Fiscal policy affects the outlook for demand and inflation and may therefore have implications for monetary policy. One measure of the impact of the fiscal stance on the business cycle is the fiscal impulse, which can be proxied as the year-to-year change in the cyclically adjusted budget balance. IMF estimates imply that the fiscal impulse has been slightly negative on average for South Africa since 2010. Taken in isolation, this implies that the fiscal stance was not a major contributor to inflation pressures over this period. Of course, government spending has impacted inflation in other ways. Take public sector wages. Average public sector wages grew at almost 2 percentage points faster per year than consumer prices between 2010 and 2021. Overall, government-related inflation has grown at well above the upper bound of the inflation target since 2009.

These estimates suggest that fiscal policy was only a meaningful brake on activity between 2018 and 2020, and it boosted the economy in the aftermath of the COVID-19 pandemic. Estimates from UNCTAD suggest that South Africa’s pandemic stimulus was the largest among the emerging markets considered, at about 4 percent of GDP. This only reflects increased transfers.

The IMF estimates imply that there has not been meaningful fiscal austerity since the global financial crisis (GFC). The chart below shows the cyclically adjusted primary budget balance. It excludes debt service costs from the budget balance and is adjusted to reflect the level that would be expected if the economy were to operating at its potential level (i.e. it is adjusted for the effects of the business cycle on tax revenue and government expenditure). The IMF estimates suggest that fiscal policy has been broadly supportive of aggregate demand since the GFC.

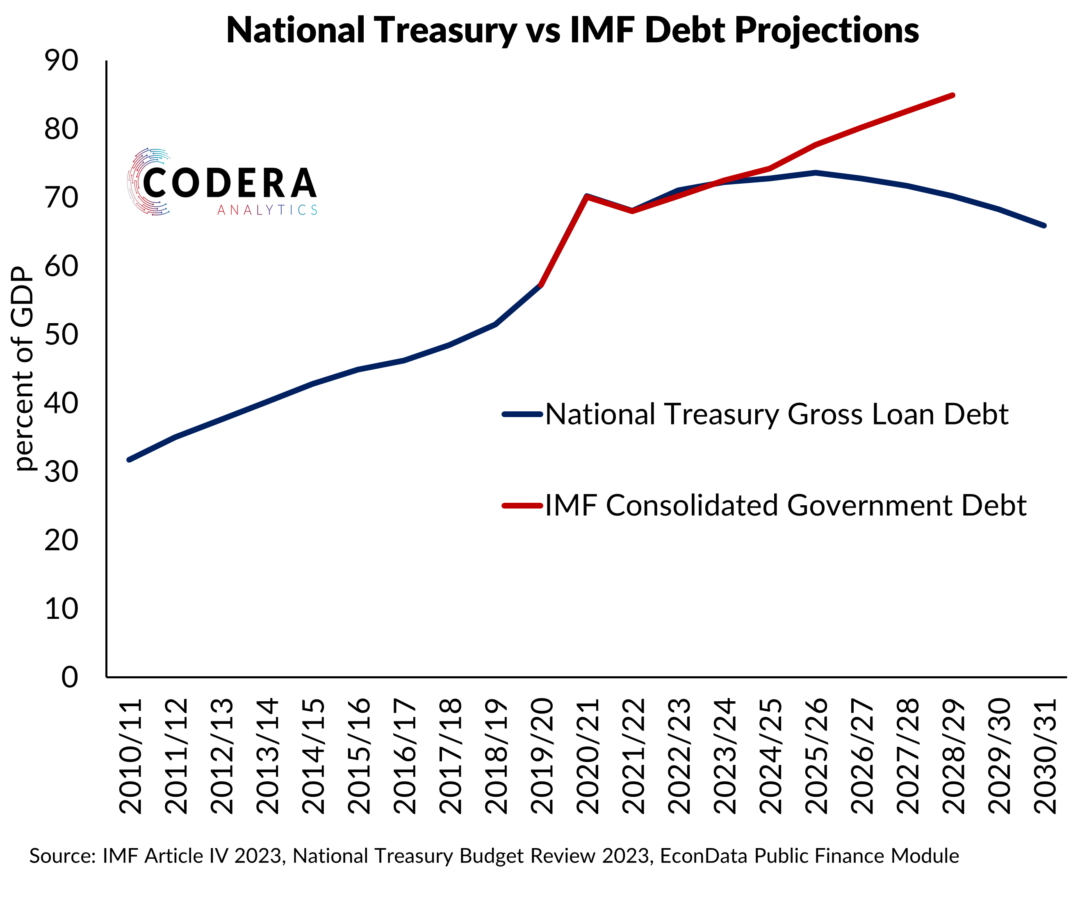

The IMF’s estimates of South Africa’s cyclical budget balance (both expressed as budget balance and primary balance terms) have remained in negative territory since 2009, implying that fiscal policy has stayed ‘loose’ even as the economy began to recover after the GFC and the output gap gradually closed ahead of the COVID-19 crisis. Looking ahead, the IMF assumes fiscal policy will become less stimulative, although both cyclical balances are expected to remain negative until 2025. The IMF expects that the cyclically adjusted primary balance will eventually turn positive. However, South Africa’s structural budget balance is predicted to deteriorate over the next 5 years, reflecting the impact of growing debt service costs from rising public debt.

Footnote

Since GDP data are released with a lag and get revised, it is difficult for policymakers to gauge the extent of current capacity pressures. The decline in trend growth and large recent GDP revisions in South Africa have made it difficult to assess fiscal space over the last several years. In this earlier post, we showed that the implied profile of the fiscal stance is meaningfully different over recent years if a real time output gap estimate is used instead of an ex-post estimate.