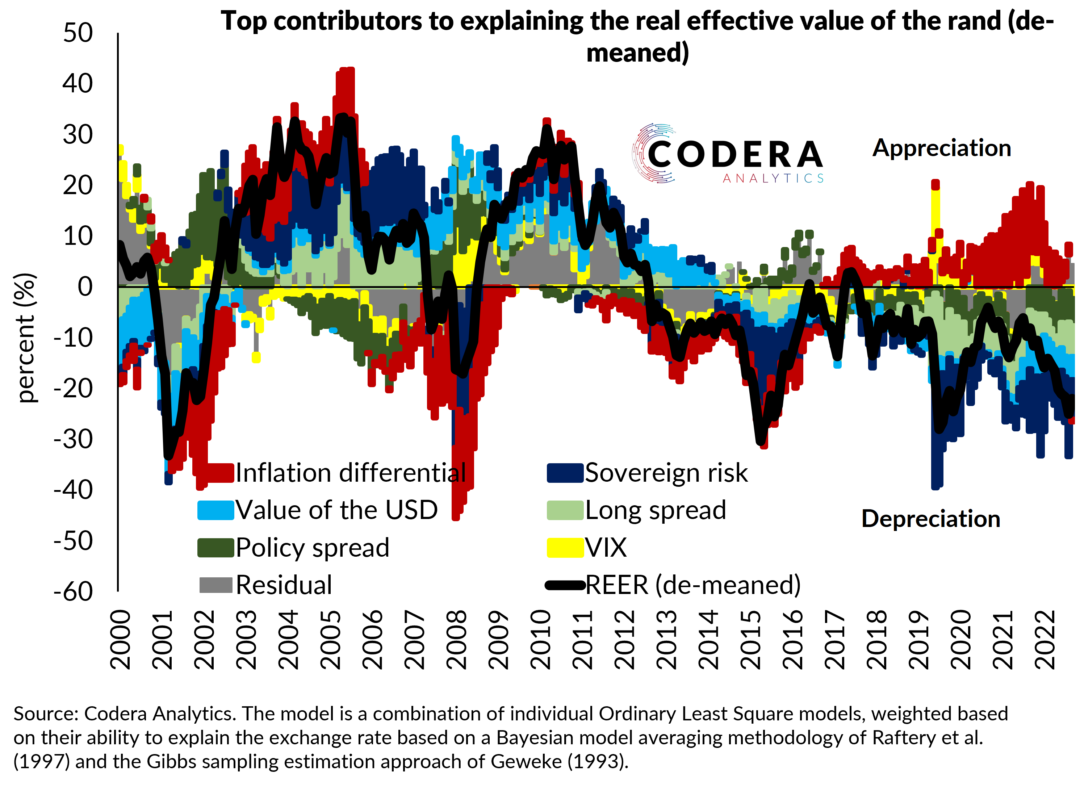

One sometimes hears South African economists argue that the SARB’s MPC relies on high relative interest rates to keep the rand strong and inflation down. Using the US as an example, the correlation between the policy spread and the value of the rand has often run the other way, with the exchange rate depreciating during periods when rates have risen more in SA than in the US. In a previous post, I showed that a simple model of the real effective value of the ZAR also shows that the policy spread does not help to keep the rand strong, once you control for other macroeconomic factors.

One explanation could be that the high relative volatility of the rand makes carry trade strategies less attractive than for the currencies of other high relative interest rate economies (here and here and here). In future posts, I will look at the relationship between rate differentials, the exchange rate and capital flows.