In today’s blog post, I repost last week’s Business Day article.

SA has not felt tight grip of austerity, yet

Some commentators claim that there has been fiscal austerity in South Africa over recent years. This is not the case.

The most common definition of austerity is higher taxes or spending cuts implemented to eliminate budget deficits and consolidate debt. South Africa has not experienced nominal cuts to national spending or large tax increases over recent years. To give a sense of what austerity looks like, consolidation measures implemented in Ireland following the Global Financial Crisis (GFC) required tax increases and spending cuts amounting to 20% of GDP.

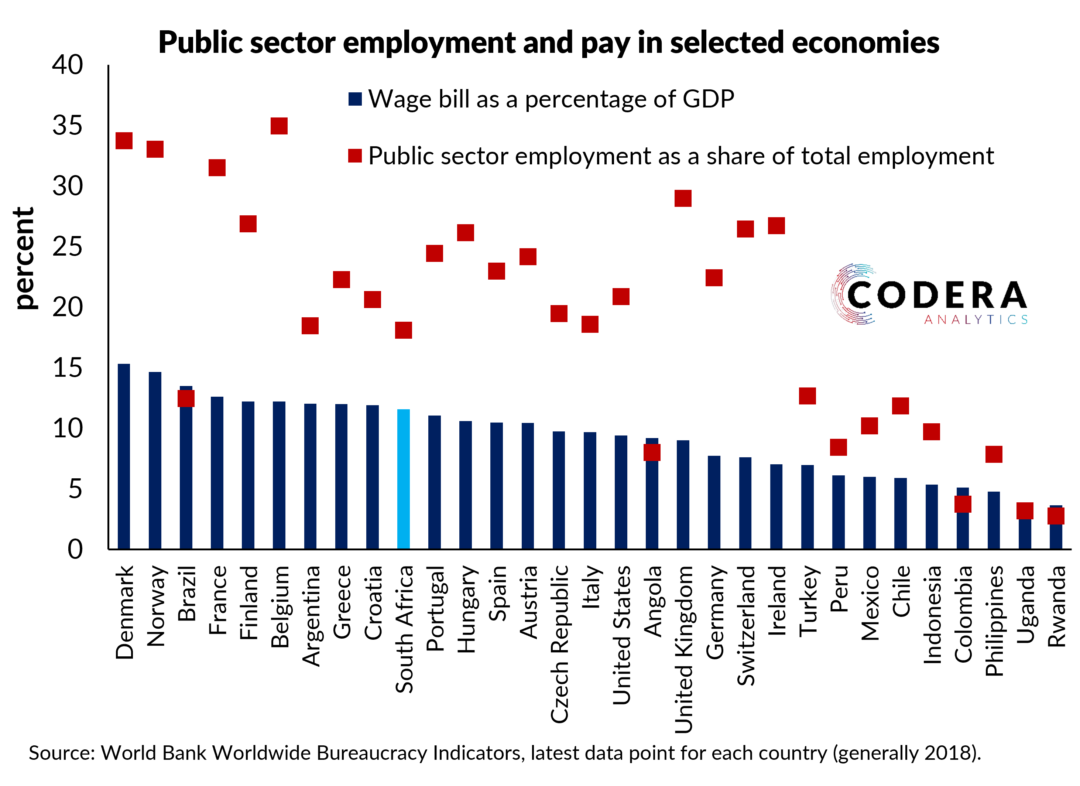

Instead, South Africa’s post-GFC fiscal framework has been characterised by a reorientation towards transfers, public employee wages and bailouts for state owned enterprises and away from public investment and provincial expenditure. Since economic growth has stalled and borrowing costs have been high, non-interest expenditure components have been squeezed, but this has not been enough to reduce budget deficits and stabilise debt. If one excludes state owned enterprise (SOE) bailouts, the growth in inflation-adjusted value of non-interest spending has declined sharply since the COVID-19 pandemic.

