In today’s post, I estimate the option-implied distribution around future values of the USDZAR. As depicted in the fan chart, the options market expects the rand to remain weak against the dollar over the next 12 months. The probability distributions for the exchange rate suggests that uncertainty about the outlook for the USDZAR (measured as the standard deviation of the options-implied distribution) remains elevated compared to history (second chart). The skewness of the USDZAR probability distribution measures the implied risk that the ZAR could move in a particular direction and its kurtosis captures the implied risk of very large ZAR changes. Although options prices have generally been skewed towards depreciation, the market is pricing in slightly lower risk of ZAR depreciation than it has over recent years. Options prices also imply that the market is expecting a lower risk of very large exchange rate changes compared to the last 15 years, particularly at a 6 to 12 month horizon.

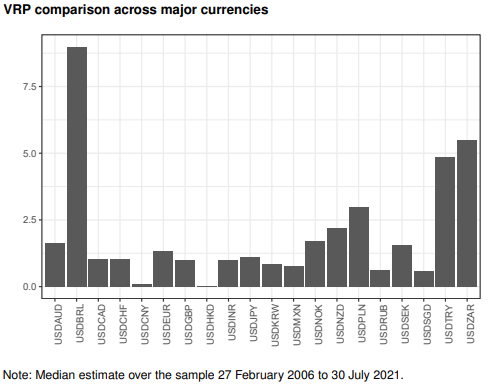

For more details on the approach used read our paper, where we show that option-implied rand variance can improve forecast accuracy when predicting the USDZAR.