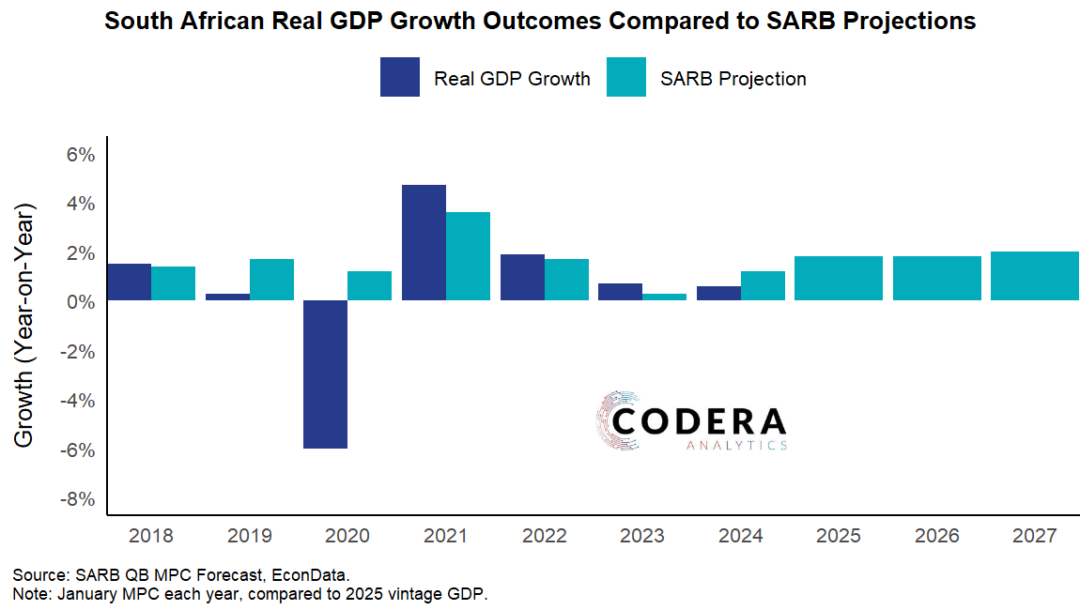

Best practice among central banks is to either publish forecasts consistent with their policy stance or to publish independent ‘staff projections’. The South African Reserve Bank (SARB) stands out for publishing projections that not necessarily in line with Monetary Policy Committee decisions. This means that forecasts are conditioned on a different policy path than has been implemented and increases the risk that their other projections will be inaccurate. The bigger danger with doing so is that it undermines the role of central bank projections as guide for the stance of monetary policy, which could lead to asset mispricing and unnecessary market volatility.

Today’s chart shows that the divergence between policy actions and projections were particularly large during late 2022 and 2023. The COVID-19 pandemic period should be set aside given the unpredictability of the occurrence of the pandemic. However, in the aftermath of the pandemic the SARB continued to interpret the pandemic as predominantly a demand shock, under-estimating the risk of supply-related inflation pressures in its wake.

The most recent SARB projections assume that 60 basis points of cuts in 2024 and 36 basis points of cuts in 2025 would be consistent with keeping inflation at the midpoint of our inflation target over the medium term.

Footnote

Our EconData platform makes it possible for our clients to build dashboards that compare their projections from SARB and National Treasury. Contact us if you are interested in subscribing to our subscriber-only EconData Modules.

Compiled by Johan Hanekom