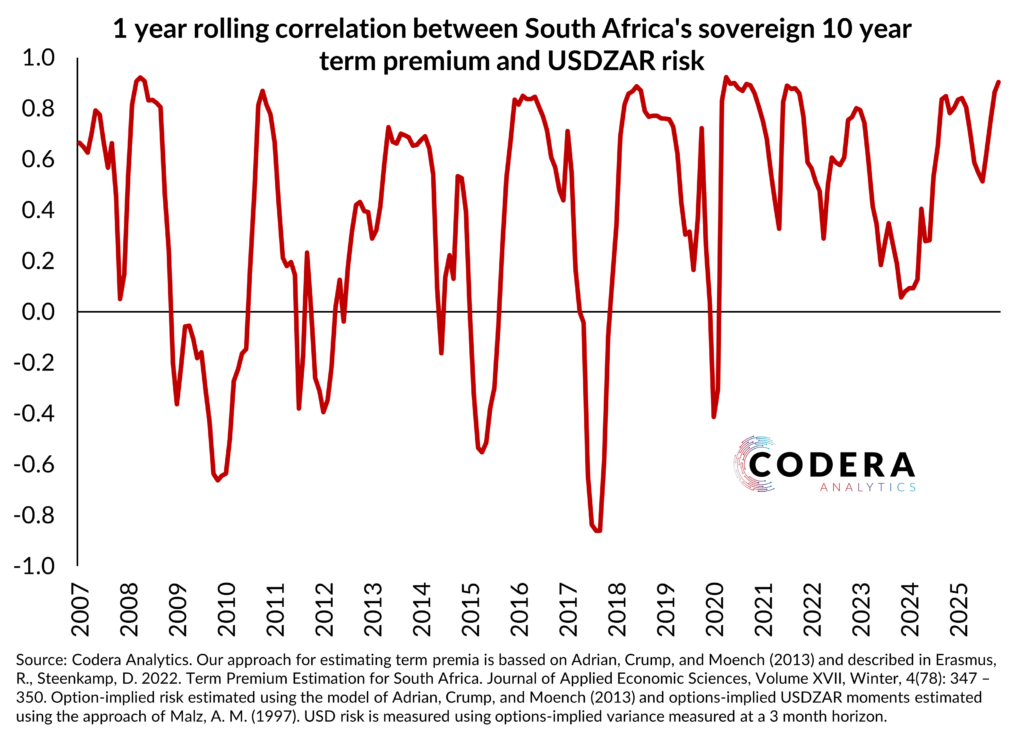

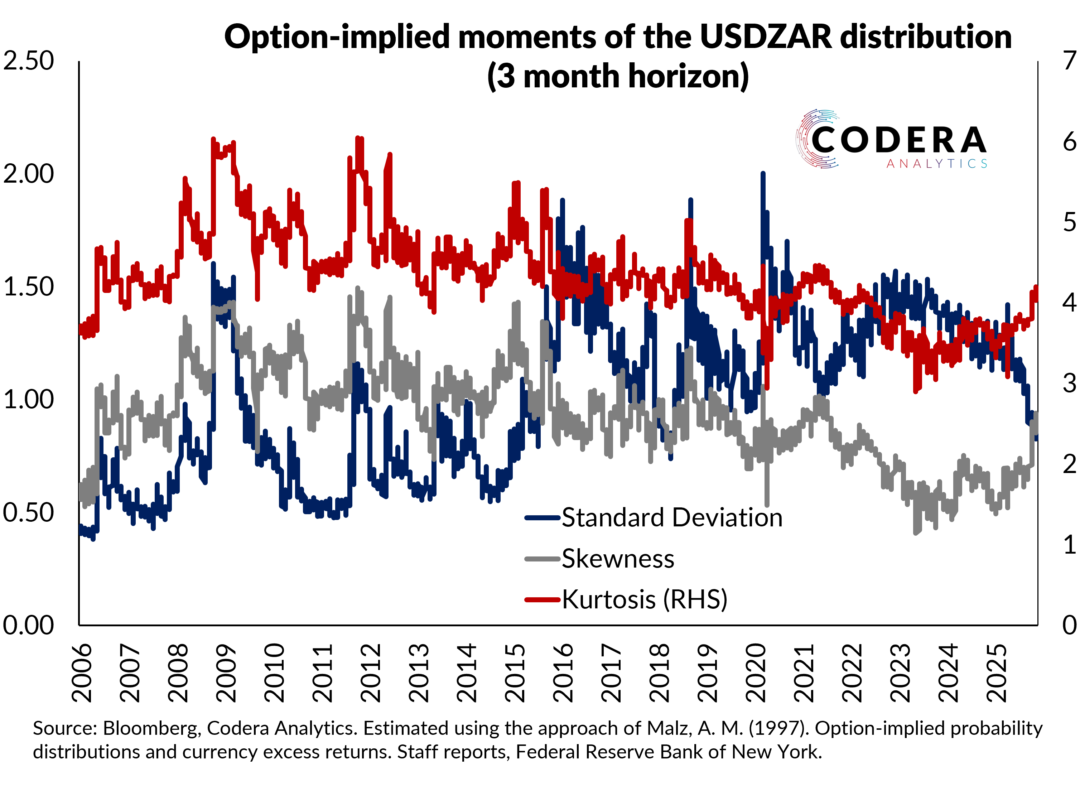

One possible explanation for South Africa’s steep sovereign yield curve is that elevated exchange rate depreciation risk has been embedded in our long term interest rates. Today’s post updates analysis from our paper on SA’s yield curve conundrum. Options-implied variance, which captures exchange rate uncertainty priced into FX options prices, has historically had a strong, but time-varying relationship with the South African term premium. This suggests that high historical South African sovereign long term rates could partly reflect investors concerns about the possibility that the rand could depreciate strongly, which would be expected to push up inflation. Since the beginning of the year, the correlation has strengthened, as uncertainty about the outlook for the USDZAR has fallen as the the term premium has fallen.