The South African Reserve Bank (SARB) published its latest Monetary Policy Review (MPR) yesterday. As usual, it provides a bunch of interesting analysis about the current business cycle.

It was nice to see SARB provide alternative measures of underlying inflation (‘supercore’ and ‘PCCI’), as we have calling for since 2022. These measures are meant to capture demand-driven inflation. As previously argued in this blog, judging whether these new measure are useful from a monetary policy perspective requires showing whether they are useful for forecasting and whether they help economists understand what economic factors are driving inflation pressures. We will have to wait for the underlying analytical notes to be released to judge whether they are useful as indicators of underlying inflation pressures.

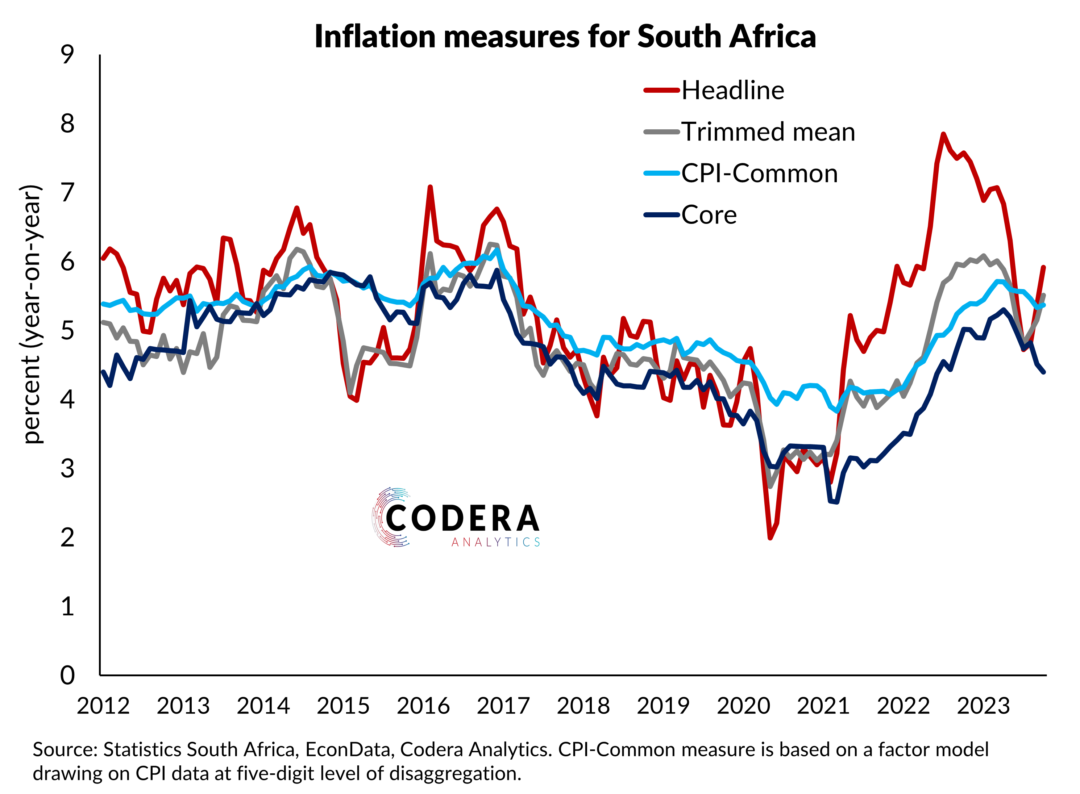

The key analytical question with regards to inflation at the moment is what is keeping inflation above the mid-point target and when these pressures will begin to dissipate. The MPR shows that food price and core goods forecast errors where the main sources of two-year ahead inflation forecast errors in 2022/23. But SARB’s policy model allows one to assess how economic shocks (demand, supply, monetary policy stance etc.) contribute to deviations in inflation from the target. So it is odd not to use the model to interpret what aspects of its economic narrative it got wrong over the last several policy decisions. As a result, economists can only judge the credibility of SARB’s inflation forecasts by looking at SARB’s consumer price component projections. Ideally, one would want to considering the appropriateness of the stance of policy by assessing the overall economic narrative underlying all of its projections. As argued previously, SARB’s assessment of the role of supply shocks was an important contributor to its under-prediction of inflation in 2022/23, and the best way to prevent future policy missteps is by having a systematic approach to learning about the sources of its forecast errors. By not using its model to communicate the narrative underlying its projections and policy stance it also reduces the information value of its forecasts.

It is also worth mentioning that the MPR features interesting content on the inflation target. Figure 5.1 shows that core inflation contributed 3.6 percentage points (about 2/3rds) to the level of inflation in 2024Q1. Getting inflation structurally lower will therefore require permanently lowering not just the government-related inflation components that have been holding up headline inflation, but other private sector inflation components.

The advantage of performing economic-driver assessment of underlying inflation (over SARB’s preferred approach of analysing individual consumer price components) is that it enables assessment of what the drivers of trend inflation have been and helps to inform the debate around the appropriate inflation target level. We showed in an earlier post how one can estimate trend inflation and use such measures for understanding the drivers of underlying inflation or debating what an appropriate inflation target might be.

The most important unanswered questions in the inflation target discussion in South Africa are what level of inflation might be achievable without dramatically higher interest rates and when to begin transitioning to a lower target to ensure as low a cost to the economy as possible. One might argue, for example, that SARB missed an ideal opportunity in the lead-up to the COVID-19 pandemic to lower the target given that favourable supply shocks were responsible for containing inflation at the time. Irrespective, a first step towards a lower target would be addressing high administered price inflation in South Africa, something only government can deal with.