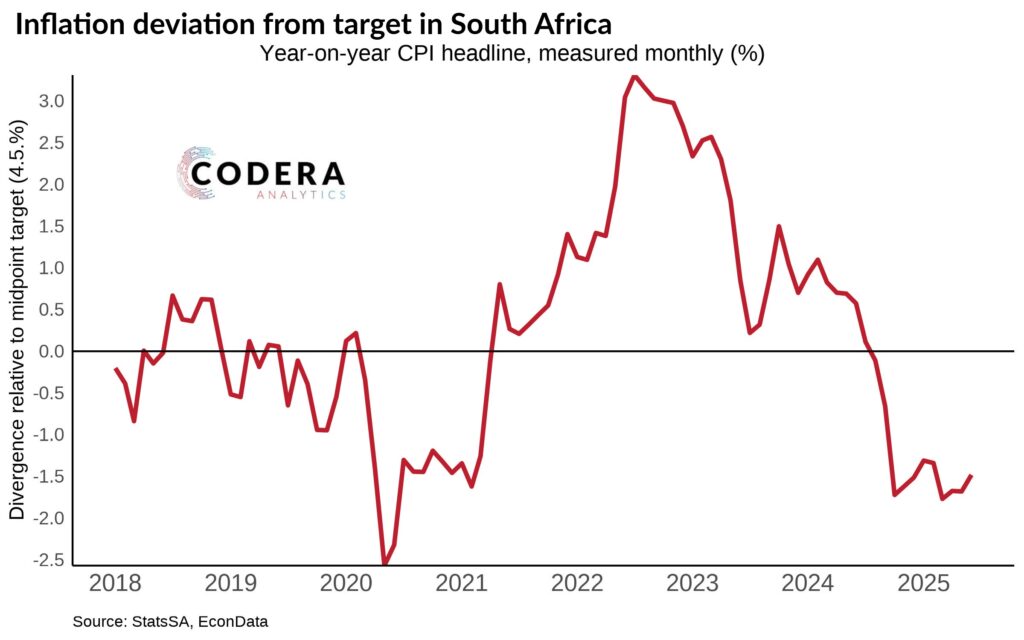

Today’s post by Sinead Morrow shows that South Africa’s headline inflation strongly deviated from the SARB’s preferred 4.5% midpoint between mid-2021 and mid-2024. Repeated divergences from the target underscores the limitations of a broad 3‑6% inflation band and reinforces the case for a lower target and improved policy communication to anchor expectations more tightly at a lower level. For more on our take on the optimal inflation target for South Africa and the implications for the appropriate conduct of monetary policy please see our paper on the inflation targeting debate.