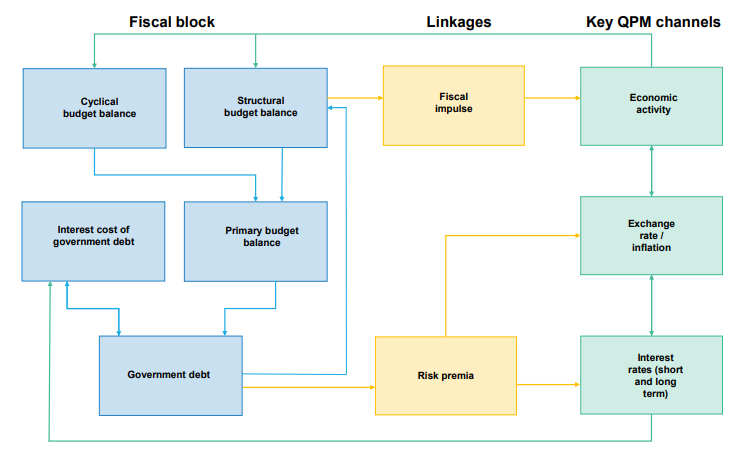

SARB has begun publishing forecasts from its updated QPM model. The new version features a fiscal block to capture how fiscal policy is affecting the economy and, in particular, how rising debt is contributing to higher long-term interest rates in South Africa.

Curiously, there is hardly any fiscal analysis in the Monetary Policy Statement: the word ‘fiscal’ does not appear at all. The only clue to SARB’s assessment of how government spending and revenue might be affecting inflation is that spending by public corporations and general government “remains positive in real terms”, while “sharply lower tax revenue, higher employee compensation and ongoing financing needs of state-owned enterprises are likely to keep the long-term cost of borrowing elevated”. Like the IMF, our assessment is that the fiscal stance has remained stimulatory at the margin, but will become less so over the coming years. One hopes SARB will communicate its assessment of the impulse from the fiscal stance to growth and inflation in future monetary policy communication.

Ahead of yesterday’s meeting, several economists had been speculating about whether the changes to the QPM would lead to a more ‘dovish/hawkish’ stance of policy. That is, whether the model would suggest that less/more aggressive changes in rate setting would be needed to achieve the inflation target. This confusion over how the Monetary Policy Committee (MPC) actually use the model in practice and how judgements affect the projections in the model demonstrates that SARB has more work to do to explain to analysts what the role of QPM in MPC decision-making is.

QPM is fundamentally a framework for summarising SARB’s views about the economy and how policy needs to be adjusted to achieve the inflation target. This is why it is surprising that the MPC’s policy narrative is not communicated through the lens of QPM. One cannot assess whether a specific policy stance is dovish/hawkish without understanding what the SARB’s assessment of the trends in the economy are and what the shocks are that are driving deviations from those trends for specific economic variables like growth or inflation. For example, the extent to which a lower-than-expected growth outcome might require a change in the policy rate depends on what the shocks are that SARB thinks contributed to a downward surprise. SARB’s own assessment is that their policy stance is mildly restrictive now, but that the current policy rate is appropriate given that risks to inflation are skewed to the upside and to ensure that inflation expectations remain anchored (as 2023 expectations are still above the upper limit of the target).

Over recent meetings, MPC decisions have diverged from the policy rate projections that underlie its published forecasts (here and here for more). The published repo rate projection for the end of 2023 is now 8%, up from 7.6% in May, so the QPM projections still imply that policy easing before the end of the year would be consistent with achieving the inflation target.

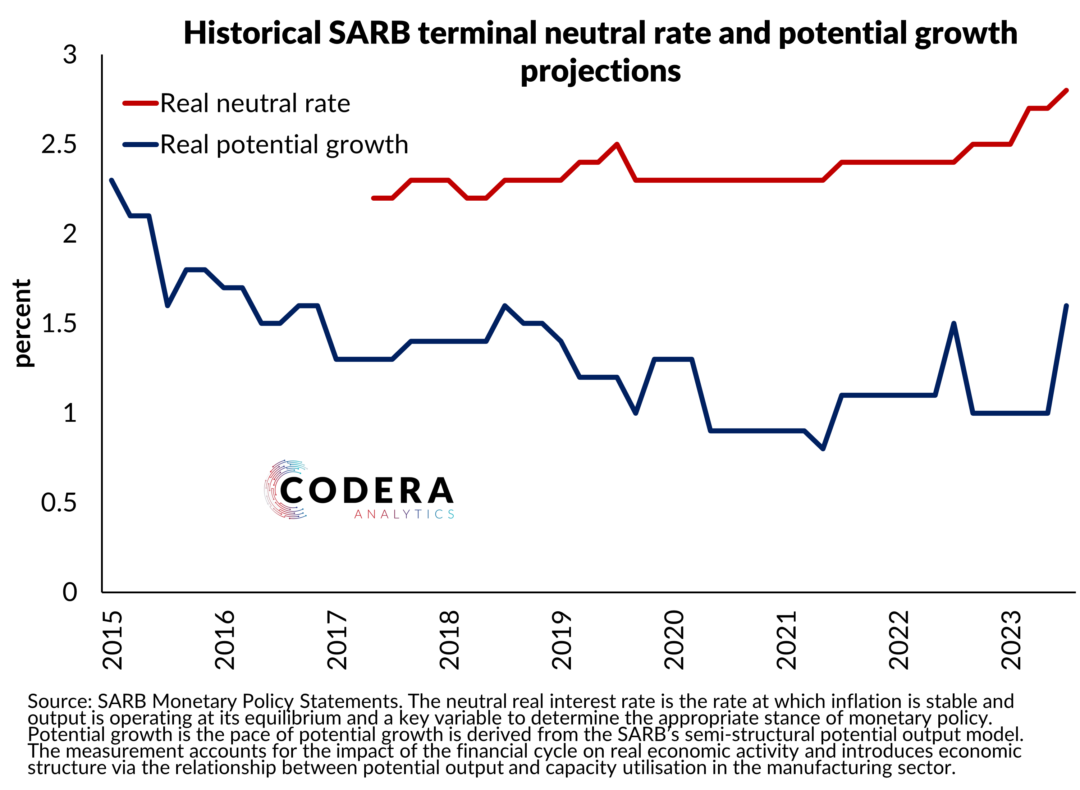

SARB has not raised its estimate of the real neutral interest rate for 2023, although its terminal neutral rate is now at 2.7% (compared to 2.5% at the time of the May 2023 meeting). This still leaves a lot of uncertainty around SARB’s assessment of when the turning point in interest cycle will be now that the new model has been adopted. We have estimated that the market thinks that the neutral rate is 50 basis points higher than SARB’s figure, which suggests some risk that further tightening might be needed.

The SARB have updated the variables that feed into QPM’s ‘Taylor-rule’, which dictates how rates should adjust to meet the inflation target based on expected inflation and the cyclical position of the economy. The updated forecasts have a lower inflation trajectory and a higher required policy path than the May projections. SARB has only very marginally lowered its core inflation forecasts. The projections do not build in much demand-pull inflation, with growth expected to be in line with SARB’s estimate of potential growth (of only -0.1% for 2023).

Unfortunately, without further details on the drivers of forecasts, it is hard to square the changes in key forecasts round to round with changes in the policy advice from QPM. Hopefully SARB will make additional analytical content available in future to describe in more detail the economic narrative underlying its projections.

Unfortunately, without further details on the drivers of forecasts, it is hard to square the changes in key forecasts round to round with changes in the policy advice from QPM. Hopefully SARB will make additional analytical content available in future to describe in more detail the economic narrative underlying its projections.