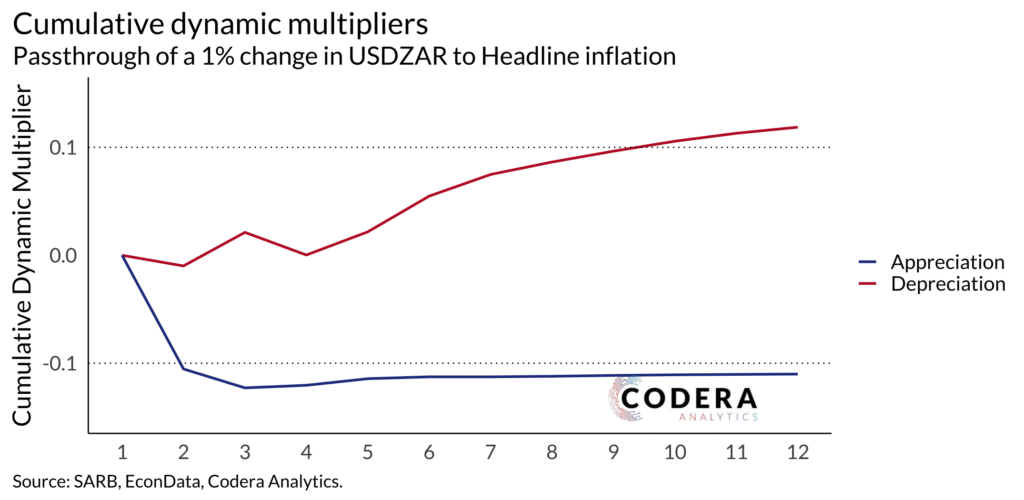

In this Policy Brief with Gabriella Neilon, we estimate exchange rate pass-through in South Africa using a non-linear cointegration approach. We find that it is important to control for pass-through asymmetry and that exchange rate depreciation tend to have a slightly stronger effect on inflation than appreciations for headline inflation. Overall, our pass-through estimates are in the same ballpark as the SARB’s most recent exchange rate pass-through estimates. However, the asymmetries that we document could be considered to refine the calibration of models of monetary policy transmission.