While South Africa has not implemented fiscal austerity, the amount of new resources flowing to government departments, provinces and municipalities has fallen off a lot. This is why South Africa is experiencing a service delivery crisis. Government spends over 60% of its budget on compensation of employees, servicing debt and grants. Growth in these categories have been crowding out infrastructure investment and maintenance and other socio-economic expenditures. It is no wonder South African roads are increasingly potholed and water shortages are becoming an everyday challenge when provinces are spending less than 2% of the value of their assets on maintenance and repair.

To assess the stance of fiscal policy over time, I estimate South Africa’s ‘fiscal space’, which refers to the extent to which there remains fiscal resources for fiscal policy to respond to unexpected shocks. A useful indicator is the cyclical fiscal stance, that is, the main budget fiscal balance adjusted for the impact of the business cycle on revenue and expenditure. The measure suggests that the fiscal stance became less prudent (i.e. more negative) after the GFC of 2008/9. Whereas fiscal policy was broadly counter-cyclical ahead of the GFC, post-GFC fiscal policy eased and remained somewhat easy even as excess capacity (what economists call the ‘output gap’) has narrowed to close to zero.

The IMF measure of the cyclical stance of fiscal policy for South Africa has remained in negative territory since 2009, implying that fiscal policy has stayed ‘loose’ even as the economy began to recover after the GFC and the output gap gradually closed ahead of the COVID-19 crisis. Looking ahead, the IMF assumes fiscal policy will become less stimulative but a cyclically adjusted primary surplus will only be achieved in 2026/27. However, the IMF predicts that South Africa’s structural budget balance will deteriorate over the next 5 years, reflecting the impact of growing debt service costs from rising public debt.

A related question is whether attempts at fiscal consolidation have weighed on economic growth in South Africa. A measure the impact of the fiscal stance on the business cycle is the ‘fiscal impulse’, which can be proxied as the year-to-year change in the cyclically adjusted budget balance. IMF estimates suggest that fiscal policy has been broadly supportive of aggregate demand since the GFC. These estimates suggest that fiscal policy was only a meaningful brake on activity between 2018 and 2020, and it boosted the economy in the aftermath of the COVID-19 pandemic. Looking ahead, the IMF assumes fiscal policy will become less stimulative, although the main budget cyclical balance is expected to remain negative.

These estimates suggest that fiscal policy has remained loose in spite of lower growth. But has loose fiscal policy stimulated economic activity or have tighter budgets worsened the economy’s slowing growth? Research by du Rand et al (2023) and the South African Reserve Bank suggest that government expenditure and investment has either had no noticeable effect on economic growth or represented a drag on growth. It is likely that higher public debt, the deterioration in investor confidence, corruption and deteriorating state capacity have reduced the impact of spending on the economy and directly weighted on potential growth.

Why did South Africa not have to implement hard austerity following the GFC like countries like Ireland or Argentina? National Treasury had consolidated debt in the lead-up to the GFC. Low debt and accommodating global environment with low interest rates helped South Africa avoid a severe consolidation.

But higher debt and rising interest rates are increasing the chances that fiscal austerity could be forced on South Africa. With limited fiscal space to respond, South Africa is increasingly vulnerable to shocks and changes in global financial conditions. A natural disaster or a global shock like the another pandemic could force cuts in public sector headcount, wage freezes or across the board nominal spending cuts if government cannot continue to borrow at manageable interest rates.

The most painless way to avoid austerity is to raise economic growth. This requires assertive policies to address public sector service delivery problems and reforms to unleash the private sector. The recent Harvard Growth Lab report provides practical measures to remove barriers to growth, stimulate investment and create employment. These include accelerating electricity market reforms to promote private sector production and storage, a shift to merit-based employment in the public sector, and relaxing preferential procurement rules. The longer South Africa delays in addressing the things that are holding the economy back from creating jobs and growing incomes, the more likely a hard fiscal consolidation becomes.