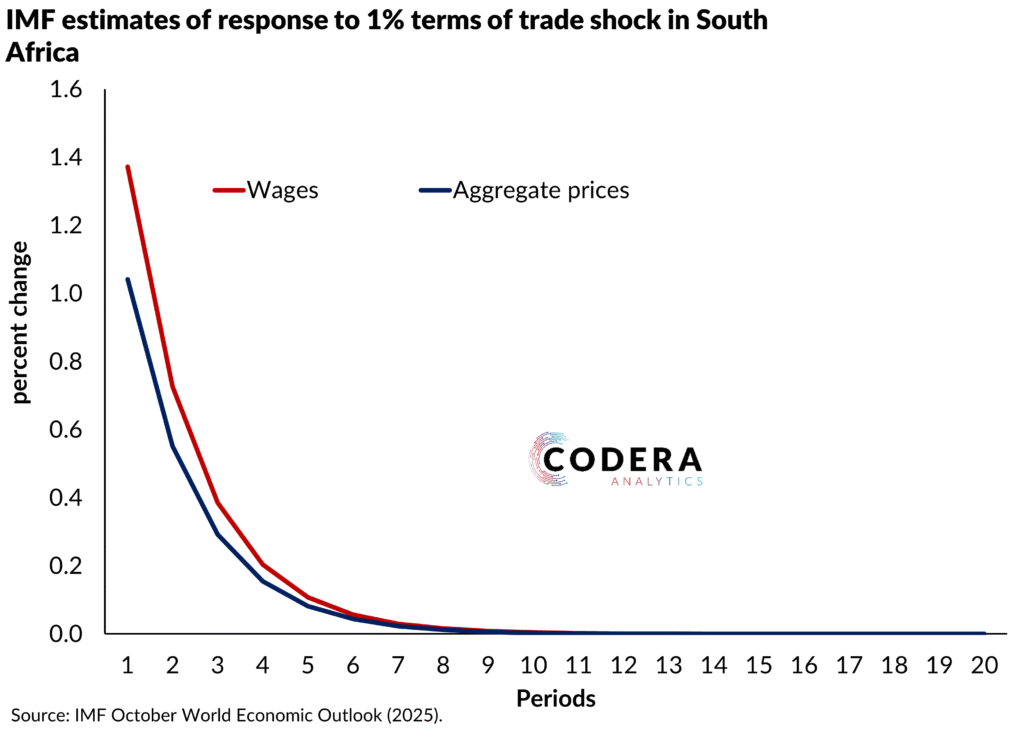

Another reason South Africa has benefitted less from higher commodity prices is high domestic inflation. IMF estimates imply that South African prices and wages rise faster than commodity prices, reducing the economy’s competitiveness. The IMF argue that this leads to a decline in the inflation-adjusted value of receipts from net exports. As a result, negative wealth effects have tended to overwhelm the income effects from higher commodity prices. Unlike most of the net exporters of commodities the IMF consider in their study, the correlation between South African consumption and commodities terms of trade is negative for this reason.

A third potential reason why South Africa has not benefitted as much from the commodity boom as other net commodity exporters is that conventional terms of trade measures overstate the actual gains from higher prices. As the figure above based on the Reserve Bank’s terms of trade indices shows, gold has played an important role in the long term increase in South Africa’s terms of trade, with terms of trade down compared to the 1960s if gold is excluded from the calculation. Gold export volumes have also declined significantly over the last two decades.

Alternative measures suggest that South Africa’s term of trade boom might have been much more modest than standard measures of terms of trade suggest. The IMF’s commodity terms of trade measure suggests that South Africa’s terms of trade are back to 2000 levels and never jumped nearly as much as for Australia or Canada.

If one instead measures terms of trade based on the level of export and import prices (with prices expressed based on actual price levels instead of indices) South Africa’s terms of trade are up around 15% since 2000, compared to over 50% based on the Reserve Bank’s measure.

In other commodity exporting economies such as Australia, export volumes have risen to meet higher global commodity demand. Despite the highest commodity prices in more than two generations, South Africa’s export volumes did not increase to take advantage of this income windfall.

