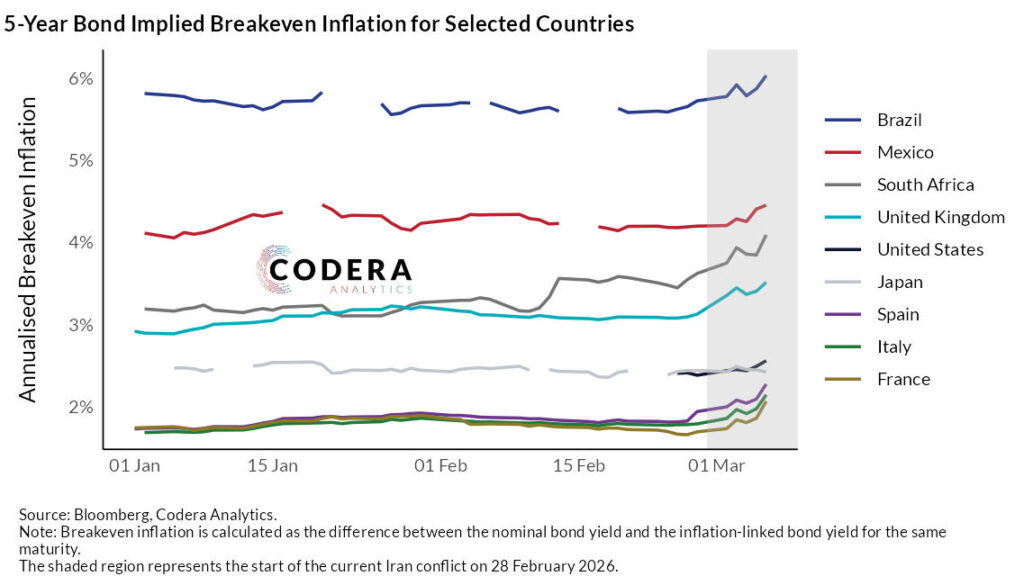

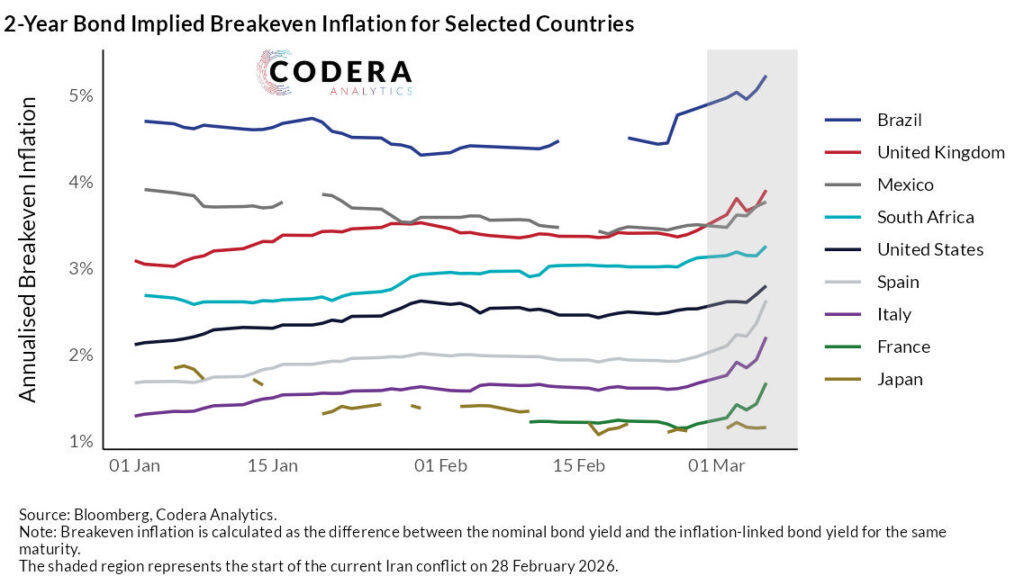

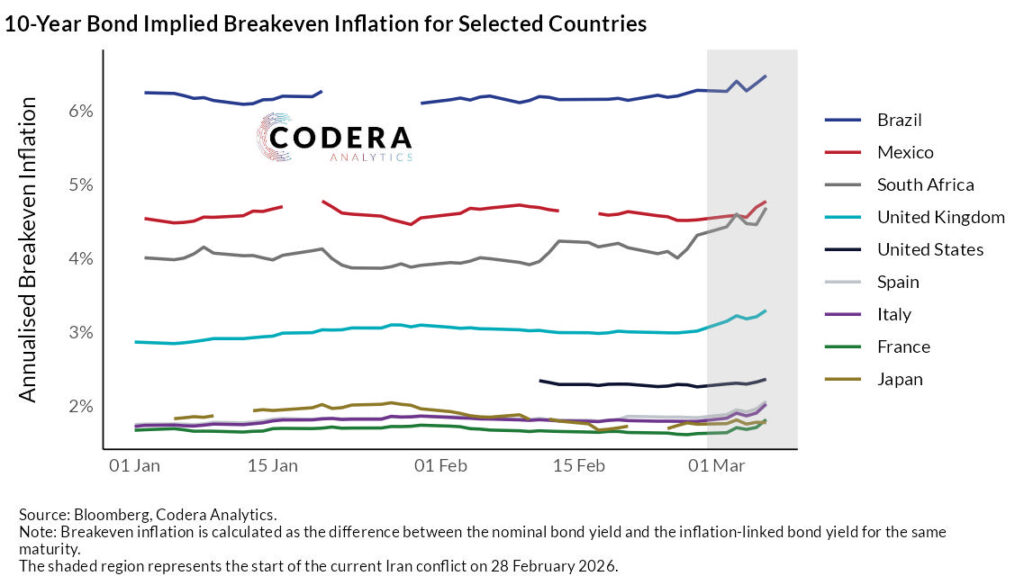

The escalation of the Iran conflict in early March 2026 has caused a sharp repricing of inflation expectations. Today’s post by Aleksandar Mitrovic shows that South African breakeven rates rose much more at the 5-year and 10-year tenors than 2-year tenor, suggesting risk premia have risen substantially and structural inflation expectations have risen more than short term inflation expectations. In major developed markets like the US, 2-year breakeven inflation has spiked by roughly 50 basis points on stagflation fears, while the 10-year maturity remains more anchored, reflecting a market that still views the current energy disruption as a temporary supply shock. Emerging markets have faced the brunt of this volatility as the weakening rand and other EM currencies amplify the impact of Brent crude prices climbing above $100 per barrel. Consequently, the term structure of global breakevens has shifted into a steep inversion, signaling that while near-term inflation is unavoidable, investors are still betting that central bank tightening will eventually contain long-term pressures. An important caveat that we highlight in our recent UNU-WIDER paper is that South African breakevens need to be adjusted for liquidity effects to be reliable indicators of expectations.