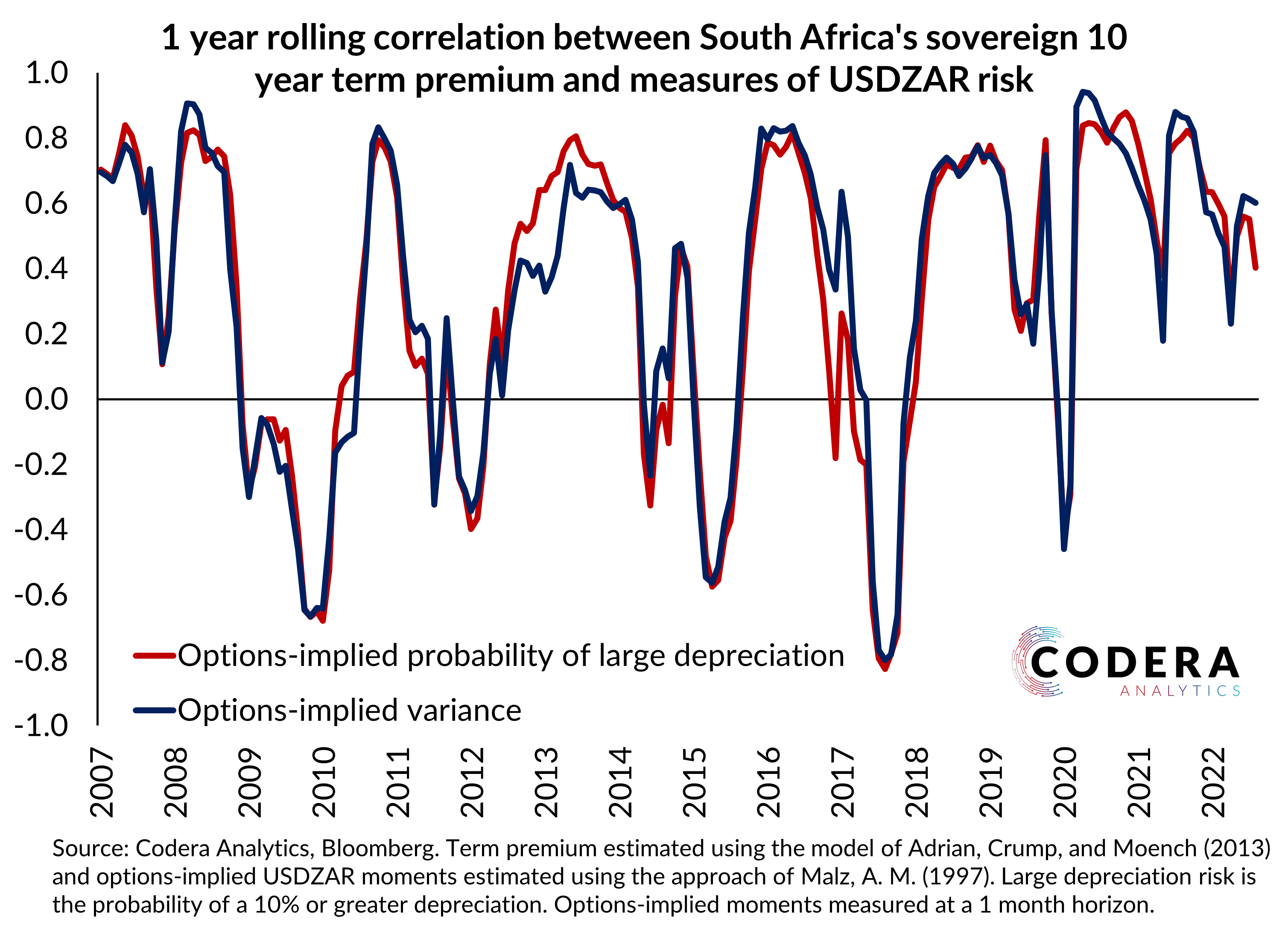

One possible explanation for South Africa’s steep sovereign yield curve is that meaningful exchange rate depreciation risk is embedded in our long term interest rates. Our USDZAR options-implied variance estimate, which captures exchange rate uncertainty priced into FX options prices, and our estimate of options market-implied probability of a 10% or greater depreciation in the USDZAR over the next month have both had a strong positive correlation with the South African sovereign term premium over the last several years. This suggests that high South African long term rates could partly reflect investors concerns about the possibility that the rand could depreciate strongly, which would be expected to push up inflation. Interestingly, the relationship becomes negative after large exchange rate depreciations. This could reflect expectations that exchange rate overshooting would be partly reversed, especially when a specific bout of depreciation was driven by global risk shocks.