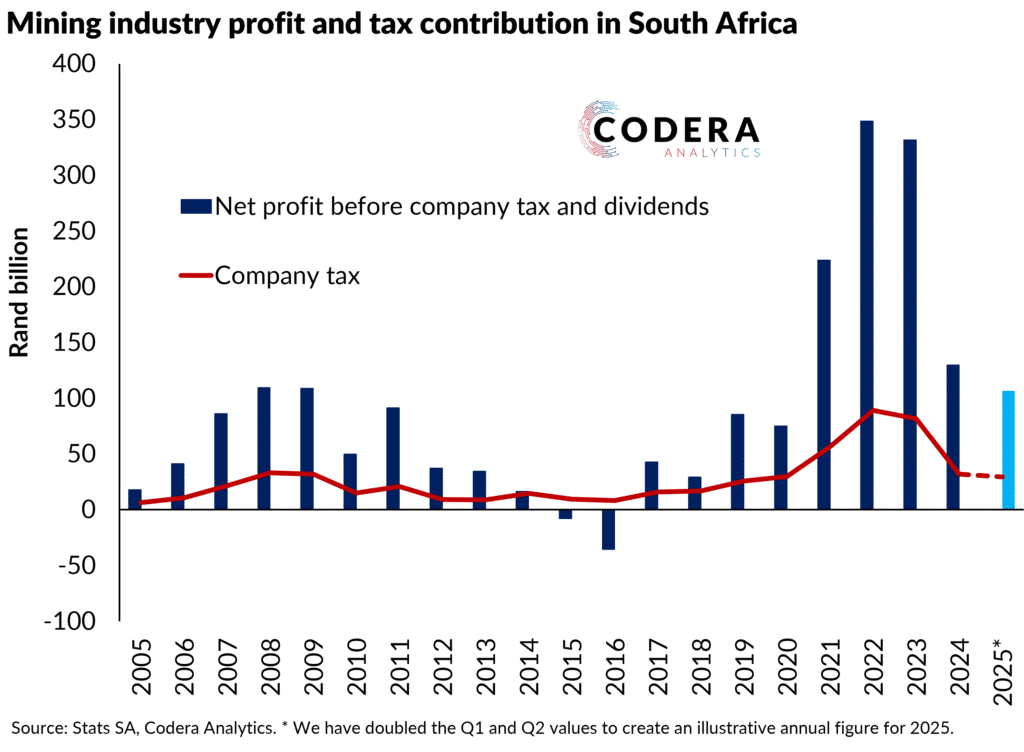

Higher commodity prices did contribute to tax revenues, but the pre-pandemic benefits from the boom were limited as the mining industry was struggling. Much has been made of tax over-collection over recent months because of high commodity prices, but company tax revenues from mining are down two-thirds compared to its 2022 peak.

The major reason for this is that the government has reduced the extent to which the economy can take advantage of higher commodity prices. As a result, South Africa has contracted government-induced ‘Dutch Disease’. The term is typically used to describe the Dutch experience following the discovery of oil and gas in the North Sea in the 1960s, when higher terms of trade from higher commodity prices pushed up wages across the economy. Whereas Dutch Disease is typically associated with productivity improvements in the commodity sector that create inflation in other sectors, the government has given the South African economy Dutch Disease through policy choices that raise the price level and slow productivity growth.

As we showed in earlier research, government-related prices and wages have grown at well above the upper bound of the inflation target. Increasingly interventionist policies also discourage investment, while poor service delivery and policy uncertainty not only raise the cost of doing business, but prevent the mining and manufacturing sectors from expanding production. When policy tries to manage every aspect of business, the economy loses its capacity to adapt and grow.

South Africa’s reform programme is focused on treating the symptoms of our illness, not its underlying causes. Government must stop micromanaging business and allow markets to reward innovation and efficiency. Healing the state involves restoring a capable, merit-based public administration to strengthen the institutions that allows open markets to work.

Dr Steenkamp is CEO at Codera Analytics and a research associate with the Economics Department at Stellenbosch University.