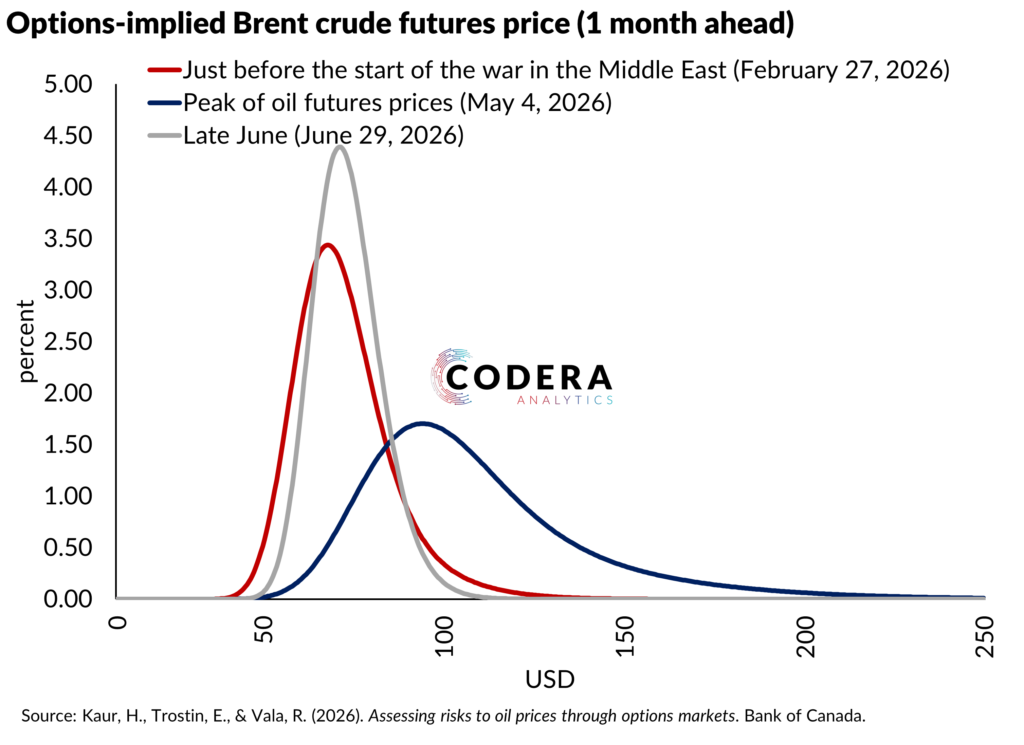

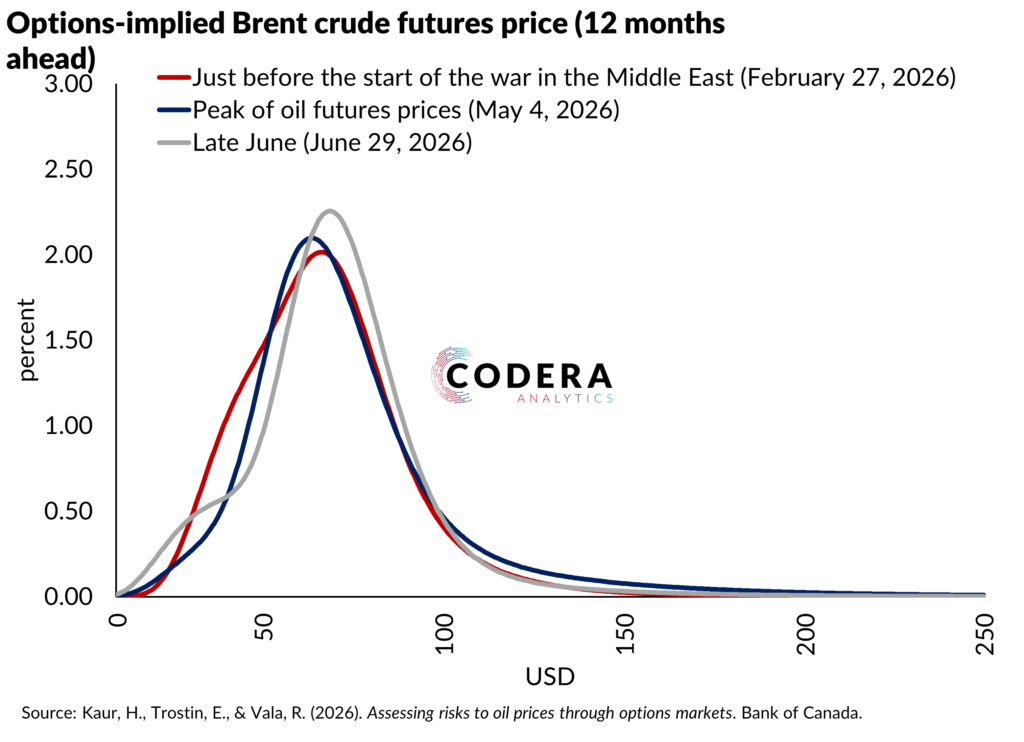

Today’s post compares how market-implied expectations of crude oil prices have changed since the start of the conflict between the US and Iran. Following the closure of the Strait of Hormuz to oil tankers, investor uncertainty drove the average expected 1-month ahead price of Brent oil up from US$73 to US$115 by early May, while the variance in future price predictions more than doubled. This disruption also caused a sharp positive skew as buyers paid premia to hedge against extreme near-term price spikes. However, the market proved resilient, and by late June the price distribution shifted back toward pre-closure norms as extreme supply anxieties largely eased. In contrast, the stable distribution of one-year-ahead oil price futures over this period suggests that investors anticipated a resolution to the war and a return to normal market conditions within 12 months.