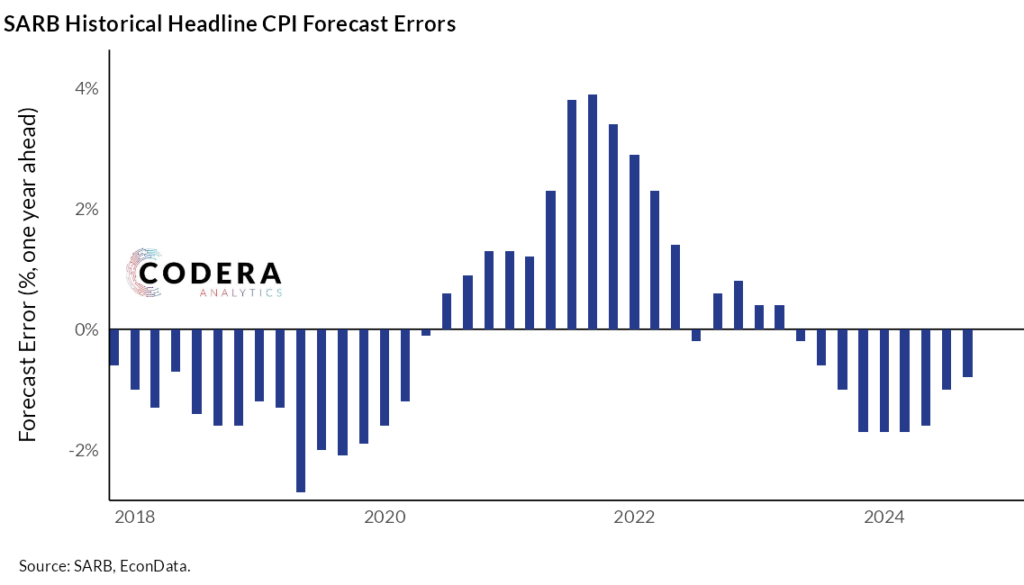

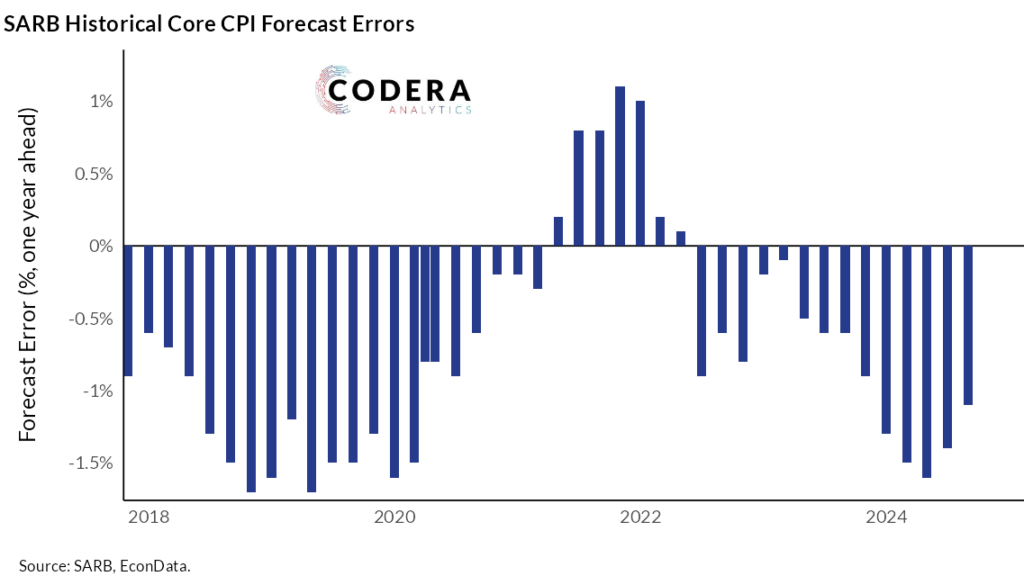

Serial correlation in a central bank’s inflation forecasts indicates that forecast errors are systematically related over time, rather than being random. This suggests persistent bias or slow information updating, meaning shocks to inflation are not being fully incorporated into forecasts when they occur. Today’s post by Aleksandar Mitrovic shows that the SARB’s projections show meaningful serial correlation over time.