Our article on banking data was published in the Business Day, below we repost the article.

Could anyone apply the wonders of artificial intelligence (AI) to predict the next bank failure in SA? Unlikely. But it does not have to be like this. Though the Reserve Bank publishes bank-level balance sheet data, a small extension to what it makes available would make far more effective analysis of the banking sector possible. This would, coincidentally, be in line with the Basel III principle of third-party oversight.

To give credit where it is due, SA stands out internationally in the availability of detailed bank-level balance sheet statistics. Since 2008 the Bank has published monthly supervisory banking data at individual bank level. The data is granular, giving a detailed view into balance sheet items such as deposits and loans.

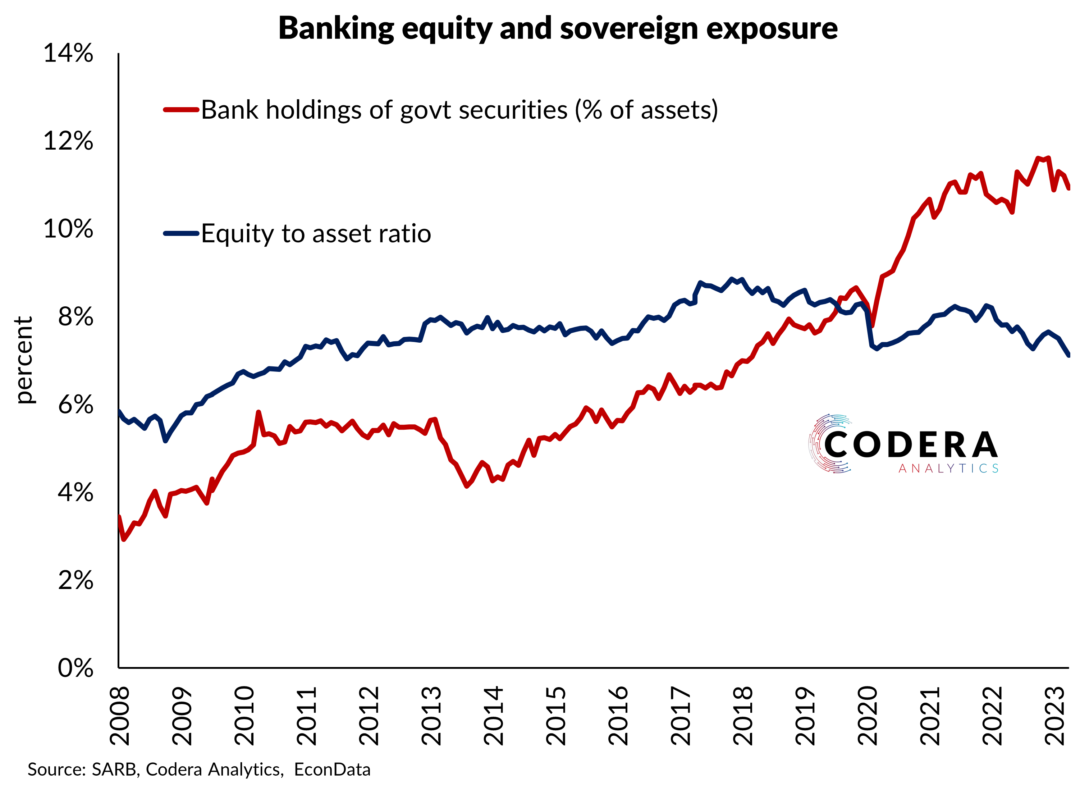

What is more, SA banks are considered to be well regulated, with strong balance sheets. The IMF’s 2023 Article IV report says the financial system is resilient and bank capital buffers are adequate against higher levels of non-performing loans. However, the report notes that there is growing exposure of financial institutions to government sovereign bonds, which increases sovereign credit risk and exposure to money market volatility.

Balance sheet data can be used to create important risk metrics, such as liquidity mismatches between short-term deposits (liabilities) and hold-to-maturity corporate bonds (assets), which is relevant given the experience of Silicon Valley Bank (SVB) in the US. SVB had invested most of its assets in long-term investments, yet it relied heavily on short-term deposits. When interest rates began to rise, SVB experienced liquidity problems.

By using publicly available data on bank balance sheets we can assess the exposure of registered banks in SA to the types of risks SVB was exposed to. For example, the graphic shows the ratio of corporate deposits to total deposits, an indicator of deposit “flight risk”, and compares it with mortgage exposure on the asset side of bank balance sheets. Simultaneous higher values of these two ratios suggest that the risk of maturity mismatches is higher.

Though there is some clustering of banks around about 30% in each ratio, there is also a large amount of dispersion. The bank with the highest share of short-term corporate deposits is HBZ. Among the largest banks, Nedbank and Standard Bank have the largest proportions of mortgages in their total assets. Banks with no short-term corporate deposits or mortgages are excluded from the graphic.

But analysts can do only so much with balance sheet data, which does not tell you about many of the operational risks banks face. The crucial point is that the income statement and regulatory data is already collected and analysed by the Reserve Bank for good reason. If the “market” — including investors, researchers and civil society — had access to the same data, it would greatly enhance the effect of the Bank’s good efforts. The Basel III framework that governs banking regulations recognises that regulators are not perfect and that it is practical, and indeed democratically important, to share information more broadly.

Consider liquidity data, for example. The liquidity position of banks can be used to assess banks’ ability to meet short-term financial obligations and therefore help describe how resilient they might be to unexpected market volatility. Banks are required to meet a minimum liquidity coverage ratio (LCR), and making this data available at bank level would enable analysts to better characterise banking risks using historical data. Suitably rigorous statistical analysis could quantify the effect of macroeconomic developments such as changes in sovereign risk on the LCRs, and the risk profiles of specific banks.

It is not as if some SA banks are not already conducting world-leading modelling on their own data. In fact, the income sheet is still a fraction of the depth of information banks have been analysing for decades now. But it would be nice for regulators to open the door a smidgen to allow the market to analyse aggregated accounting line items for risk assessment purposes.

One might worry that more data availability might lead to market instability. On the contrary, it is considered best practice among leading central banks to make it easy for the public to understand the health of the bank they bank with. For example, the European Central Bank and Reserve Bank of New Zealand have banking dashboards on their websites that show how each bank performs compared with regulatory requirements and measures of their likely resilience to shocks.

Public availability of data is crucial not only to democratising information but also for enabling research and analysis to better understand what is happening in the economy. Banking data is particularly important given the complexity and changing nature of banking risks. The recent collapse of SVB demonstrated how banks (and regulators) can get things spectacularly wrong.

Would the SVB damage have been as pronounced if independent voices with access to the relevant data could warn of growing risks? Also unlikely.

• Dr Steenkamp is CEO at Codera Analytics and a research associate at Stellenbosch University. Roos is an associate with Codera.