A rule of thumb when thinking about the long-term fundamental fair value of a currency is that you will get as many different estimates as the number of models you use. But that does not mean that models are not useful. Different models are useful for different purposes and help to shed led light on how drivers of currency movements might be changing over time. In today’s post, we focus on the simplest fair value model that is commonly used: those based on purchasing power parity (PPP).

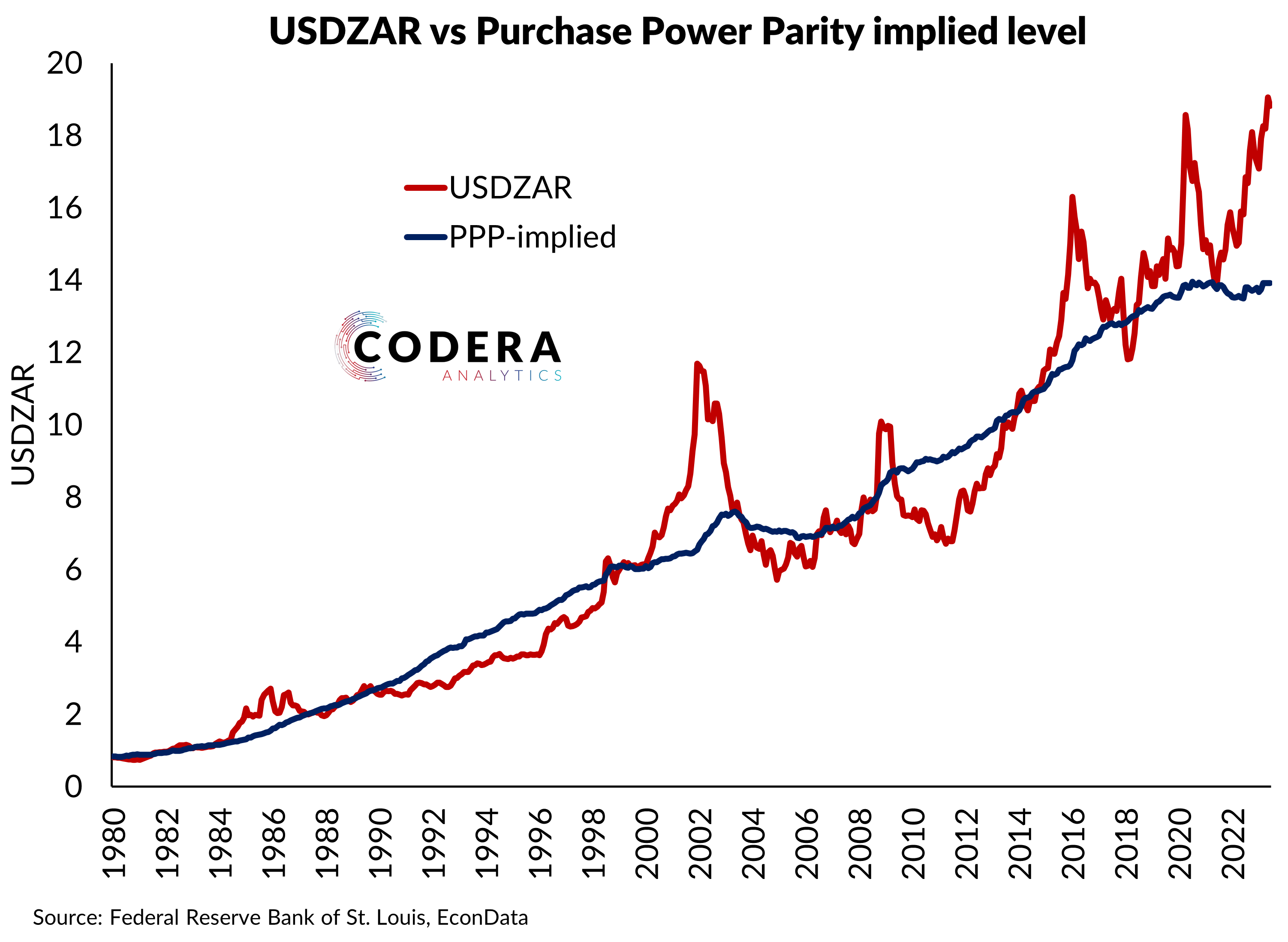

The idea underlying such models is that relative prices should bear on the long term value of a country’s exchange rate. Let us look at the simplest possible case for a single bilateral exchange rate. The chart below plots the PPP-implied level of the USDZAR over the last several decades. A PPP model based only on inflation changes compared to the United States suggests that the ZAR is around 25% undervalued against the USD at present. The chart reveals the tendency for the exchange rate to appreciate/depreciate after bouts of sharp depreciation/appreciation.

As is clear from the simple PPP model presented above, such models tend to struggle to detect mean reversion in exchange rates. As a result, in practice, fair value models generally incorporate other explanatory factors that can explain deviations from PPP.

The second chart provides recent fair value estimates based on a PPP model. This model suggests that the USDZAR is undervalued by around 12% at present.

This is broadly in line with the SARB’s recent assessment. The SARB provides projections of the real effective exchange rate and their latest forecasts (from May 2023) imply that the rand is undervalued by around 13% on a trade-weighted basis. Their projections also assume that this undervaluation is not expected to be eliminated this year.

Since South Africa’s inflation target is higher than that of the US, models that incorporate a PPP consideration in fair value assessment typically build in steady depreciation of the rand over the long term. As can be seen from the chart, simple models like these suggest that the exchange rate can take years to correct misalignments from what inflation and interest differentials would imply.