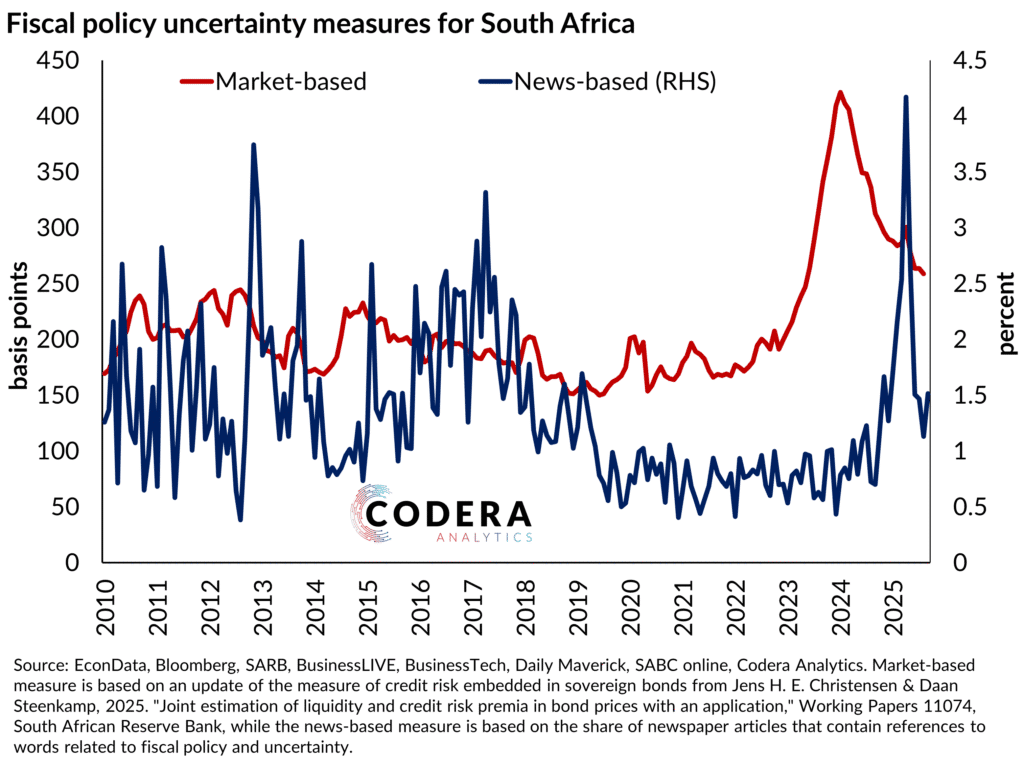

Today’s post with Jacques Quass De Vos compares two other market- and news-based fiscal policy uncertainty measures for South Africa from Codera. Fiscal policy uncertainty has been getting more news coverage over the last year but market-based measures of fiscal risk (a specific type of fiscal uncertainty) spiked a lot earlier. As we have shown, the recent spike in the South African fiscal credit risk premium seems tied to the increase in the South African government debt-to-GDP ratio. This higher perceived level of credit risk also seems to have influenced investors’ perceptions about the future liquidity in the South African government bond market, causing them to demand notably higher liquidity risk premia.