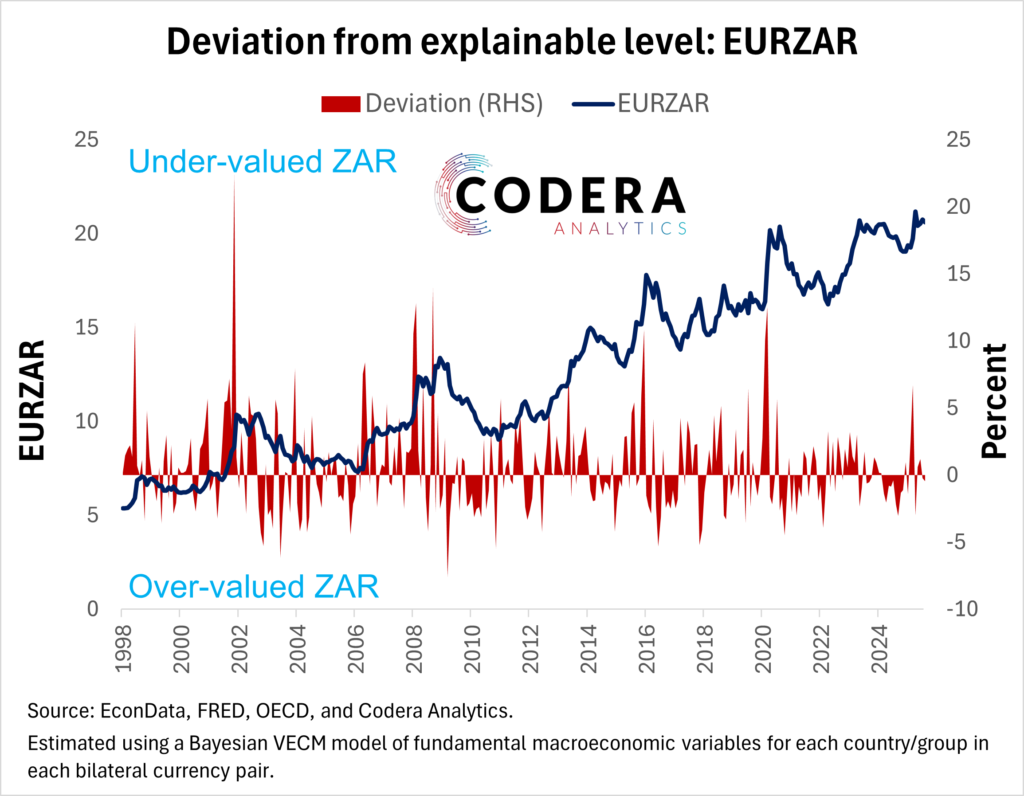

In today’s Codera Analytics post by Oliver Guest we show that fair value estimates of the EURZAR is close to fair value based on a Bayesian regime-switching Vector Error Correction model that incorporates interest rates, consumer prices, money supply and industrial production data, and allows for the drivers of exchange rate movements to change over time.

Codera provides FX forecasts for ZAR crosses and major DM and EM currencies (including Africa). Unlike most forecast providers, our forecasts are updated daily (and our fair value models on a monthly basis), and we produce regular reports demonstrating the performance of our model suite and forecasts. Contact us for a demo.