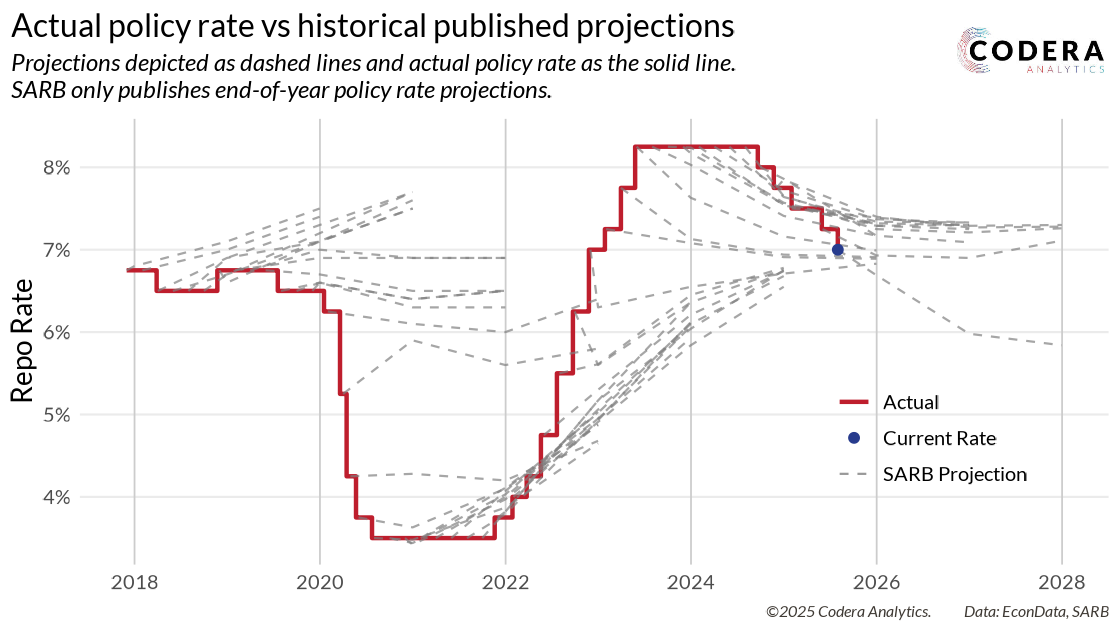

Today’s chart of the day shows that there have been times when SARB policy decisions have diverged from their published policy rate forecasts that accompany a decision. The divergence between policy actions and projections were particularly large during late 2022 and 2023. The COVID-19 pandemic period should be set aside given the unpredictability of the occurrence of the pandemic. However, in the aftermath of the pandemic, the SARB continued to interpret the pandemic as predominantly a demand shock, under-estimating the risk of supply-related inflation pressures in its wake. This meant that the post-pandemic spike in inflation caught SARB by surprise, as they have been slow to revise their judgements about the underlying trends in the economy, for a long time holding on to a view that inflation pressures would be transitory despite growing evidence to the contrary.

The SARB’s July 2025 projections imply that it can cut interest rates by another 100 basis points by the end of next year, a major change in the projections relative to earlier forecasts. Our view is still that inflation will pick up over the next 6 months and that it will be difficult for the SARB to achieve a 3% target without a lot of luck (e.g. ZAR strengthening) or the government’s help.

Compiled by Aidan Horn