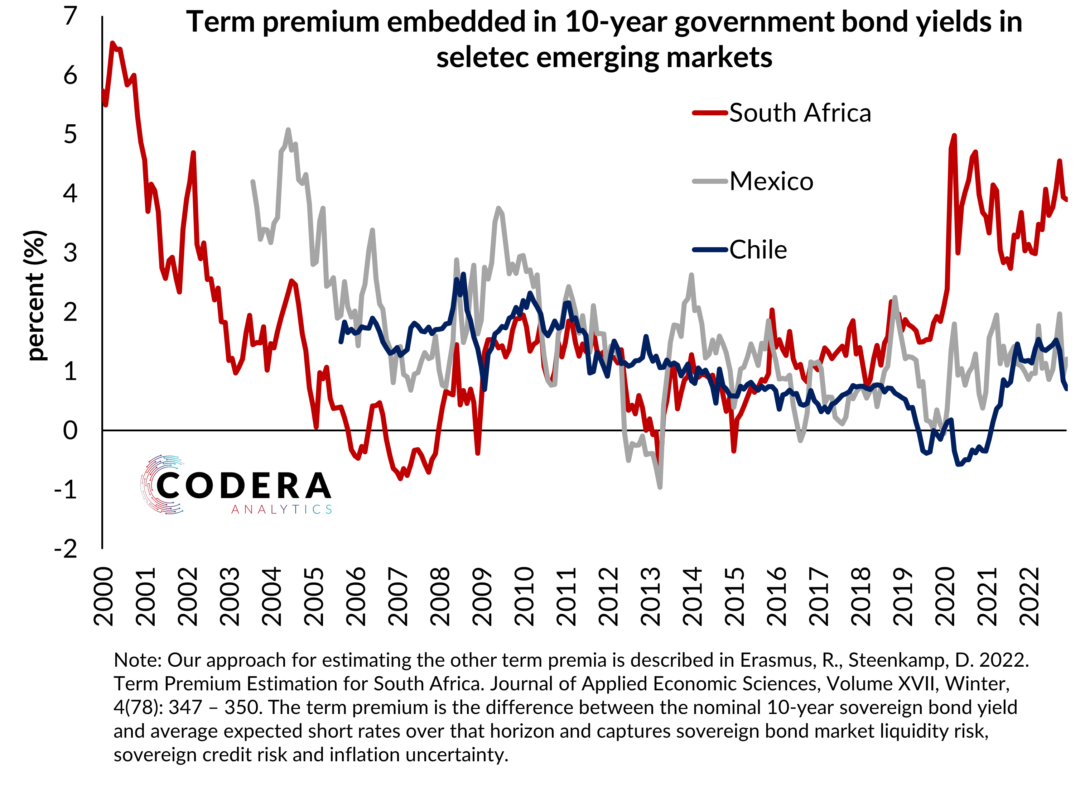

Today’s post provides an update of Codera’s term premium estimates for the South African sovereign bond curve. Focusing on the 10 year point, our estimates show that that the decline in long yields has reflected a fall in the term premium and not a reduction in average expected short rates. The implication is that market-implied neutral rate has not declined meaningfully since formal adoption of a lower inflation target.