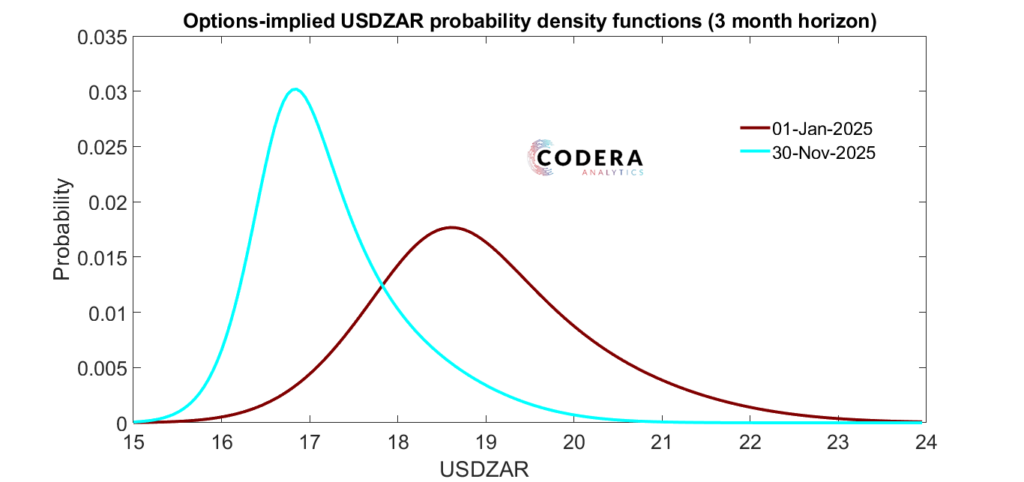

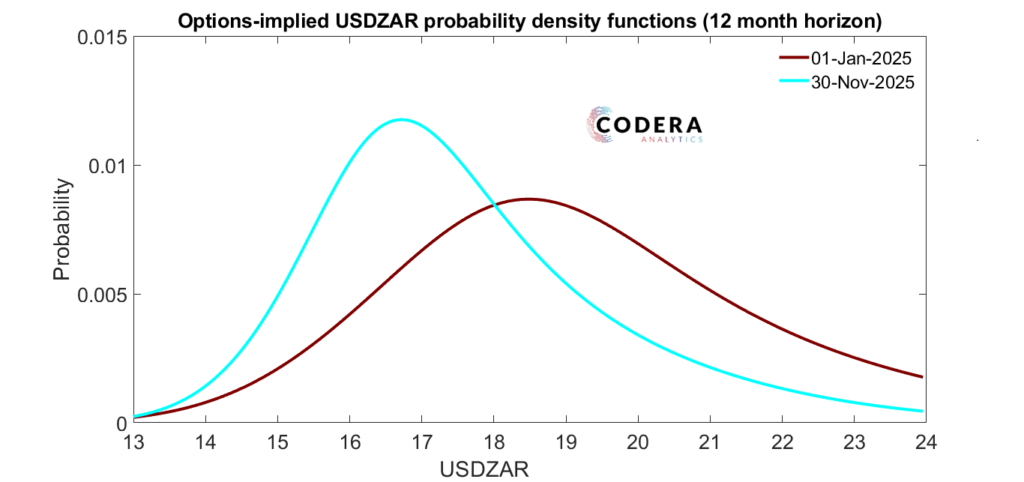

In today’s post, we back out market expectations of future USDZAR movements using options prices. The distribution of the USDZAR’s options-implied density has become more peaked, with more of the distribution’s probability mass at lower exchange rate levels as uncertainty around the mean expected value of USDZAR has decreased, particularly over a shorter horizon. As is typical for the rand, the market continues to price in a larger probability that the currency could depreciate than appreciate, visible as a rightward skew in the distribution. These figures show that the market is pricing lower ZAR uncertainty overall and lower risk that the rand could appreciate than at the beginning of the year (here and here).

Footnote

For more details on the approach used read our paper, where we show that option-implied rand variance can improve forecast accuracy when predicting the USDZAR. This paper by Michelle Lewis also provides more discussion on using option pricing to gauge market expectations.